The Clorox Company (NYSE:CLX) is gaining momentum on the back of its smooth progress on 2020 Strategy, focus on e-commerce and brand-management initiatives. In addition, the company is benefiting from its strategic buyouts coupled with higher pricing and cost-saving efforts. Apparently, it delivered ninth straight quarter of positive earnings surprise in second-quarter fiscal 2019.

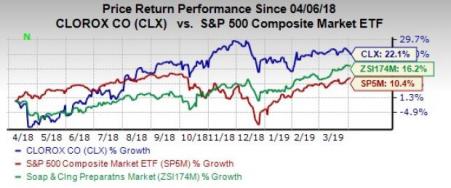

Impressively, this Zacks Rank #3 (Hold) stock remains investors’ favorite too as it returned 22.1% in a year. Shares of this leading consumer products company have also outperformed the industry, which rallied 16.2% in the same time period. Meanwhile, the S&P 500 index gained 10.4%.

Factors Narrating Clorox’s Growth Story

Clorox’s 2020 Strategy, which is aimed at driving growth at product categories and enhancing overall market share, is encouraging. The strategy focuses on increasing net sales by 3-5%, expanding EBIT margin by 25-50 basis points and generating free cash flow of 10-12% of sales, all on a yearly basis. Markedly, the 2020 Strategy is expected to be achieved through key accelerators like investment in brands; development of e-commerce; technological advancements; enhancement of growth culture and focus on the 3Ds - desire, decision and delight.

Meanwhile, Clorox remains keen on making strategic partnerships with retail customers and evolving capabilities in both physical world and online. As a result, Clorox witnessed an improvement in digital capabilities leading to a strong performance in e-commerce, which is now a significant revenue contributor. Notably, the company is ahead of its plan to achieve $500 million from e-commerce sales by 2020.

Clorox also has a diversified brand portfolio, which positions it well to deliver growth and sustain in the challenging macro landscape. The company’s approach toward brand management allows each of its brands to develop further through rigorous research and development, marketing strategies, financial control and operating leverage. In addition, management is focused on making investments in demand building including digital marketing, e-commerce and product innovation pipeline.

Furthermore, Clorox’s price increases and cost savings are providing a boost to gross margin. However, the margin growth was somewhat hurt by elevated commodity, and manufacturing and logistics expenses. In fiscal 2019, management expects gross margin to remain flat as gains from higher prices and cost-saving efforts are expected to be offset by increased costs and adverse foreign currency exchange rates.

Although Clorox continues to anticipate gross margin expansion in the second half of the fiscal year, it expects a muted growth due to the shift in supply-chain spending toward the back half. Moreover, the company expects EBIT margin to decline on flat gross margin expectations, and plans to complete the Nutranext integration and invest strongly in advertising to support the strong back-half innovation plans.

Nevertheless, gains from product innovations and buyouts are expected to drive Clorox’s top and bottom lines. Management projects sales growth of 2-4% from the fiscal 2018 level. Innovations are likely to deliver about 3 percentage points of additional sales. The top line is also likely to reflect the combined positive effect of the Nutranext acquisition and the Aplicare divestiture to the tune of 3 percentage points. Also, fiscal 2019 earnings per share of $6.20-$6.40 from continuing operations, includes nearly 8-12 cents benefit from the Nutranext acquisition. The Zacks Consensus Estimate for the fiscal year is currently pegged at $6.33.

Bottom Line

Although issues related to higher costs and foreign currency translations persist, we believe these concerns will be offset by Clorox’s impressive strategic efforts. Also, a VGM Score of B and long-term earnings growth rate of 6.4% demonstrates the stock’s inherent potential.

Three Better-Ranked Stocks in the Consumer Staples Space

Medifast, Inc. (NYSE:MED) has an impressive long-term earnings growth rate of 20% and a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

MGP Ingredients, Inc. (NASDAQ:MGPI) has outpaced the earnings estimates in the trailing four quarters by an average surprise of 2.4%. The company has a Zacks Rank #1.

General Mills, Inc. (NYSE:GIS) is a Zacks Rank #2 (Buy) stock, which has delivered an average trailing four-quarter positive earnings surprise of 11.1%.

Zacks' Top 10 Stocks for 2019

In addition to the stocks discussed above, would you like to know about our 10 finest buy-and-holds for the year?

Who wouldn't? Our annual Top 10s have beaten the market with amazing regularity. In 2018, while the market dropped -5.2%, the portfolio scored well into double-digits overall with individual stocks rising as high as +61.5%. And from 2012-2017, while the market boomed +126.3, Zacks' Top 10s reached an even more sensational +181.9%.

See Latest Stocks Today >>

MEDIFAST INC (MED): Free Stock Analysis Report

MGP Ingredients, Inc. (MGPI): Free Stock Analysis Report

General Mills, Inc. (GIS): Free Stock Analysis Report

The Clorox Company (CLX): Free Stock Analysis Report

Original post