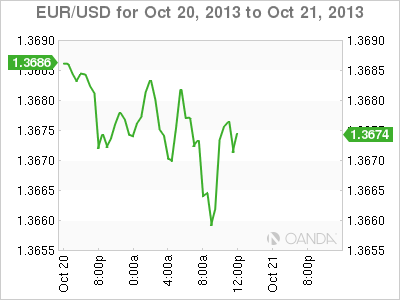

In an interview Monday morning, Chicago Fed Reserve President Charles Evans (a voting member) continues to push for continued monetary stimulus, reiterating that policy makers would probably require a "couple" more months of US jobs data before deciding to pare back on the $85b a month bond-buying program currently in place. EUR/USD" title="EUR/USD" border="0" height="300" width="400">

EUR/USD" title="EUR/USD" border="0" height="300" width="400">

The Fed's monetary stimulus program has created no inflationary pressures, nor an asset bubble. Corporate earnings have been strong, and a good enough reason to support an improving stock market, even though to some, current record benchmarks look a tad expensive.

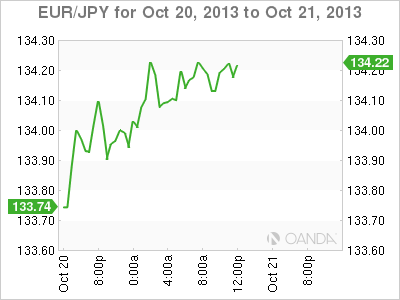

From his own viewpoint, Fed Evans believes that any move to taper at the December FOMC meet "will be pretty tough." The obvious reason, which has been well documented by Bernanke and his fellow policy cohorts, is the ongoing "fiscal drama" being played out in Washington – the US debt ceiling debacle has only been suspended, not dealt with under their "kick the can policy." EUR/JPY" title="EUR/JPY" border="0" height="300" width="400">

EUR/JPY" title="EUR/JPY" border="0" height="300" width="400">

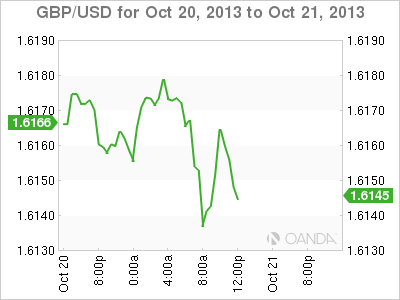

Consumer spending still needs to play a bigger role. "If various actors in the economy stepped back and let the business community really take hold and consumers, too, we could see a big expansion in growth and we could pull back that much more quickly" according to Evans. GBP/USD" title="GBP/USD" border="0" height="300" width="400">

GBP/USD" title="GBP/USD" border="0" height="300" width="400">

Dollar direction has been influenced by the markets interpretation of the Fed's timing to taper. The recent US partial shutdown has many revising US growth numbers for the remainder of 2013 and even next year. The dollars collapse across the board has been trading in tandem with delaying the timing to taper. Weaker projected growth requires ongoing fiscal stimulus. However, tomorrow's extraordinary non-farm payroll release is capable of beating expectations, if so, it could easily reverse, partially or all, the dollars slide experienced over the past-five trading sessions.

For now, consolidation near currency highs (dollar lows) takes hold as market awaits tomorrows release of Septembers NFP report. Option expiries and stop losses will most likely drive the limited interest in the New York market. Topside EUR offers continue to remain into 1.3710 with big stop losses just above may become more attractive if EUR dips remain somewhat limited.

Original Post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Chicago Fed Evans “No” To Taper

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.