In early December 2014, I unveiled my Dividend Death Watch, a list of energy stocks and master limited partnerships (MLPs) with dividend sustainability issues.

Well, the axe has already fallen…

Last week, Linn Energy LLC (NASDAQ:LINE) and BreitBurn Energy Partners LP (NASDAQ:BBEP) each cut their distributions by over 50%… and more cuts are sure to follow.

Hopefully, the unfolding energy bust will convince investors that chasing yield ends in tears.

As I’ve said all along, we’re looking for dividend growth, not high yields. And the faster the dividend growth, the better.

With that in mind, let’s take a look at two companies that recently gave their dividend payouts huge boosts, even though few have noticed.

Natural Monopolies

Last year, utilities were the best-performing U.S. sector. The strong showing by this regulated, low-growth group surprised many.

However, the investing environment continues to favor these natural monopolies in early 2015, as interest rates fall further and the stock market enters a period of heightened volatility.

Some utility stocks have become expensive, though. For example, Duke Energy (NYSE:DUK) (DUK) trades at an enterprise-value-to-EBITDA (EV/EBITDA) ratio of 13.2x and a price-to-sales (P/S) ratio of 2.4x. These are lofty valuation multiples, especially for a utility.

By comparison, the utility stocks in the S&P 1500 SuperComposite have an average EV/EBITDA ratio of 10.5x and an average P/S ratio of 1.8x. Thus, we must be careful when looking for opportunities in this sector.

One of the cheapest utilities is the AES Corporation (NYSE:AES), which operates coal, diesel, hydropower, gas, oil, wind, and biomass power plants.

With an EV/EBITDA ratio of 8.0x and a P/S ratio of 0.6x, AES is valued at a significant discount to the average utility.

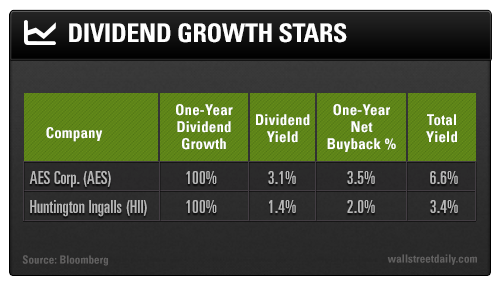

Now, AES’ stock is cheap primarily due to its international exposure. The firm operates in 19 countries around the world, and therefore is subject to foreign exchange and local political risks. However, this diversification should be viewed as beneficial, and the fact that the company recently doubled its dividend payout shows that management is very confident in the underlying businesses.

Like AES, my next dividend growth star doubled its dividend payout in 2014. And, though it’s not a utility, it is a de facto monopoly…

A New Carrier Class

Huntington Ingalls (NYSE:HII) is the sole builder of U.S. Navy aircraft carriers and has built more ships in more classes than any U.S. naval shipbuilder.

For the past couple of years, Huntington Ingalls has been building the Gerald R. Ford, the first in a brand-new class of aircraft carriers. The second aircraft carrier in the Ford class, the John F. Kennedy, is already in early stages of construction.

Basically, Huntington’s backlog is very healthy.

HII also happens to be one of the most attractively valued defense stocks. It trades at lower EV/EBITDA and P/S ratios than every one of its peers: Lockheed Martin (NYSE:LMT), General Dynamics (NYSE:GD), Raytheon Company (NYSE:RTN), and Northrop Grumman(NYSE:NOC).

Not only have both of these companies doubled their dividend payout in the past year, they’ve been repurchasing shares, as well, giving them respectable total yields (dividend yield plus the net share buyback percentage over the past year).

As you know, I’m not as optimistic about U.S. and global economic prospects as most economists. Therefore, I take comfort in the fact that the revenue from these two companies is relatively insensitive to the business cycle.

The combination of outsized dividend growth, cheap valuations, and reliable streams of revenue suggests these stocks are poised to outperform in 2015.

Safe (and high-yield) investing,