Bank stocks spent much of the past decade recovering from the financial crisis. This was particularly true for the big U.S. bank stocks as they faced a unique set of regulatory challenges that were brought about by the crisis. In the years since, the largest banks have collectively rebuilt very strong capital buffers, and in more recent years, have returned billions of dollars to shareholders through dividends and share buybacks.

Bank of America (NYSE:BAC) certainly faced a tough road since the crisis when it was on the brink of insolvency for a short period, but the company has been born anew in recent years and in our view, offers investors very strong prospective total returns. Bank of America is a high-quality dividend growth stock among the big U.S. banks.

Business Overview And Recent Events

Bank of America was founded in 1904 and is headquartered in Charlotte, NC. The company provides traditional banking services such as deposit-taking and auto and home lending, but also competes heavily in credit cards, as well as wealth management. To a lesser extent, Bank of America also plays in global banking and equity and debt markets.

The bank delivers more than $90 billion of annual revenue and its current market capitalization is $287 billion, making it one of the largest financial companies in the world by that measure.

Bank of America reported Q1 earnings on 4/16/19 and results were better than consensus estimates. Total revenue was essentially flat year-over-year, falling fractionally to $23 billion. A 5% gain in net interest income was entirely offset by a 6% decline in noninterest income. The gain in net interest income arose from higher lending rates as well as stronger lending spreads, thanks to still-low deposit funding rates. Indeed, net interest yield was up 9bps to 2.51% in Q1, a very strong gain considering the significant flattening of the yield curve that has occurred in the past twelve months.

Average loans and leases rose 4% year-over-year to $897 billion as consumer loans gained 3% and commercial loans added 4%. Average deposits rose 5% year-over-year to $1.4 trillion.

Credit quality deteriorated slightly in Q1 as provisions for credit losses increased $179 million to $1 billion. The bank’s net charge-off ratio increased 3bps to 0.43% during Q1, and while these numbers are moving in the wrong direction, we see this as more of a fluctuation in credit metrics rather than a trend change. Credit quality was at historical highs in the relatively recent past, so some moderation off of those levels is to be expected. While we’ll watch Bank of America’s credit quality metrics, we see no cause for concern today.

Bank of America’s years-long focus on reducing operating costs continues to pay off and in Q1, operating expenses fell 4% against the prior year’s Q1. That drove the bank’s efficiency ratio down to 57%, which is in line with its large banking peers. Bank of America struggled for years after the crisis with a bloated cost structure thanks to a combination of the Countrywide acquisition and legacy assets that weren’t performing, and had to be wound down. That is all behind it at this point and Bank of America is operating quite efficiently today, which we see as adding to the attractiveness of the stock.

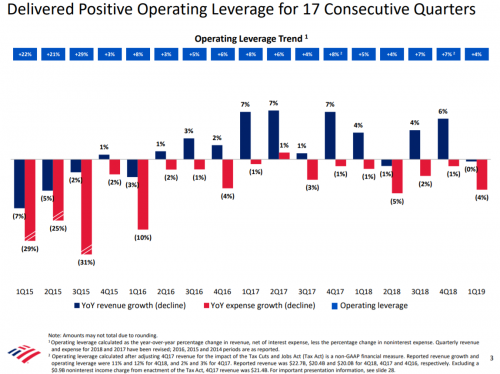

Indeed, as we can see below, Bank of America has achieved positive operating leverage for a staggering 17 consecutive quarters.

Source: Q1 earnings presentation, page 3

This leverage provides the bank with higher profit margins over time whether revenue grows or not. We can see that even in a variety of environments in the past 17 quarters, Bank of America has managed to reduce expenses over and over again, and while the low-hanging fruit has certainly been picked, we do not see this story as complete. This should help drive margin improvement in the coming years, as it has in recent years. This tailwind becomes even more powerful when revenue is rising, which we see as the case for the foreseeable future.

Pretax income rose 4% in Q1 while net income rose 6% on a dollar basis. On a per-share basis, earnings rose 13% to $0.70 year-over-year thanks in large part to a reduced float. Bank of America has been returning capital to shareholders in enormous amounts in recent years, helping to not only rebuild the dividend, but reduce the float as well.

The bank repurchased $6.3 billion in stock in Q1 alone, in addition to the $1.5 billion it returned to shareholders via dividends. Bank of America has become an outstanding capital return story in recent years, and we see that continuing.

After the Q1 report, we’ve slightly increased our earnings-per-share estimate for 2019 to $2.85.

Bank of America trades today at 10.5 times our expected earnings for 2019, which compares favorably to our fair value estimate of 12 times earnings. Should the stock revert to our estimate of fair value over the coming years, we see a low single digit tailwind to total returns as a result.

Combined with our estimate of 8% annual earnings growth – due to a small increase in revenue, continued margin expansion, and the share repurchase program – in addition to the current dividend yield of 2%, we see Bank of America producing low double-digit total returns annually in the coming years.

Strong Capital Generation Leads To Dividend Growth

Bank of America’s dividend was devastated during the financial crisis as the company tried simply to stay in business during the worst of it, unconcerned with shareholder returns. However, those days are gone and Bank of America’s capital position not only makes it much better insulated against losses in the future, but also allows it to return a lot of cash to shareholders.

While the focus has been on the buyback in recent quarters, the dividend has grown at very strong rates as well, and we see that continuing to be the case in the coming years.

Bank of America’s capital position has been more than adequate for years at this point, which means when it generates capital – the vast majority of which comes from earnings – it has the flexibility to pay that capital out to shareholders rather than hoard it on the balance sheet.

Because of this, we see Bank of America producing very high rates of dividend growth in the coming years, raising the payout from the current $0.60 per year to $1.42 by 2024. While that is an immense amount of dividend growth, Bank of America’s payout ratio is just 21% today, meaning there is a lot of upside remaining from boosting the proportion of earnings that are distributed as dividends. Combined with robust earnings growth, we think the dividend growth story at Bank of America is a long way from being done.

Final Thoughts

Bank of America has rebuilt itself since the Great Recession, becoming much stronger in the process. This recovery fueled its ability to return billions of dollars to shareholders annually. Combined with a low valuation and robust growth prospects, the stock earns a buy rating due to its high expected returns of ~13% annually in the coming years.

In addition to an exceptional dividend growth profile, Bank of America has a lot to offer shareholders, making it one of the best large bank stocks in the U.S. today.