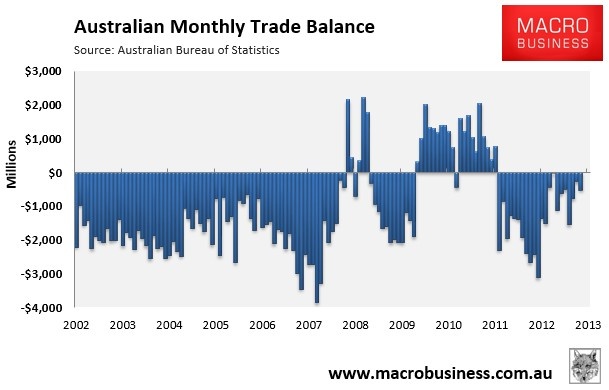

Australia’s trade deficit increased more than expected in October to AUD 529 million, which points to softer economic performance as commodity exports declined. Western Australia continues to drive a large share of exports to China to record highs. The October trade balance and disappointing third-quarter GDP suggests that Australia will face a difficult path as the economy struggles to re-balance. However, underlying data continues to highlight early signs of productivity growth away from mining, as housing and industrials take the lead.

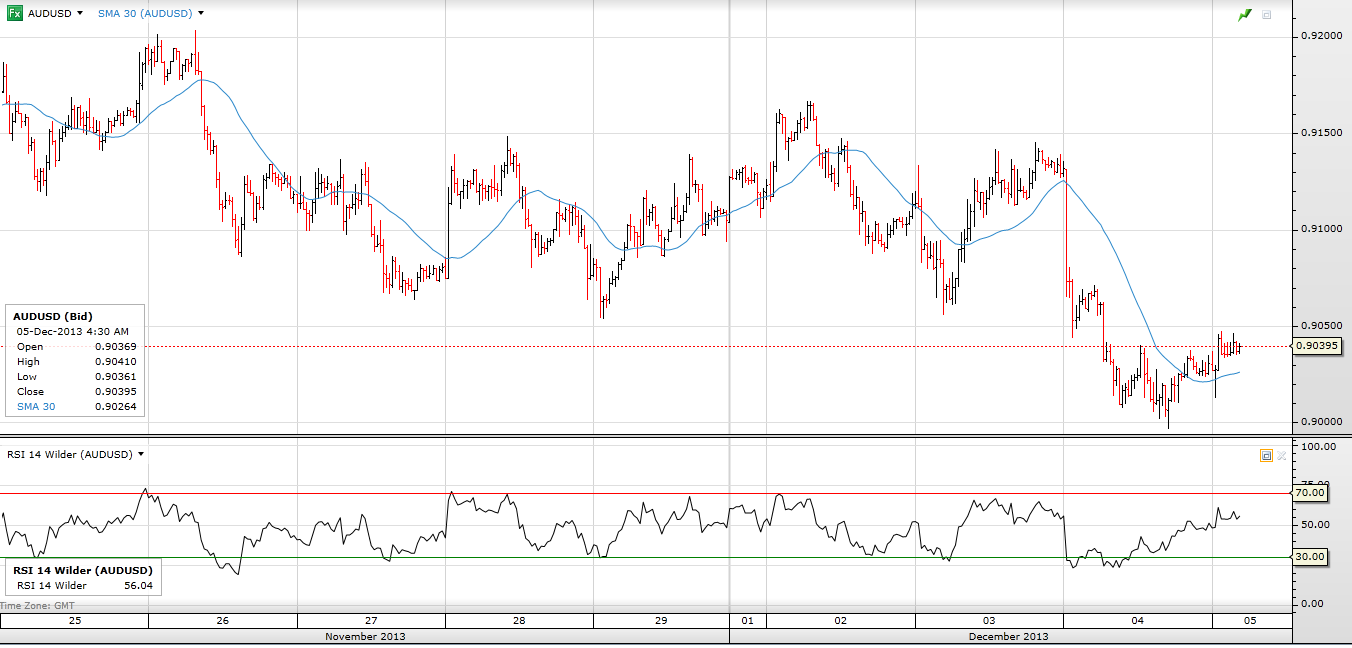

Limited upside for Aussie

The macro reality continues to push AUD lower, but it will still need to settle below 0.9000 in order to please the Reserve Bank of Australia (RBA). AUDUSD had a few upside moments this past week, but most of it was from USD month-end profit-taking ahead of the important US non-farm payrolls report on Friday. Traders are waiting for continued downside momentum, but AUDUSD will need to move below its 30-day simple moving average, seen on the hourly chart below.

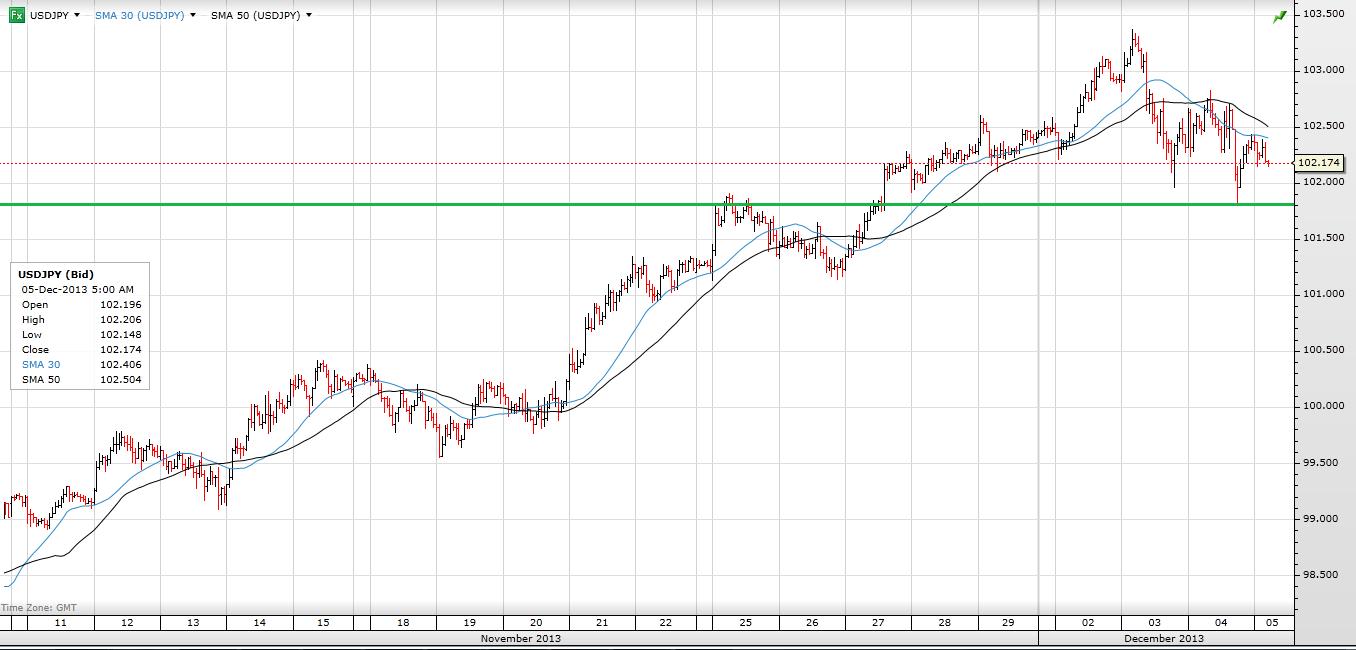

USD overshadows JPY

USDJPY is taking an extended breather as traders take profit, but lower support levels around 101.80 and 102 could help. Recent developments from Japan are also supportive for USDJPY, but the slow moving upper house is causing some drag. Reports that Japan is preparing a USD 53 billion stimulus package this week caused little market reaction, and was priced in since September. Japan has been silent lately, so the market should look towards December 12 when the Cabinet is scheduled to report details of a supplementary budget, if approved.

There seems to be a greater correlation between the Nikkei and USDJPY, which could reflect JPY weakness. 15,000 is an important level for Nikkei, so traders might feel more comfortable if we remain above that mark.

What’s ahead

On Thursday, the European Central Bank’s (ECB) rate decision will be the key event, and while the market does not expect a change in policy, ECB president Mario Draghi’s press conference could trigger some interesting price action on the crosses.

In the US, the final estimate for Q3 GDP will be scrutinised, with a close look at personal consumption and initial jobless claims data.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Asia Focus: USD Profit-Taking Continues, But Aud Downside Likely

Published 12/05/2013, 05:51 AM

Updated 03/19/2019, 04:00 AM

Asia Focus: USD Profit-Taking Continues, But Aud Downside Likely

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.