Video streaming website Netflix (NASDAQ:NFLX) is slated to announce its first quarter 2015 earnings results on Wednesday, April 15th after market close. Wall Street expects the company to post earnings of $0.68 a share on $1.57 billion in revenue, down from $0.86 earnings per share and up from $1.48 billion in revenue from the same quarter a year prior.

In its Q4 2014 report, the video-streaming company posted a record 13 million new members throughout the year, resulting in a total of 57.4 million global Netflix members. Netflix also posted revenue of $1.48 billion, marking a substantial year-over-year increase from $1.18 billion. The company forecasts 1.80 million new domestic subscribers and 2.25 million new international subscribers in Q1

The streaming service is currently available in more than 50 countries throughout North America, South America, and Europe. The streaming service recently became available in New Zealand and Australia this past March. In addition, there has been talk of Netflix expanding its service to Asia sometime in the near future.

Netflix has also been releasing its largest amount of original content yet throughout 2015. The 320 hours of original content Netflix plans to release throughout the year will actually cost the company less than most of its licensed content.

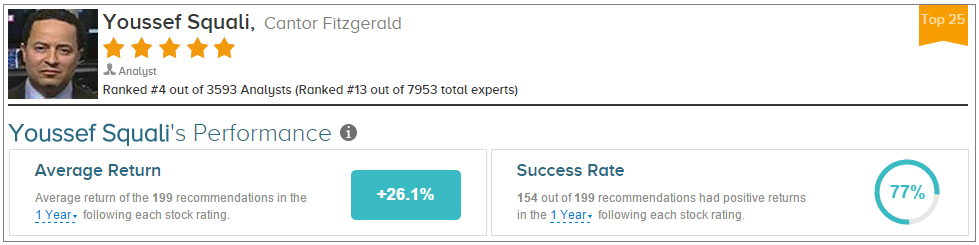

On April 13th, Cantor Fitzgerald analyst Youssef Squali weighed in on Netflix ahead of its Q1 earnings with a Buy rating and $500 price target, according to SmarterAnalyst. He noted, “Given Netflix’s significant global subscriber growth potential, improving original content slate, ability to raise prices over time and recent headlines around unbundling, we remain positive on Netflix, the original OTT disruptor.”

Sqauli has rated Netflix 31 times since January 2010, earning a 100% success rate recommending the company and a +54.9% average return per NFLX recommendation. Overall, he has a 77% success rate recommending stocks and a +26.1% average return per recommendation.

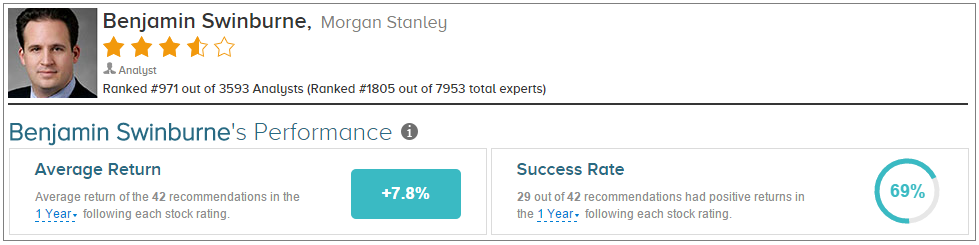

Likewise on April 13th, Morgan Stanley analyst Benjamin Swinburne maintained an Overweight rating on Netflix with a price target of $535. The analyst believes the increased momentum in user engagement conveys “continued success of its content strategy.” He added, “We believe lower churn is the most immediate benefit, as consistent new content through the year lowers incentive for subs to disconnect even temporarily.”

Swinburne has rated Netflix 5 times since June 2014, earning a 50% success rate recommending the stock and a +2.0% average return per recommendation. Overall, he has a 69% success rate recommending stocks and a +7.8% average return per recommendation.

On average, the top analyst consensus for Netflix on TipRanks is Moderate Buy.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Analysts Remain Positive on Netflix Ahead of Earnings

Published 04/14/2015, 08:35 AM

Updated 05/14/2017, 06:45 AM

Analysts Remain Positive on Netflix Ahead of Earnings

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.