The case for the aluminum market is one of short-term gain, long-term pain.

A Reuters article paints a fairly positive picture of an industry not so far from balancing supply and demand as is generally believed, but an industry in which spot premiums are dissuading producers from taking steps to close the gap.

The Case For Surplus

Of course it’s not quite as simple as that, as a little more explanation will make clear. First, the traditional case for a market seriously in surplus.

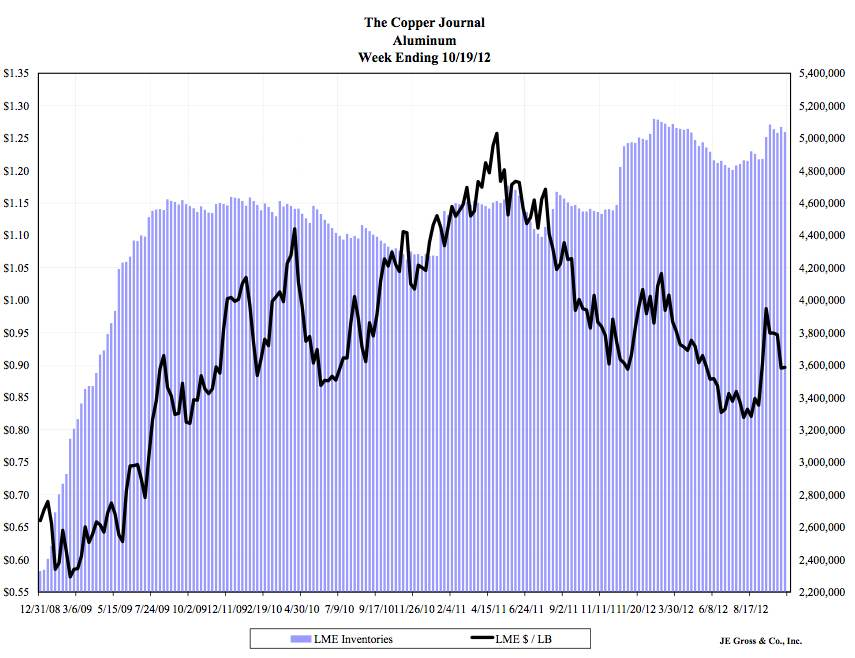

HSBC bank, in a recent quarterly report, estimates aluminum capacity to be 1.5 to two million tons per year in surplus, with exchange and non-exchange inventory to be circa 6.7 to 7 million tons.

Reuters, on the other hand, quotes Steve Hodgson, head of international sales at Russian aluminum producer Rusal, who says but for the physical premiums available to spot sellers, between 2.5 and four million tons of capacity would already have closed, yet Rusal puts the surplus at only 300,000 to 400,000 tons.

Underlining how important this physical premium has become, Rusal has just announced that all its contracts will henceforth incorporate a floating element to capture the physical premiums prevailing at the time of delivery.

Propping Up The Industry

Hodgson suggests 10-15% of the industry is being kept profitable by these physical premiums alone. Taking this to its logical conclusion, that means the likes of Glencore, JPMorgan and Goldman Sachs, whose control of the LME warehouse network (in large part causing this availability squeeze) are keeping a number of Western producers afloat and imposing higher prices on consumers everywhere than would otherwise be the case.

Whether you take Rusal’s view of surplus or HSBC’s is probably academic -- they both agree the market is in surplus and will likely remain so for the foreseeable future.

Downside Risk

Indeed, the risk is if anything to the downside inasmuch as increased availability -- from increased Chinese exports, a deeper recession in Europe, the U.S. failing to resolve its budget negotiations and incurring the “fiscal cliff” penalty or a collapse in the forward premium supporting the stock and finance plays -- rather than to the upside.

If Rusal is right (and we have our doubts about these numbers), it would not take much capacity to be closed to achieve balance; ironically, if that were to happen, the forward curve could flatten sufficiently for the stock-and-finance plays to slow or even cease, easing the physical premiums and resulting in more capacity being idled -- a potentially self-feeding spiral.

Here’s an alternate viewpoint on US aluminum capacity, from Aluminum Association President Heidi Biggs Brock, interviewed by MetalMiner at Aluminum Week in Chicago:

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Aluminum And The 'Availability Squeeze'

Published 10/23/2012, 02:52 PM

Updated 07/09/2023, 06:31 AM

Aluminum And The 'Availability Squeeze'

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.