Tuesday, May 10

![]()

Thursday, May 12

![]()

![]()

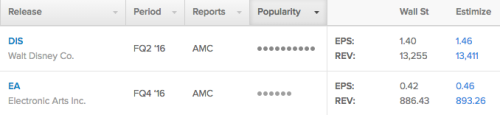

Walt Disney Company (NYSE:DIS)

Consumer Discretionary - Media | Reports May 10, after the close.

The Estimize community calls for EPS of $1.46, six cents higher than Wall Street, while revenue estimates of $13.4B just above the sell-side’s $13.25B. The Estimize community has been slightly bullish on Disney’s profitability, moving EPS estimates up 4% since the FQ1 report, now expecting YoY growth of 18%. Revenue estimates have only been ratcheted up 1%, and are expected to grow 8% from the year-ago period. On average DIS has beaten on EPS 65% of the time, but only 47% on sales.

What to Watch:

Studio Entertainment: Disney is coming off a strong Q1 primarily driven by the success of Star Wars: The Force Awakens. The global success of the movie drove revenue growth at both Studio Entertainment and Consumer products which increased 86% and 23%, respectively. This quarter should continue to get a nice bump as the blockbuster was still going strong well into the beginning of 2016, plus the box office success of animated film, Zootopia, which currently stands as the top grossing movie of 2016, nearing $1 billion in ticket sales as of early May. Meanwhile, the newest Captain America movie released last Friday drew in $180 million in ticket sales for its opening weekend, a benefit that won’t be seen until next quarter.

Parks & Resorts: Lately parks and resorts have performed just as well as Disney’s studio entertainment. This sector saw revenue increased 9% and operating income climb 21% for Q1 2016. Higher operating income at domestic locations was due to higher average ticket prices and attendance growth. This more than offset the increases in labor costs and new guest offerings incurred in the quarter. With a Star Wars themed attraction set to launch soon, parks and resorts should continue to see stable growth.

Media Networks: Media networks, on the other hand, have been a sour spot for Disney lately. As cord cutting habits run rampant and programming costs continue to increase, cables networks suffer. Last quarter, Disney saw operating income fall 5% in this segment, due to a substantial decline from ESPN.

Electronic Arts (NASDAQ:EA)

Information Technology - Software | Reports May 10, after the close.

The Estimize community calls for EPS of $0.46, four cents above Wall Street. Revenue expectations from Estimize are also higher at $893M as compared to the Street’s $886M. Estimates have remained relatively flat over the last 3 months, with EPS expected to grow 18%, and sales anticipated to remain in-line with year-ago results. EA tends to be a big mover after earnings, with the stock increasing 5% on average in the 30-day post report period. The company has a decent history of beating, surpassing the Estimize EPS consensus in 78% of reported quarters, and revenues 56% of the time.

What to Watch: Just like Disney, EA received a huge boost last quarter thanks to the success of Star Wars: The Force Awakens. Sales of Electronic Arts’ Star Wars based game, Battlefront, has already well surpassed the 13 million benchmark established for March.

Apart from Star Wars, EA has been seen success across many of its other hits. Last year, Madden 2016 was the #1 sports title in the U.S. while FIFA topped that same list in Europe. Meanwhile the return of Need for Speed drew twice as many active players as the previous game. Players also logged more than 150 hours of gameplay from its first person shooting games, Battlefield.

Besides console and PC games, EA is emerging as a major player in the rapidly growing mobile gaming sector. It’s Madden football games are consistently in the top 5 most downloaded games on the Apple (NASDAQ:AAPL) Store. Last quarter featured nearly 50% year over year growth in active players for Madden NFL Mobile. Mobile gaming continues to be the fastest growing sector in the gaming industry and could prove beneficial for EA down the road.

Fossil Group Inc (NASDAQ:FOSL)

Consumer Discretionary - Textiles, Apparel & Luxury Goods | Reports May 10, after the close.

The Estimize consensus calls for EPS of $0.20, two cents above Wall Street and seven above company guidance. Revenue expectations are just slightly more bearish at $667.75M vs the sell-side’s $667.8M, but both are higher than guidance of $663.5M. These numbers have been trending downward since the last quarterly report, with Estimize EPS estimates falling 37% and revenues down 3%. This puts growth expectations at -75% for EPS and -8% for sales. This is a company that has historically beaten on the bottom-line in 65% of reported quarters, and on sales in 47% of reported quarters.

What to Watch: Fossil is best known for making watches not only under its own brand name but also for Michael Kors, Kate Spade and other high fashion brands. The company is coming off a better than expected fourth quarter which saw a 12 cent beat on the bottom line and $70 million on the top. Despite the beat, the last two quarters have come with negative growth for both earnings and sales, as the company is in the midst of a brand transformation. The stock has followed suit, losing over 50% of its value in the last 12 months.

Lately, Fossil is seeing encouraging trends through its core brands, Fossil and Skagen, aided by strong ecommerce growth, rising direct to consumer sales, and modest comp store sales. Growth from these brands last quarter were largely offset by declines in the company’s multi-brand licensed watch portfolio and weak currency conditions. At the beginning of the year Fossil announced it would let it’s watch license with Burberry expire in December 2017, a move that some analysts believe could cost the company between $100-200 million a year.

As smartwatches rise in popularity, Fossil is taking steps to continually innovate its product offerings. Last December the company purchased wearables technology provider, Misfit, in what looks to be a move towards a Fossil fitness tracker. Meanwhile, Fossil already develops and sells smartwatches with the android operating system.

Shake Shack (NYSE:SHAK)

Consumer Discretionary - Hotels, Restaurants & Leisure | Reports May 12, after the close.

The Estimize consensus calls for EPS of $0.07, one penny above Wall Street. Revenue expectations of $52.7M are just slightly higher than the Street’s $52.5M. Estimates have remained largely unchanged since the Q4 2015 report, with YoY growth expected to come in at 86% on the bottom-line, and 41% on the top-line. This is a stock that tends to have huge price swings around the earnings season. In the 5 quarters since its IPO, shares increase an average of 19% in the 30-day pre-earnings period, only to fall 8% in the 30-day post-earnings period. SHAK historically has beaten both EPS and revenue estimates 80% of the time.

What to Watch: Not only is this a company that tends to beat, but they beat by a lot! In the last 4 quarters, SHAK has posted an average EPS surprise of 162%, and YoY growth of 200 - 900%. Revenue growth was also impressive in 2015, increasing 47%+ each quarter. Arguably the more important metric for this company is same shack sales, which increased 11% in Q4, and 13.3% in 2015. The outlook for 2016 isn’t as impressive, with the company guiding for same shack sales of 2.5 - 3.0%. First quarter 2016 expectations look less rosy due to increased labor costs and beef prices.

Despite changing consumer preferences for organic and fresh meal options, which has helped boost so many fast casual names such as Shake Shake, the need for value in some cases has shifted the focus back to fast food joints which are attempting to offer healthier options as well. However, SHAK has a very loyal customer; quarterly traffic increases are driven by limited time offers and constant menu innovations.

Shake Shack continues with it’s aggressive expansion plan, with 13 domestic stores set to open this year, and 7 licensed Shacks scheduled to open in the U.K. Middle East and Japan.

Nordstrom (NYSE:JWN)

Consumer Discretionary - Multiline Retail | Reports May 12, after the close.

The Estimize consensus calls for EPS of $0.45, in-line with Wall Street. Revenue expectations of $3.289M are just slightly below the Street’s $3.293M. Numbers on the bottom-line have been ratcheted down 22% in just the last 3 months, with top-line numbers only being reduced 2%. This puts growth expectations at -27% for EPS and 3% for sales. Nordstrom has a terrible track record for beating, only surpassing the Estimize EPS consensus 53% of the time and revenues 20% of the time.

What to watch: The outlook for all department stores is rather bleak for Q1 with Macy’s Inc (NYSE:M), Kohl’s Corporation (NYSE:KSS) and Nordstrom all expecting YoY profit declines, with only JC Penney Company Inc Holding (NYSE:JCP) anticipated to post growth this week. After a terrible fourth quarter, missing by 5 cents on EPS and $77M on the top line, Nordstrom’s management team issued lower-than-expected guidance for 2016, expecting earnings to decline 30% in first half of the year due to a heavy investment cycle and the shift of its anniversary sale.

Of the department stores, Nordstrom is considered higher-end, a hard spot to sit as the US consumer becomes more value-focused and less willing to spend on apparel. However, same store sales remained strong during the first half of 2015, coming in at 4.4% and 4.9% in Q1 and Q2, dipping down to 0.9% and 2.7% in the last two quarters of the year. Expectations for 2016 are light, with the company expecting comparable store sales of 0 - 2%. A large part of the company’s success during the first half of the year was attributed to Nordstrom Rack, Nordstrom’s discount store. That segment has continually seen sales grow in the double-digits, but lately weakness in the full-price locations have offset that strength.