It’s the last day of 2013. Some markets are closed for the day, while others will close earlier than usual. After the wild ride in currency markets over the past two days, it is uncertain if there is still some market manipulation left to be done, or if all the exotic option barriers have already been hit. Nevertheless, the last trading day of the year provides us with all-important settlement prices and the incentive is strong to drive prices to convenient levels.

If you are taking the rest of the week off, note that the European Central Bank’s (ECB) meeting is next week, on January 9. This week, the final PMIs are out on Thursday and the Eurozone monetary data on Friday. Both could have an effect on the ECB’s tone. With the EURUSD trading right below last October’s high of 1.3830 (and the high of 2013, if you omit the weird and short-lived spike on Friday to near the 1.39 level), there will be plenty of opportunities for the pair to move in the coming sessions.

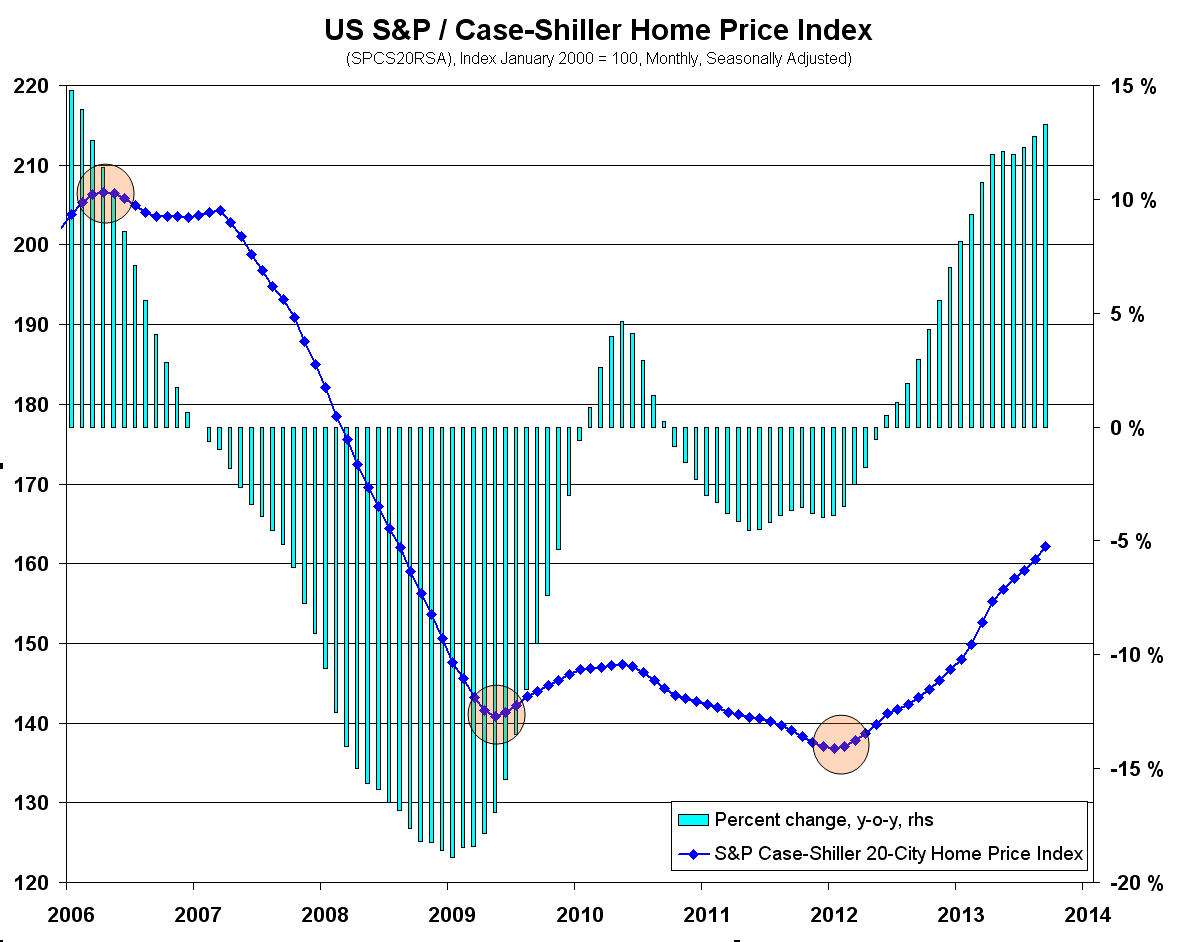

US October S&P / Case-Shiller Home Price Index (14:00 GMT). The 20-city index is expected to have increased by 13 percent in October from year ago and 0.7 percent from September. The index has risen every month since December 2012. It is worth noting that the index is calculated from average prices over the past three months. The October LPS home price index was published on Monday and showed home prices rising 0.1 percent from the previous month and 8.8 percent year-over-year. Today’s data release should offer no big surprises as data for the first two months — and practically for the third month as well — are already in.

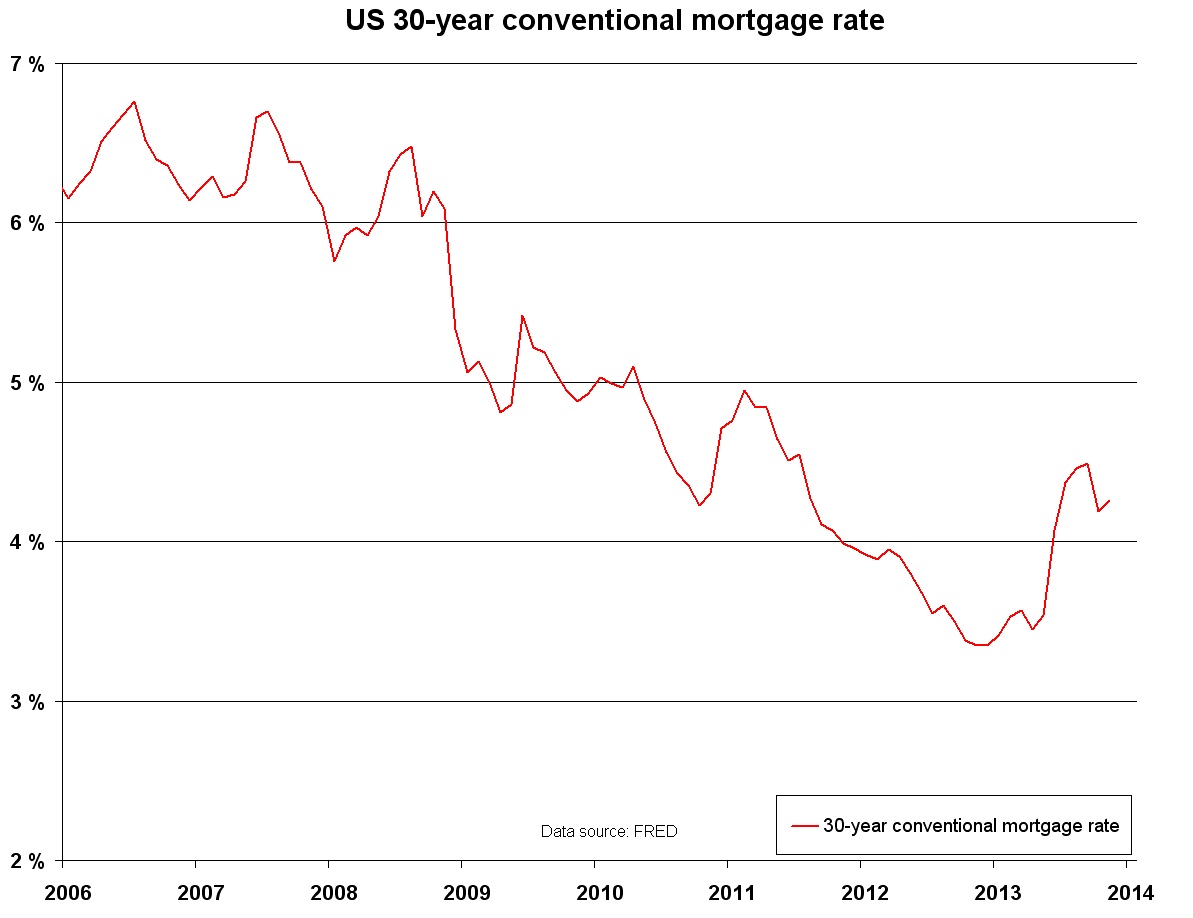

Longer-term, it will be interesting how the housing market will digest the higher interest rates. The 30-year mortgage rate is currently roughly a full 1 percent higher compared with the beginning of 2013. Then again, real estate prices are still far below their bubble peaks and those prices coincided with much higher mortgage rates than we have now. The blog Calculated Risk yesterday had a nice overview of the different housing indices and forecast that house prices would continue rising in 2014, but at a more modest rate than in 2013.

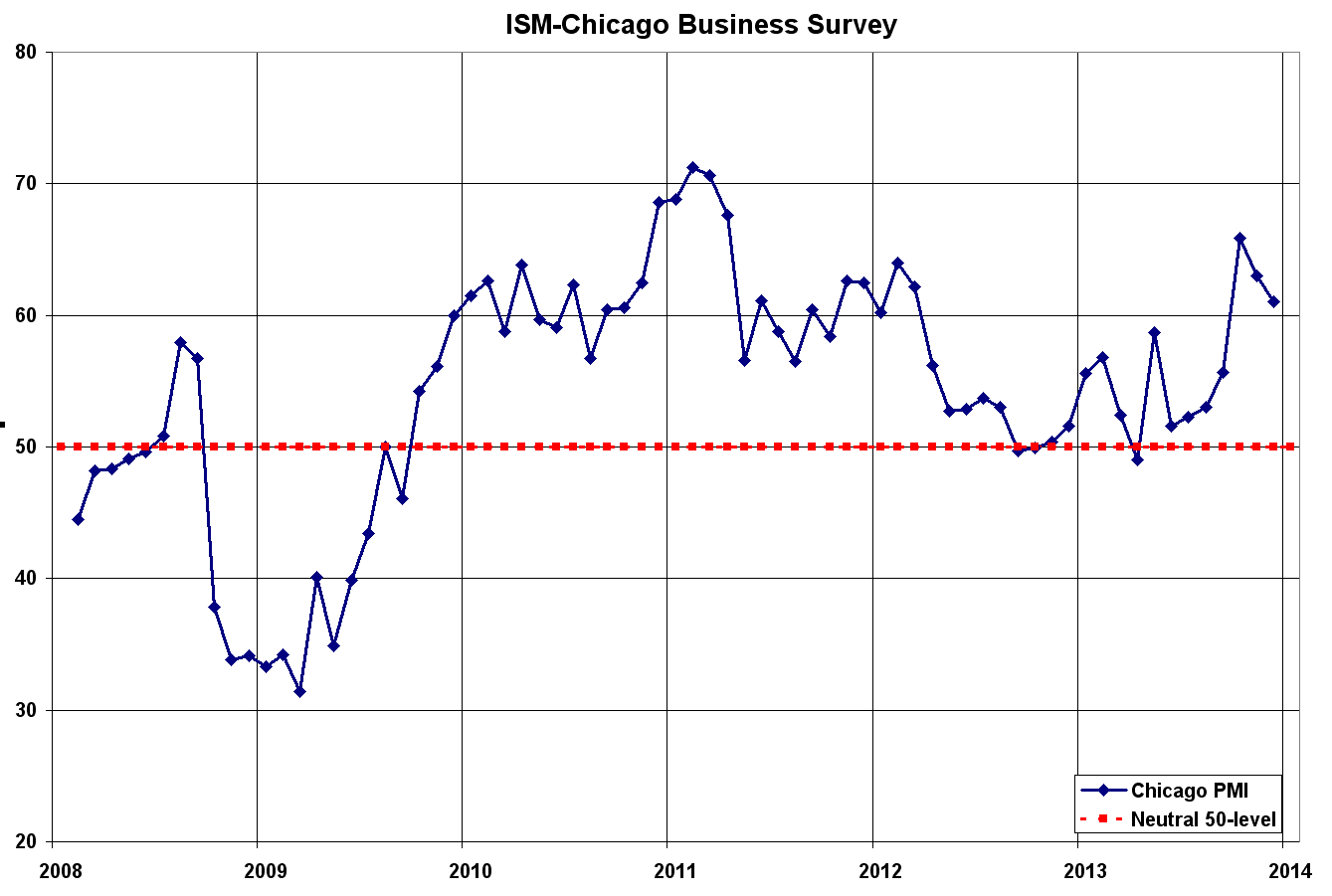

US December Chicago Purchasing Manager Index (14:45 GMT). The regional Chicago PMI is expected to post a small decline to 61.0, down from 63.0 in November. The index is clearly above the 50-level, suggesting positive growth outlook. The index's small decreases in the past two months have given away half of the gains October’s monstrous surprise jump generated. As Saxo Bank Head of Macro Strategy Mads Koefoed noted at the time, October’s increase was unusually large. Perhaps this is just mean reversion to the long-term trend and I would not be too worried until the index starts to poke below the 55 level. The November press release is here and December’s will be available here. This is the last regional number before the national statistics are published next Thursday.

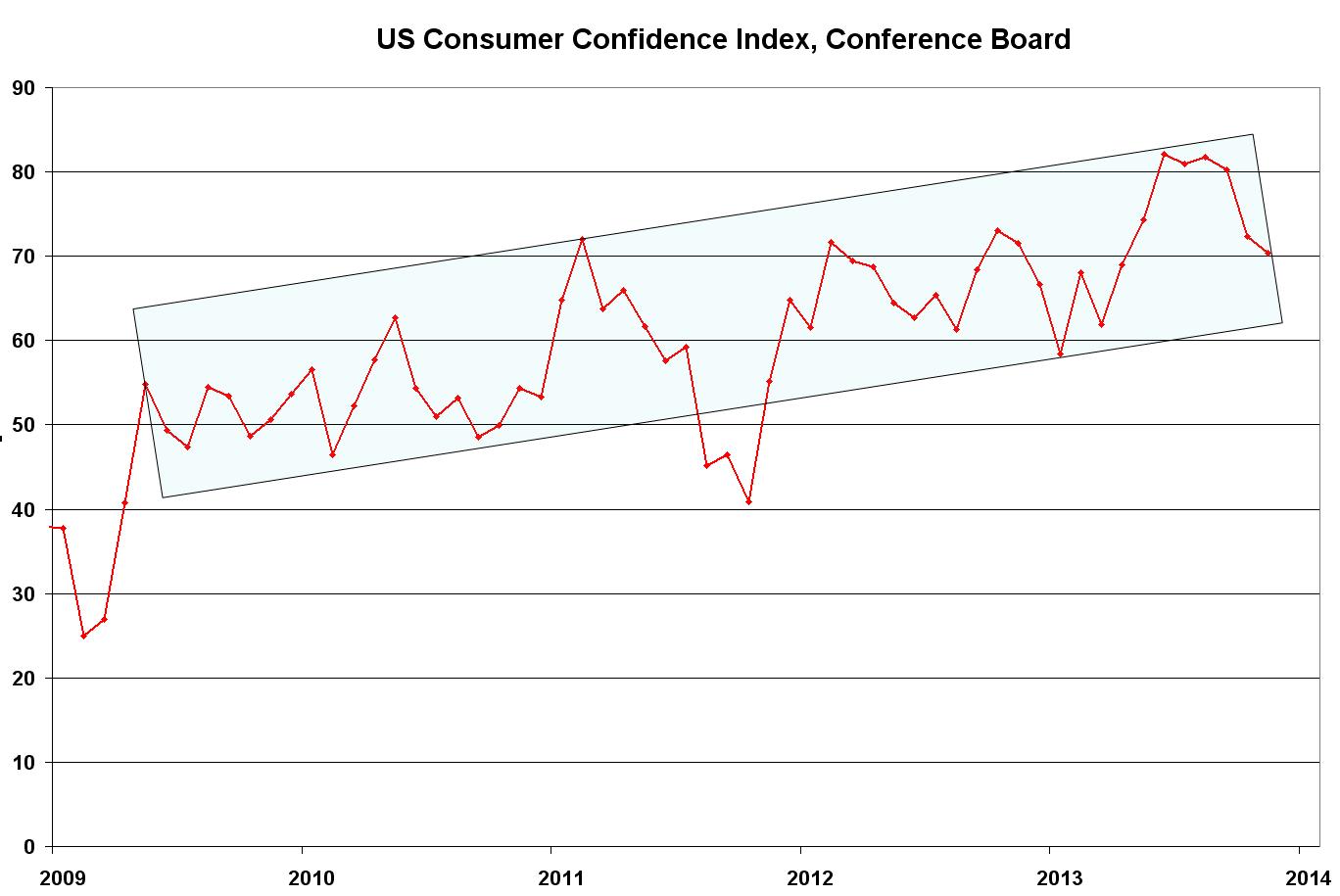

US December Consumer Confidence Index (15:00 GMT). The Conference Board’s index is expected to have risen to 76.5, up from November’s 70.4. Confidence indices have been in a well-behaved rising trend channel since late 2010, with a spike below the channel during the 2011 trouble with the US debt ceiling. This time, the confidence index started falling in October in reaction to the looming US government shutdown and a plethora of negative headlines. As the fiscal issues were solved and disaster averted, the economic numbers have been positive. And with only limited negative market reaction to the US Federal Reserve’s tapering announcement, consumer confidence should show an increase in December, as the consensus expects. Also supporting the case for higher confidence is the Thomson Reuters/University of Michigan’s consumer survey for December, which was published earlier and rose to 82.5 from 72 in November.

I hope 2013 has been kind to you all and wish you all the best in 2014!

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

3 Numbers To Watch: US Home Prices, Chicago PMI, Cons. Confidence

Published 12/31/2013, 01:10 AM

Updated 03/19/2019, 04:00 AM

3 Numbers To Watch: US Home Prices, Chicago PMI, Cons. Confidence

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.