Chinese support of the Euro Zone sovereign debt crisis quickly faded as sticky Greece situation shows no signs of improvement. Meanwhile, can the global QE inspired blow-off rally in risk assets continue apace?

China rides to the rescue – for 12 hours…

Statements out of China in support of buying European debt saw risk appetite slamming back into full speed ahead in Asia and EURUSD on the rebound in the same time frame. Yesterday we had Wen Jiabao indicating support for “getting more deeply involved” in resolving the EU’s debt crisis and these comments were followed up today with comments from the PBOC’s Zhou in China today: “China will always adhere to the principle of holding assets of EU sovereign debt…We would participate in resolving the euro debt crisis.” The comments sent the USD plunging once again in Asia and the Euro rebounded well off its lows to close to 1.3200, though its rebound was far less impressive than the general rebound in risk and in particular, the jump in pro-risk currencies like the Aussie. A look at the likes of the Spanish and Italian 10-year yields suggests that market participants are limiting their speculation on the impact of China’s support to EURUSD rather than the actual instruments that China would supposedly be buying. (and as we are about to post this, virtually the entire rally has been unwound.)

One has to wonder at the real degree of commitment that China can offer from here as signs that it is experiencing its own significant challenges have increased of late, including the central government allowing the local governments to “just rollover” their debts, no doubt because balance sheets are in tatters and tapped out at the local government level after they were at the center of the huge push to expand credit and force further economic growth in the wake of the global financial crisis.

USD/JPY breakout – status please

As risk appetite has pushed higher, JPY crosses have done likewise after recent poor Japanese data and after the Bank of Japan yesterday pledged further easing measures – to the tune of 65 trillion JPY of asset purchases (over $800 billion!), a massive easing program that firmly sees the BoJ outpacing the recent dovishness of the ECB or the Fed. The BoJ also declared an inflation stability goal of 1 per cent. These moves took USDJPY to the cusp of resistance (78.30 area) yesterday and the pair has been trying beyond that level in today’s trade, though there is some lack of fundamental support from the still quiescent bond markets .But the force of the BoJ’s dovishness seems to be outweighing this hindrance for the moment.

The key in the coming few days for JPY crosses is whether that USDJPY former resistance, now support holds (the move has been so sharp that we have to give the support some leniency back down toward 77.75). As well, crosses like NZD/JPY have gotten downright parabolic and are likely to suffer climactic reversals in the short term once the current complacent environment in risk assets fades – plotting the likes of NZD/JPY vs. major equity indices bears this out – more on this below.

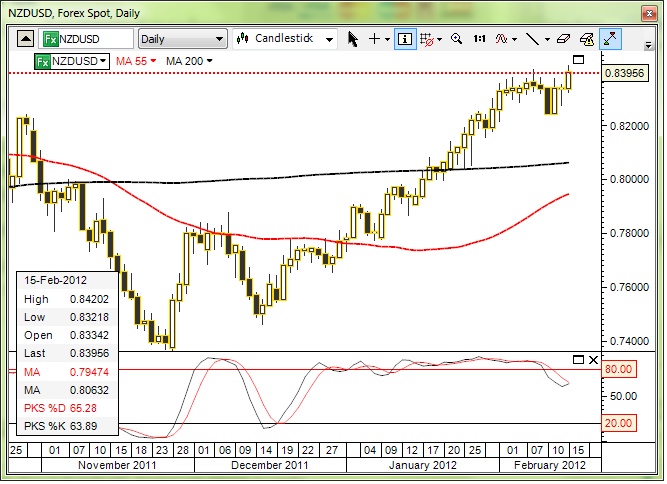

Kiwi blow-off

The NZD is in blow off rally mode if we look at the currency versus any of the major G10 currencies outside the Aussie, after a strong Q4 retail sales report, though we must remember that October still saw a number of Rugby World Cup finals in the country that provided a one-off support early in the quarter. The action in the currency has reached a totally unsustainable trajectory over the last couple of days and is overdue a correction. See NZD/USD chart below.

Chart: NZD/USD

NZD/USD has rushed back to new highs on the most recent statements in support of Europe from China, but also possibly from the QE meme after the BoJ’s most recent easing moves. The momentum is divergent here, but the direction in NZD crosses will be determined by the overall direction of global risk sentiment. NZD/USD" title="NZD/USD" width="605" height="453">

NZD/USD" title="NZD/USD" width="605" height="453">

Bank of England inflation report

Today’s BoE Inflation report seemed largely a non-event, certainly in terms of the market’s reaction. The BoE expressed the hope that the economy is stabilizing and the belief that inflation will fall to 2% by the end of 2012 from 3.6% according to the latest figures. The EUR/GBP resistance at 0.8400 remains emphatically in place after the action today, the question being whether ECB having to step up its balance sheet expansion in the months ahead will drive that pair beyond the recent 0.8220 lows and toward 0.8000 eventually.

Australia to raise taxes

A new Australian law to increase revenues by reducing tax exemption on health care plans for higher earning Australian has gained widespread press and a new hefty tax on mining companies will kick into gear around mid-year. This tendency aggravates the problem in a world of hyper-easy central banks of finding alternative assets in which to invest, as the supply of Australian government bonds is already very small. Already, Australia’s RBA has been forced into creating a special liquidity facility for the banking system to offset the tremendous need for quality instrument for capital reserves.

Looking ahead

As we are writing this, EUR/USD has effectively unwound all of the last bit of rally impetus that it found on the heels of the statements out of China. Risk appetite was clearly stimulated by those self-same statements, but remains in rally mode – a bit of a disconnect, to say the least. The other argument that can be made here is that the BoJ moves from yesterday and resulting weak JPY are merely adding to the “QE to infinity” meme that has driven global asset markets since the dramatic moves by the ECB at its meeting in early December.

As for the Euro more specifically, the Greek deal still doesn’t appear to be a deal as endless details have yet to be worked out and the EU side is still looking for more explicit commitment from Greek officialdom, all while the eventual specter of an election awaits in the months ahead.

Watch out for the latest FOMC meeting minutes for whether dissent to the FOMC rate expectations is more widespread than the consensus suggests. Analysis in the wake of the Jan. 25 decision suggested that the spread of expectations appeared less dovish than the actual statement showed.

Also watch out for the pivotal Australia employment report out in Asia’s Thursday session, as the Australian domestic economy is headed more or less in the opposite direction of the QE/risk appetite inspired rally in AUD.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

12-Hour Euro Stimulus from China Already Fading

Published 02/15/2012, 09:50 AM

Updated 03/19/2019, 04:00 AM

12-Hour Euro Stimulus from China Already Fading

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.