WTI crude oil has returned to near four-month lows on a combination of a continued rise in domestic crude inventories together with the commodity-negative impact of the recovering dollar. We take a look at inventories and production levels.

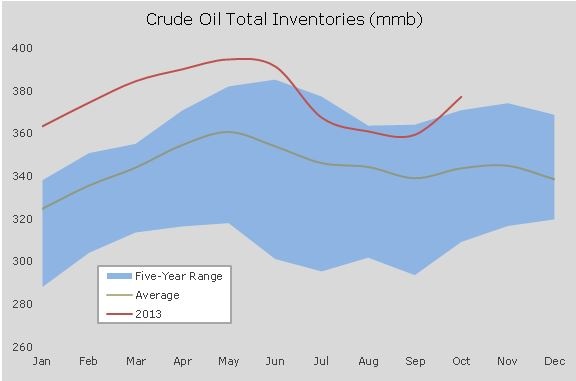

Crude inventories rose by 4.1 million barrels last week, according to data released yesterday by the US Department of Energy. This was the sixth week in-a-row that inventories rose, this time to a total of 383.9 million barrels, the highest since June and some 11 percent above the five-year average.

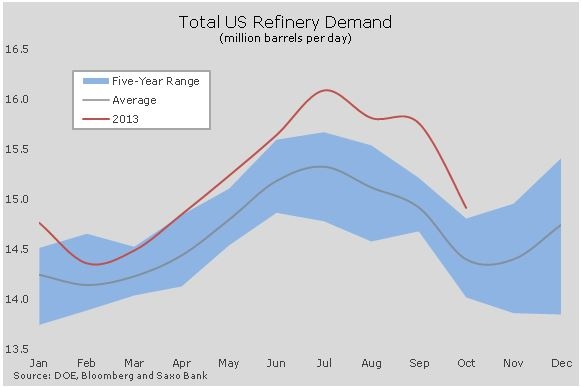

The increase was triggered by the continued slowdown in demand from refineries as they go through seasonal maintenance and turnaround from (summer) gasoline to (winter) distillate production.

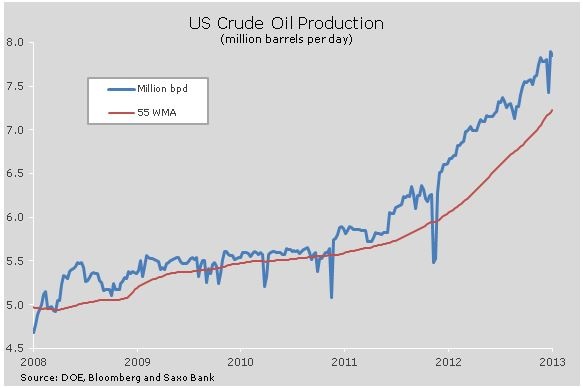

Domestic production continues its upward trajectory with some 7.8 million barrels being produced last week. Such a level of production in the US was last witnessed in 1989.

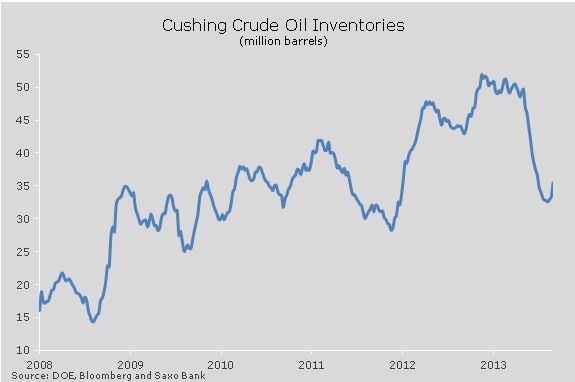

As a result of strong production and reduced refinery demand crude inventory levels at Cushing, Oklahoma, the delivery point for WTI crude, rose by 2.2 million barrels to 35.5 million. This was the biggest jump since December following a long period earlier this year where inventories dropped due to increased pipeline infrastructure taking oil away from the production region towards the Gulf of Mexico.

The lack of demand against continued strong production has resulted in the spread between WTI crude and Brent crude staying elevated. The spread is currently at USD 13.05/barrel, the highest since early April.

The slowdown in US refinery demand witnessed at the moment is expected to be reversed within a few weeks which then should begin to lend some relative support to WTI crude, not least if some of the current supply disruptions, especially in Libya, begin to improve. Brent crude as the seaborne global benchmark would be more price sensitive to such changes in geopolitical risk relative to landlocked and non-exportable WTI crude.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

WTI Crude Struggling As Inventories Rise Amid Low Demand

Published 11/01/2013, 06:07 AM

Updated 03/19/2019, 04:00 AM

WTI Crude Struggling As Inventories Rise Amid Low Demand

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.