There’s been a tremendous amount of discussion among traders and market commentators about the classification of the current trend in equities. Specifically, whether we are in a counter-trend rally (a dead cat bounce) or in the early stages of a new up trend after the March low. As I often do, I turn to volatility to get insight into what’s developing in the financial markets.

Last Sunday I wrote that I believed we were/are in a counter-trend rally within a longer-term bear market. Part of my reason for this is based on the lack of decline in volatility. This will cause many to stop and shout, “But the VIX has fallen from 83 to under 40!” And you’d be right. But I think we must evaluate the path volatility has taken from the viewpoint of its one-year percentile, i.e. where is it within its one-year range. Specifically – has its current decline been similar to prior bear market bottoms or counter-trend rallies?

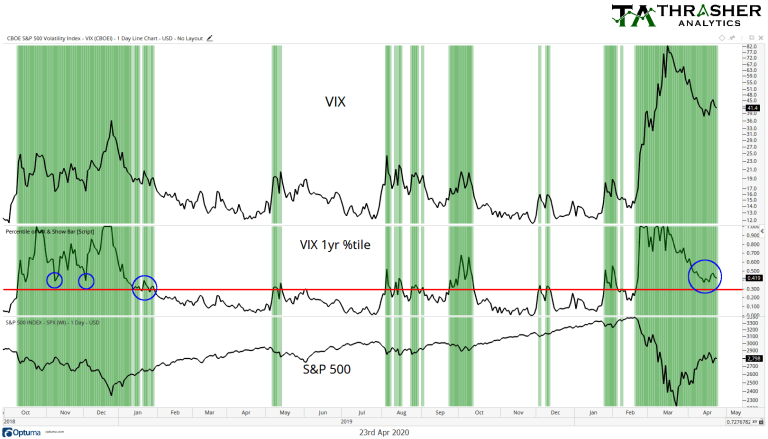

I last wrote about a persistently elevated VIX on March 5, noting that when we see VIX stay at an above-average level, historically we don’t see an immediate bounce in stocks – but instead experience further downside in price. During severe and protracted declines and bear markets, we historically see the VIX stay above roughly the 30 percentile of its one-year range. I’ll be taking a look at last two major bear markets as examples as well as the decline in late-2018.

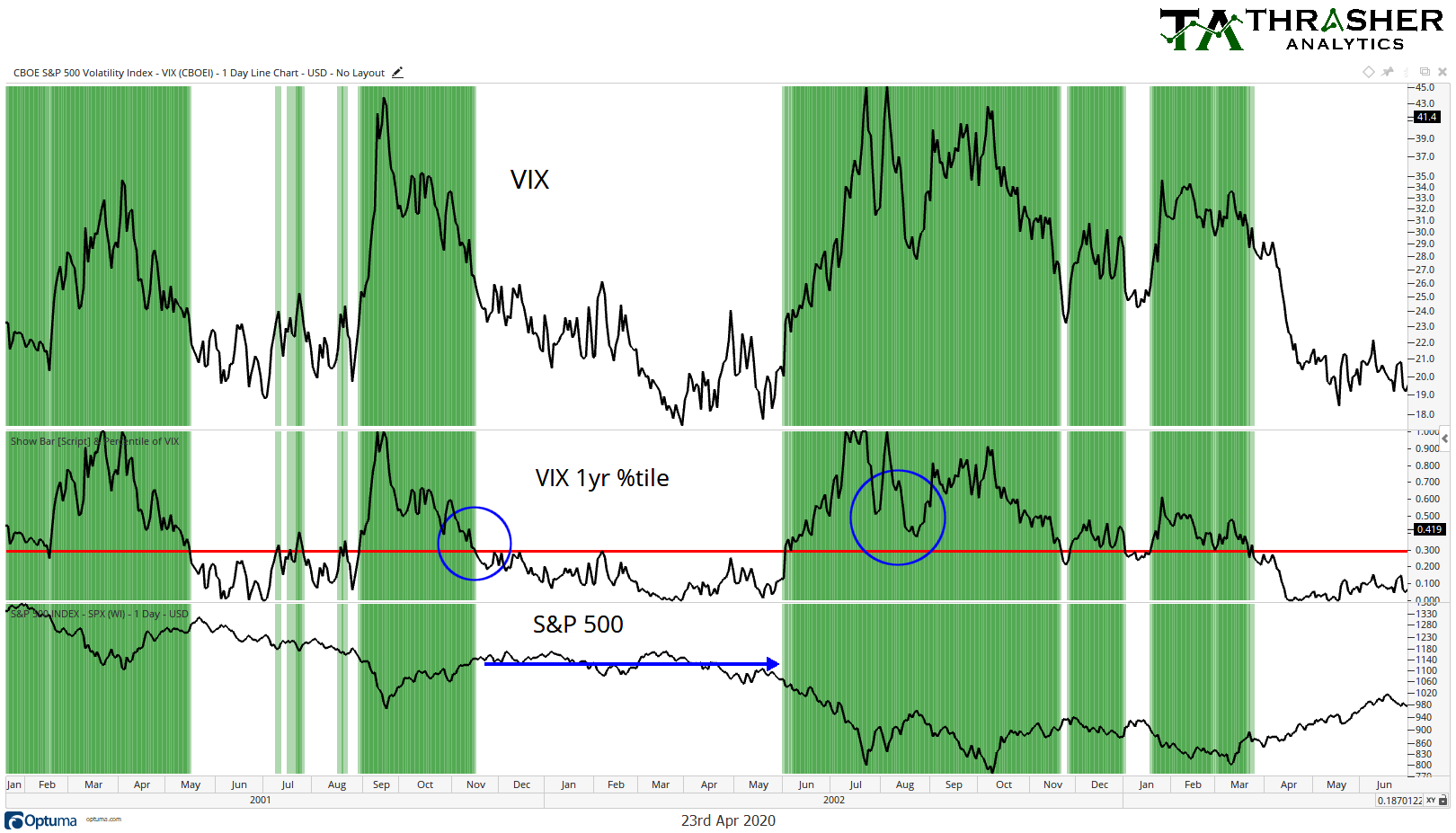

Let’s start with the bear market that resulted from the dot-com bubble. Things didn’t start really moving until late 2001 when we dropped 20% within three months, a similar (albeit not as fast) decline as we have seen today. The VIX fell below its 30-percentile in November and the S&P 500 basically flatlined for seven months. Then, equities started moving materially lower and volatility started rising again. During the next bounce in stocks, what we now know as a ‘dead cat bounce’ in mid-2002, VIX never got to its 30percentile. Instead, volatility stayed elevated, which stocks then responded to by making a new low, eventually bottoming out.

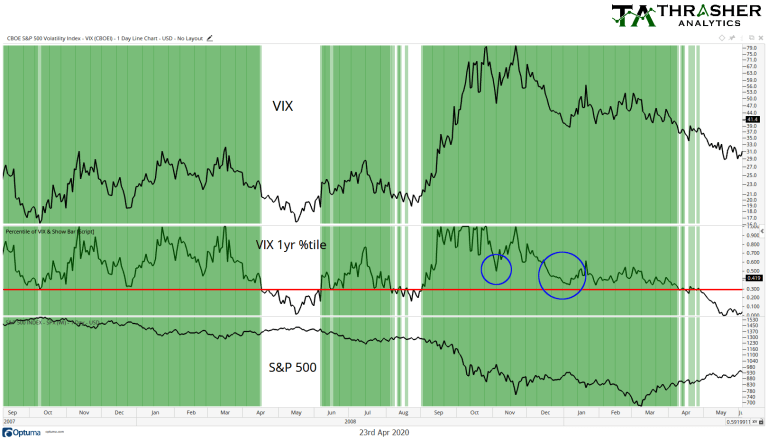

Next, we had the Great Financial Crisis in 2008. Stocks began a fairly slow and orderly decline in early 2008 and the real fireworks didn’t kick off until October, again, when we saw a 20% decline over a three-month period. SPX saw some large counter-trend rallies, from 15% to nearly 25%, before the final March ’09 low. During that time, we never saw the VIX break its 30 percentile until April, after equities had bottomed.

Finally, we have today. First, notice on the left side of the chart that shows the Q4 ’18 decline. During the two brief bounces in equities we also didn’t see the 30 percentile of the VIX break. We could look at the corrections in 2011 and 1998, too. They also had counter-trend rallies that were marked with elevated volatility until the final low in SPX was formed. Today, we have the one-year percentile for the Volatility Index at 0.41, even though the VIX has been cut in half.

By using the percentile of volatility, we can better evaluate its move higher and put the corresponding price action of the large-cap equity index in context. These historical examples are some of the reasons why I believe we haven’t finished seeing downside price action in stocks just yet. However, if we see the VIX continue to move lower as well as several other criteria I’ve laid out in my Thrasher Analytics letter be met then I’ll gladly shift my bias and begin looking for further upside in equities . It’s important to keep an open mind and adapt to the changing price action.

Disclaimer: Do not construe anything written in this post or this blog in its entirety as a recommendation, research, or an offer to buy or sell any securities. Everything in this post is meant for educational and entertainment purposes only.