Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

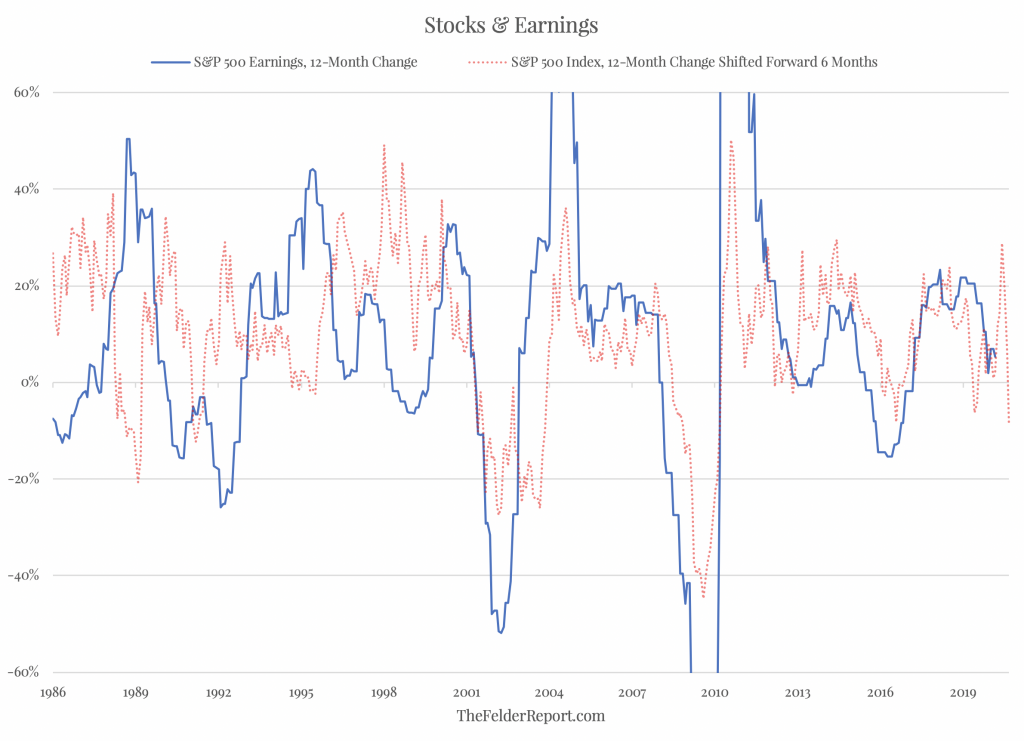

One reason for the record-setting stock market crash we witnessed in the first quarter was a rapid reappraisal of the earnings situation for the S&P 500. As I noted here back in January, stocks were discounting about a 30% jump in earnings growth over the coming six months, a pretty Herculean assumption. When COVID-19 destroyed the prospect of earnings growth for the first half and introduced the distinct probability of a major earnings decline, the S&P 500 was forced to adjust and in dramatic fashion.

However, it appears that the index is now discounting just a 9% decline in earnings going forward. With many businesses shut down completely at present and for at least the rest of the month, this could still prove to be a very optimistic assumption. Earnings growth could easily turn much more deeply negative than that.

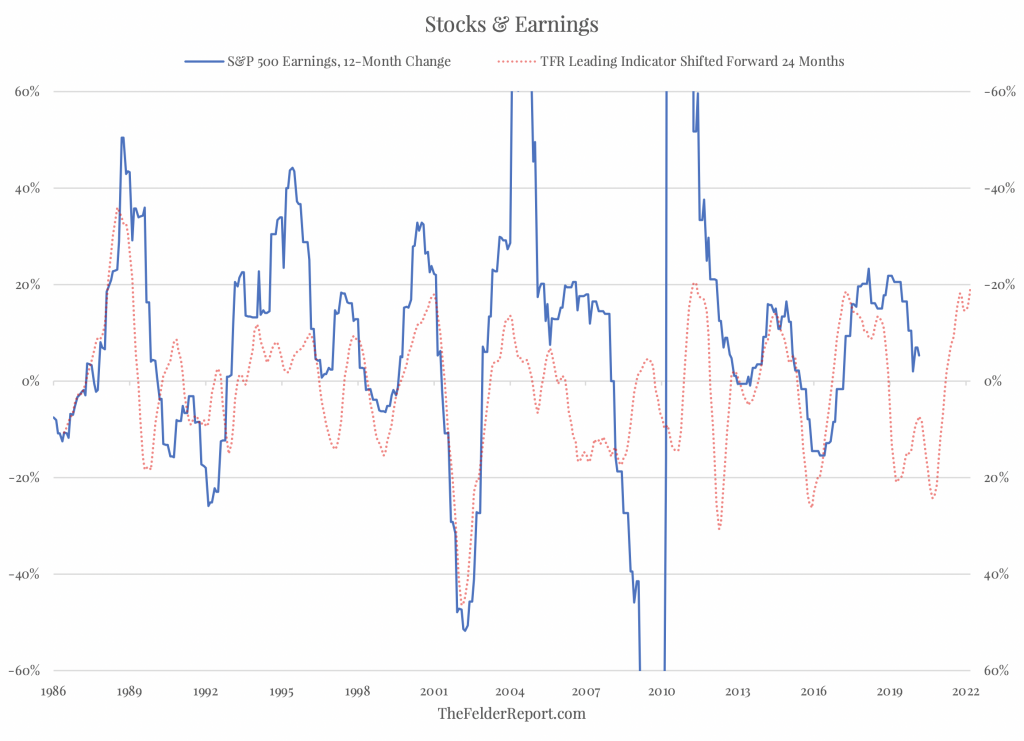

Then again, stocks don’t always have to match the decline in earnings. Obviously, if earnings fall 90%, as they did during the Great Financial Crisis, the stock market doesn’t need to fall 90%, as well (although it did fall 45% year-over-year at its nadir back then). And there is some evidence to suggest that this earnings recession will be relatively brief. My macro earnings model suggests that earnings growth could hit bottom in September or October of this year before rebounding and returning to positive numbers in the first half of 2021.

If stock prices do discount earnings growth by six months in advance and our model is accurate, that September/October bottom in earnings growth would suggest a stock price bottom in March/April, in other words, right about now. This would seem to support the idea that the recent low in the S&P 500 was a sustainable bottom, at least for the next several months.

However, there are a couple of major longer-term issues to consider, as well.

For one, stocks are still very expensive. The Buffett Yardstick remains much closer to its all-time highs than its lows or even its historical average, for that matter.

Second, earnings in recent years could be dramatically overstated and vulnerable to a more sustained decline than our model would suggest.

For these reasons, it probably makes a good deal of sense to maintain a defensive posture, especially if you have a longer-term time horizon and are invested primarily in the index.

Here is a trillion (dollar) reasons why the US economy is likely to hold up until elections: between now and then, Yellen is likely to drain the Treasury General Account (TGA) and...

Stocks finished flattish on the day, but we are moving into the busiest part of the week. Now that Meta’s results are out of the way, we will have GDP and PCE to finish the...

The airline industry is gearing up for what could be a record-breaking summer travel season, if forecasts turn out to be correct. Despite challenges such as the Boeing (NYSE:BA)...

Are you sure you want to block %USER_NAME%?

By doing so, you and %USER_NAME% will not be able to see any of each other's Investing.com's posts.

%USER_NAME% was successfully added to your Block List

Since you’ve just unblocked this person, you must wait 48 hours before renewing the block.

I feel that this comment is:

Thank You!

Your report has been sent to our moderators for review

Add a Comment

We encourage you to use comments to engage with other users, share your perspective and ask questions of authors and each other. However, in order to maintain the high level of discourse we’ve all come to value and expect, please keep the following criteria in mind:

Enrich the conversation, don’t trash it.

Stay focused and on track. Only post material that’s relevant to the topic being discussed.

Be respectful. Even negative opinions can be framed positively and diplomatically. Avoid profanity, slander or personal attacks directed at an author or another user. Racism, sexism and other forms of discrimination will not be tolerated.

Perpetrators of spam or abuse will be deleted from the site and prohibited from future registration at Investing.com’s discretion.