Market prices remains relatively contained despite this weeks scheduled event risk releases. Investors have yet to find firm footing in the second week of the New Year. However, this mornings show and tell from various Central Banks could gives us grounds for fresh market movement, if not, then it will be up to tomorrows highly anticipated non-farm payrolls release to give us further insight into how deep and wide the market can expect the Fed's taper to be. Yesterday's FOMC minutes revealed that members saw "declining benefits" from monthly bond purchases and many of the voters favored QE tapering in 'measured steps.'

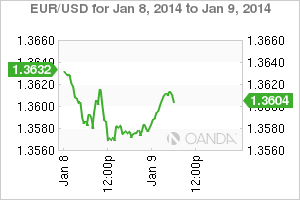

Will the previously united stimulus front get a makeover in 2014? Follow the leader is not a “perquisite” for policy makers anymore. With rate divergence expected to dominate the trading theme in 2014 everything that the ECB or the BoE says and does will come under extra scrutiny. Will the "big" boys come out to play later this morning? No one expects the ECB or BoE monetary policy meeting to deliver any changes in their policy stance this month. Despite both Central Banks remaining price conscious, a theme of higher rates, mainly forced by the pull of US treasuries, could potential threaten global expansion is not something to taken lightly so early in the campaign. No policy maker will be willing to thrown caution to the wind just yet. In this current lower rate environment the Euro-zones peripheral states are taking full advantage of declining yields to issue debt ("demand to match appetite") - Ireland, Portugal, Slovakia and Spain have all stepped up this week. EUR/USD" border="0" height="200" width="300">

EUR/USD" border="0" height="200" width="300">

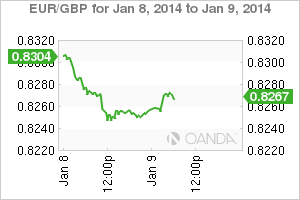

The market expects Draghi to remain balanced in his views at today's press conference; any new innovative language will be kept for a rainy day. As per usual, he will be expected to highlight the required risks surrounding their economic outlook. Perhaps he might comment on the sterilization of the Securities Markets Purchases program? The 18-member single currency remains contained for the time being. Most of the "bears" are probably still in holiday mode shock after last months bullish move higher and the fact that the pullbacks have been rather stingy. The EUR’s use as a “funding” currency is not forgotten, benign inflation, interest rate differentials, a dovish ECB; a hawkish Fed cannot be lost on the EUR's value. Overall, the negatives outweigh the positives. Give it time, the growing monetary policy divergence is expected to become more of a USD supporter over the coming months. EUR/GBP" border="0" height="200" width="300">

EUR/GBP" border="0" height="200" width="300">

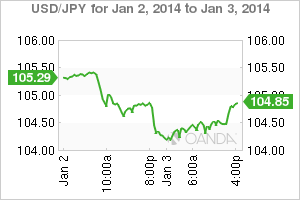

Governor Carney Governor is in a tough position. The BoE has already indicated that its benchmark rate will stay at +0.5% this year. However, relatively stronger data is pushing UK policy makers towards a stimulus exit. Just before Christmas, the BoE indicated that it would "dilute a credit-boosting program as housing prices, sales and mortgage demand all accelerate." It may be time for the BoE to scrap its forward guidance and tell everyone how long they intent to maintain the +0.5% cash rate. UK policy makers have very much underestimated the their own economy's economic strength. The unemployment rate could hit +7% this year rather than in 2016 when first reported. UK fundamentals currently support sterling and this despite the recent -250 point drop from this years high last week (1.6605). Falling unemployment and stronger UK growth prospects continue to find buyers you are bullish GBP over its Euro-zone counterparties. All in all, the varying Central Bank monetary themes for 2014 will provide investment opportunities, especially when policy makers get a stronger handle on how best to implement their own monetary policy. USD/JPY" border="0" height="200" width="300">

USD/JPY" border="0" height="200" width="300">

Thus far, today's surprise is that economic sentiment across the Euro-zone rallied to a two-year high last month. Is this a sign that the regions recovery is finally beginning to take hold? Improved spending and business investment has managed to push the sentiment indicator to finally print 100.0. The uptick was regionally broad based, with the ever important service sector finally moving into positive territory for the first time in two-years. The industrial sector was the second most confident. Coupled with this week's upbeat retail sales data and a stabilized regional unemployment rate (+12.1%) it's becoming very difficult to go all out on a 'bearish' EUR whim. But, as indicated earlier, eventually higher rates will disown the 'single' currency. The appetite for the mighty dollar will be expected to mirror that of US treasuries – higher rates equals a higher dollar. Stronger US data should improve the 2014 “gravitational "asset pull story, and further pressurizing EM/USD positions. Before that, patience remains the order of the day.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

What’s The ECB And BoE To Do?

Published 01/09/2014, 07:06 AM

Updated 03/05/2019, 07:15 AM

What’s The ECB And BoE To Do?

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.