Yesterday’s European Central Bank (ECB) press conference was the ultimate damp squib for those, like myself, expecting its leader, Mario Draghi, to take a more aggressively dovish turn — if not taking any actual measures now or cutting rates, then at least indicating some intended new policy measure and emphasising the risks from deflation.

Instead we got a very passive press conference similar to a number of others earlier this year that saw the euro higher in their wake. The lack of a strong signal from Draghi means that the pressure will continue to the upside on the euro unless we get a stronger set of hints that something new is in the works, or in the event that European data worsens notably. So for EURUSD, it will be up to stronger US data to do the heavy lifting if the pair is to finally find a local top — cue today’s US employment report...

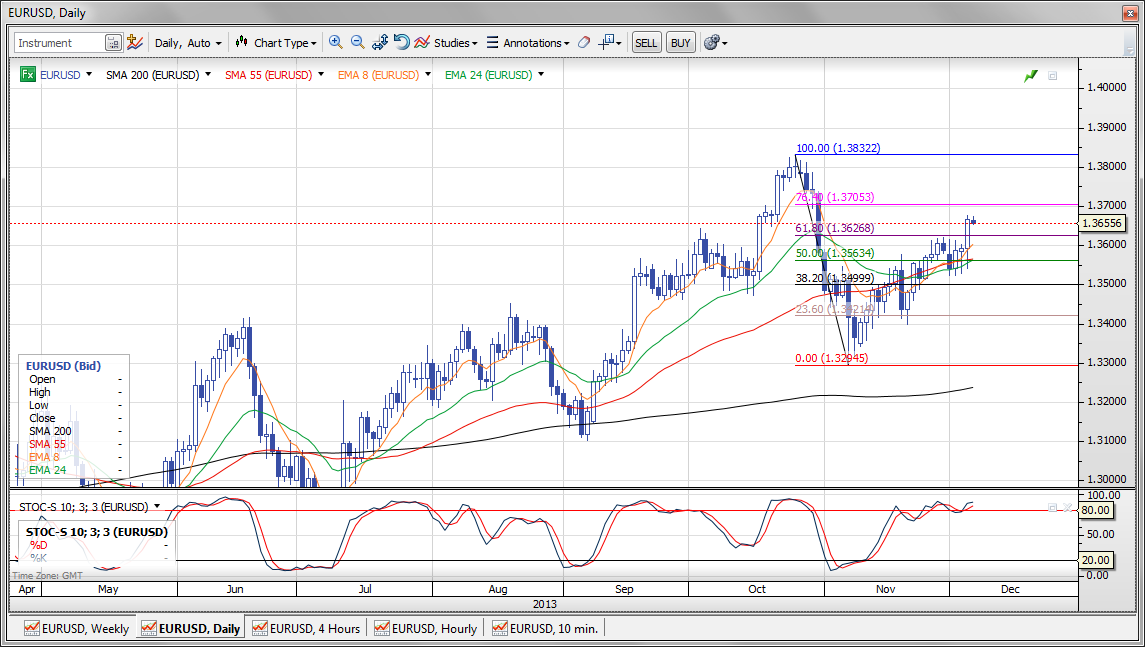

Chart: EURUSD

EURUSD has now pushed through the 61.8 percent retracement level on the shoulder-shrug from the ECB yesterday and appears to be on its way to test the final Fibonacci (76.4 percent) at around 1.3700 and possibly even the 1.3800-plus top if the US employment report today is weak. Only a full reversal of yesterday’s gains today on a strong US employment report can offer the bears encouragement at this point.

Note how the response to the ECB meeting also effectively scotched the GBP rally as EURGBP ripped back higher through the 0.8300/25 resistance area. GBPUSD also looks soft and could be set for a test of the 1.6250/00 support on a strong US employment report.

Japan announced a gargantuan stimulus package yesterday of 5.5 trillion yen to offset the impact of raising the sales tax next year, and it will supposedly have an impact of over 18 trillion yen on the economy. The package will not be offset with debt financing as the government claimed that it could use surprisingly high tax revenues from growth this year to cover the spending. But let’s be honest, the Bank of Japan’s QE is making this possible and it is hard to claim that Japan is showing a compelling move toward fiscal retrenchment after this move.

An advisory group in Japan told the Japanese Government Pension Investment Fund that it should reduce its bond holdings and seek higher returns elsewhere. The bonds would of course be bought by the Bank of Japan. The fund has 124 trillion yen in assets and the recommended allocation reduction would be to 52 percent from 58 percent. More fodder to drive Japanese stocks higher (as long as the JPY remains weak) it would seem.

The two stories above and the continued rise in US long yields should help USDJPY to continue to find support. The pair has survived an assault on the 101.60 area so far and it will be up to the US employment report to trigger a possible go at the highs of the cycle and beyond, provided no ugly surprises are in store.

Looking ahead

In addition to today’s US employment data, we have the release of the inflation measure the Fed has generally preferred — the PCE or personal consumption expenditures price index. The September headline reading came in at plus 0.9 percent year-on-year and thus matched the lowest reading since late 2009, while October is expected to come in at plus 0.7 percent. The core reading is expected to be 1.1 percent in October after September’s reading of 1.1 percent. The 1.0 percent readings in 2009 and late 2010 were the lowest since the data series began in the early 1960s save for an isolated reading in 1998. An especially low reading could give the Federal Open Market Committee (FOMC) reason to delay its decision to taper asset purchases. See a great post from Izabella Kaminska over at FTAlphaville on the debate on whether QE actually causes deflation.

As for the payrolls number itself, expectations are running rather high for this number after the strong reading last month, a number of positive weekly claims number and the strong November ADP reading. A weak number, therefore, offers the most potential response in volatility terms. The latest debate on whether to extend unemployment benefits has now been engaged. If the benefits expire, this will likely help to bring the unemployment rate sharply lower in 2014 due to the effect on the participation rate.

Again today we have the juxtaposition of the Canadian and US employment reports on the same day which offer a make or reverse situation after the USDCAD break higher this week. This is a potential setup moment for whether USDCAD is engaging in a large extension of what has thus far been a very halting and sluggish uptrend since the 2011 lows.

Economic Data Highlights

- Australia Nov. AiG Performance of Construction Index out at 55.2 vs. 54.4 in Oct.

- Switzerland Nov. CPI (0815)

- Norway Oct. Industrial Production and Industrial Product Manufacturing (0900)

- Germany Oct. Factory Orders (1100)

- US Nov. Change in Non-farm Payrolls (1330)

- US Nov. Unemployment Rate (1330)

- Canada Nov. Unemployment Rate and Net Change in Employment (1330)

- Canada Nov. Average Hourly Earnings and Average Weekly Hours (1330)

- US Oct. Personal Income and Spending (1330)

- US Oct. PCE Deflator and PCE Core (1330)