Today’s data calendar has plenty of items, beginning from the final purchasing manager indices in Asia and Europe, and a flurry of US data, most notably the July employment report. While the European data is usually interesting, the fast moving Ukrainian crisis lessens the value of the indicators, and the European Central Bank will not be influenced one way or another by macro numbers, with the possible exception being a further dramatic drop in the inflation rate.

Even though the Federal Reserve Bank’s tapering schedule is also on auto-pilot, at least there is much more uncertainty on the near-term growth rate of the economy and the timing of the first rate hike and frequency of the eventual hikes, which keeps the markets more prone to react to US macro data at the moment.

I would recommend checking the overnight Japanese and Chinese purchasing manager indices for a confirmation that Asia is growing at a healthy pace, followed by a cursory look at the European numbers before today’s main course of US data.

US July Employment Report (12:30 GMT).

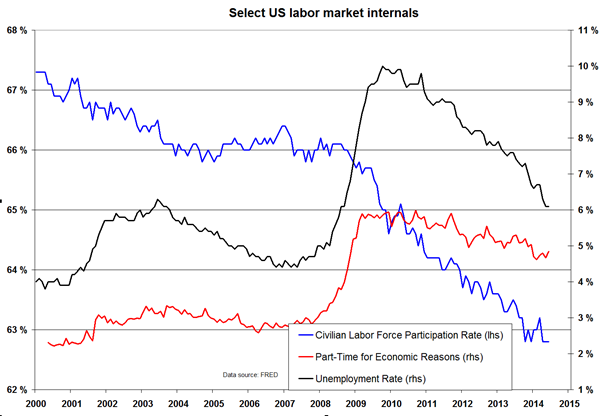

The consensus forecast expects an increase of 230,000 jobs in July, less than the increase of 288,000 in June, but a respectable number nevertheless. The unemployment rate is expected to remain unchanged at 6.1 percent. The civilian labour force participation rate has been steady now for couple of months, but remains at crisis lows. At the same time, the share of people working part time for economic reasons has increased a bit recently, but the trend is still down.

Yesterday’s sell-off in the stock and bond markets started after the second quarter employment cost index from US was published. The index increased 0.7 percent from the previous quarter, a bit more than the consensus forecast of 0.5 percent. That is the biggest quarterly gain since 2007, and the weekly jobless claims were also positive, with the four week moving average decreasing to levels last seen in 2006.

In annual terms, wages and salaries of the private industry workers are now 2 percent higher than a year ago, so there are no real reasons to be scared of runaway wage inflation or a more hawkish Federal Reserve. As yesterday was the last day of the month, the idea of tighter labour markets leading to a tighter Fed was the perfect excuse for over-extended bulls to clear up their portfolios ahead of the today’s employment report.

This suggests that on top of the headline payroll number the most important number to watch will be the average hourly earnings, which increased by 0.2 percent in May and June, and the consensus expects the same growth rate for July as well. It is possible that the number comes in at 0.3 percent, and the weakness in stock and bond markets and the strength of the USD could continue on the same grounds as yesterday, but the stock market corrections now underway probably do not have much downside left.

US June Personal Income & Outlays (12:30 GMT)

Both personal income and spending are expected to increase by 0.4 percent from month ago, and as the chart shows, there is very little drama in the numbers. Following the previous discussion, more interesting will be the personal consumption expenditure price index, which increased 0.2 percent in May, or 1.8 percent from year ago. The core price index, which excludes some volatile items from calculations increased 0.2 percent in May, or 1.5 percent from year ago.

As the chart shows, the price index change has been creeping higher in the past few months. The headline 1.8 percent is getting awfully close to the Fed’s long-term target of 2 percent, but the core index is still way below such levels. But now it does not take much to push the core index to the 1.7 percent level, which would wake up all the investors that the 2 percent level is getting close, and the Fed would have to begin the forward guidancing to a rate hike in the beginning of 2015.

US July ISM Manufacturing Report (14:00 GMT)

The composite manufacturing index is expected to increase to 56.0 from 55.3 month ago. The important sub-indices are all well above the boom bust 50 level, and thus the outlook remains very favourable. It is particularly positive, that the customer’s inventories subindex is unusually low, while the new orders subindex is unusually high. The report is available on the ISM’s website.