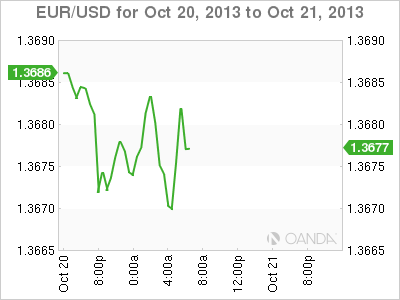

This week the market is playing catch up. A plethora of missed US fundamental releases now get to see light of day beginning with tomorrow's non-farm payroll report. Investors are eager to get their feet wet now that the US fiscal crisis has been temporary been put on hold for a few months at least. Currently, asset classes are straddling some significant key levels helped by the last minute deal in the US to avoid a debt default, lifting the tension brought by the 16-day stalemate. By clearing the worst of the fiscal hurdles there is little on the immediate horizon to derail the global equity rally – however, maintaining the dollars collapse may not be so easy a question to answer. EUR/USD" border="0" height="300" width="400">

EUR/USD" border="0" height="300" width="400">

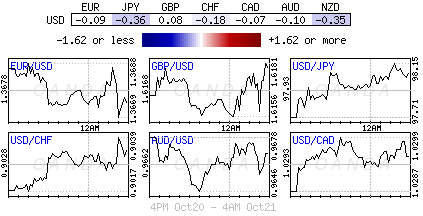

The dollars negative ride has taken a firm grip now that the timing of Fed tapering becomes increasingly more in question. With the debt ceiling temporarily on hold, analysts are finding it difficult to see what could meaningfully derail the recent Emerging Market FX rally into year-end. A surprise in tomorrow's employment report could certainly throw "a cat amongst the pigeons." The markets initial expectations are for a subdued jobs report – if so, then picking up 'carry' in some higher yielding Emerging Market currencies appears the most appropriate course of action in the short-term. EUR/JPY" border="0" height="300" width="400">

EUR/JPY" border="0" height="300" width="400">

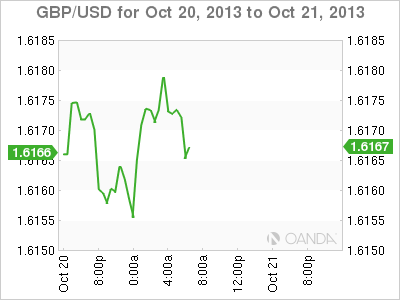

The dollar ended last week beaten down by investors pushing back their expectations of when the Fed might start winding down stimulus. So far this week dollar punters are beginning to shift their stance – looking for a slightly stronger dollar in case there is a slew of good economic US data released. Playing the percentages after such a move is the most prudent of positioning taking. Anything in line with consensus (NFP, +180k, +7.3%) is likely to lead to a broad dollar rally, as expectations for a delay in tapering are once again 'pared.' The key element of the report will be the participation rate - the declining labor force participation is at least partly behind the easing in the unemployment rate last time out. The unemployment rate is arguably the Fed's primary employment benchmark. GBP/USD" border="0" height="300" width="400">

GBP/USD" border="0" height="300" width="400">

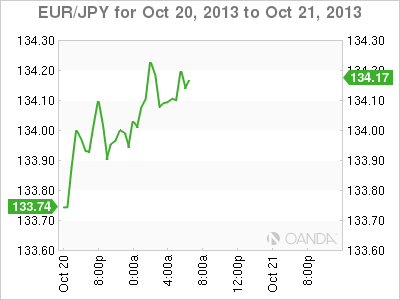

Market interest should remain on the low side until tomorrows delayed US September non-farm payroll report is finally released. Currently the USD is steady, but retracements from last week's steep losses have been rather limited. The 17-member single currency remains below the pivotal 1.3711 resistance (2013 high), while the USD/JPY pair hovers around the ¥98 handle as the market heads Stateside. Many expect the EUR to continue to struggle in the 1.3670-1.3711 resistance area. This region is a combination of the 2004, 2010 and 2013-year highs. Even if the topside is breached the street expect the 2009 high of 1.3739 to be the next line of a "material" defense for the dollar. Despite the USD selloff looking somewhat overdone near-term, the immediate support for the EUR comes in at 1.3647 through 1.3598 – where a lot of wood is required to be chopped. EUR/JPY" border="0" height="300" width="400">

Overnight, Japan saw another trade deficit in September - ¥932b (above consensus) and the 15th consecutive month of deficit. Their current account surplus is also trading down at ¥161.5b in August, down from ¥1.3t in the same period last year. If or when the current account turns into a deficit, Japan will need capital imports to finance it. Under this scenario it would provide for a few headaches for PM Abe's government. Japan would most likely be required to pay more to attract foreign capital/funds. But a current account deficit may also help to weaken JPY – being short Yen is one of the primary crowded trades that the market currently has on.

Currently, the removal of the twin risks of a Chinese hard landing and Fed tapering is providing a significant positive backdrop for risk markets. A strong employment report tomorrow, with positive revisions, will again have investors questioning the possibility of a December taper.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

To Pare Or Not To Pare: That’s The Dollar Question

Published 10/21/2013, 07:51 AM

Updated 07/09/2023, 06:31 AM

To Pare Or Not To Pare: That’s The Dollar Question

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.