At the beginning of each month, we focus on the monthly employment report produced by the Bureau of Labor Statistics (BLS). It is an employment report card – but where should this report card be sent?

Earlier this past week, the FOMC decided not to taper its quantitative easing program – in part due to unemployment levels not reaching its target. Employment growth is the responsibility of the Fed. In 1977, Congress amended The Federal Reserve Act, stating the monetary policy objectives of the Federal Reserve (aka dual mandate):

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.”

How well did the Fed do with this mandate? It is hard to argue that between 1977 and now inflation has not moderated (blue line in figure 1). A decline from 6-7.5% at the lowest in the late 70s (and 10-12.5% 1980-82) to about 2.5% or less for the past 15 years must be considered success.

Figure 1 – Consumer Price Index (all items less food and energy) – aka core inflation (blue line)

Unfortunately, employment growth has also moderated into contraction (blue line in figure 2)

Figure 2 – Year-over- Year Growth of the Labor Force Participation Rate (blue line, left axis)

In view of the pronounced difference in the results for the two mandates it seems appropriate to ask why was the Fed given a dual mandate? From Wikipedia’s discussion of monetary policy:

Monetary policy rests on the relationship between the rates of interest in an economy, that is, the price at which money can be borrowed, and the total supply of money. Monetary policy uses a variety of tools to control one or both of these, to influence outcomes like economic growth, inflation, exchange rates with other currencies and unemployment.

It is generally believed monetary policy influences employment. But there are two problems with the dual mandate.

Problem 1 – Is Unemployment / Employment Influenced by Monetary Policy?

A boringly written Fed study this week concluded:

…. that (the systematic component of) monetary policy can be most effective at controlling inflation, while having little or no direct impact on measures of economic activity. The policy implications of a situation in which a central bank misperceives the policy-relevant trade-off between inflation and unemployment have been studied by Sargent (1999) and Cogley and Sargent (2005).

To add another dimension to monetary policy and employment, this study also concluded:

In normal circumstances, monetary policy could have done more to stimulate aggregate demand and overcome weakness in economic activity, but recently it was hamstrung by the zero bound on nominal interest rates, which forced the use of alternative, less effective policy measures.

There seems to be a very loose correlation (at best) between monetary policy and employment – and being at the zero bound has generally disconnected any significant effect of monetary policy from employment. I believe the reason the Fed focuses more on interest rates rather than employment (when employment currently is the biggest problem) is the Fed does not see any monetary tools to boost employment.

During the subsequent press conference following issuance of the FOMC meeting statement this past week, Chairman Bernanke indicated there were many views on whether monetary policy was currently effective in improving employment – although he believed it was. Here is what Chairman Bernanke said about employment:

The decline [in employment] is in part cyclical, but there is also a longer-term downward trend in participation that aren’t related to the recession. Recently, the decline has been mostly due to the longer trends.

Longer trends?? Chairman Bernanke’s examples included less women working and too many old people not working. Wow! Does he know data shows both old people and women are more positive factors on employment than the population in general.

It is interesting how the FOMC shifted from talking about unemployment and started talking about participation rates. This leads to problem 2.

Problem 2 – The Way Employment is Measured is Wrong

The Fed (and economists in general) believe the way to monitor employment is to monitor employment slack – which they believed was measured by the unemployment rate. That is logical at first brush but unfortunately headline U-3 unemployment as defined by the BLS does not measure slack – but people’s opinion (done by survey based on whether they were unemployed and are actively looking).

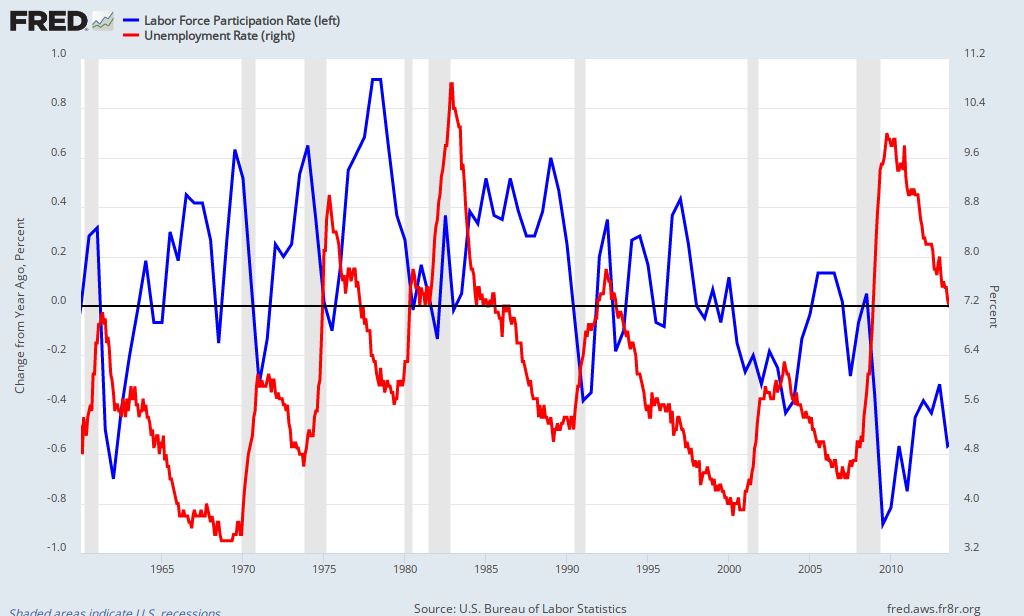

Whether my opinion is right or wrong, there is no argument that employment dynamics have been deteriorating since 1977. Figure 3 below shows:

- Continuous deterioration of the growth of the labor force participation rate since 1977 (blue line, left axis) – with the participation rate growth generally negative since 2000.

- While the participation rate is trending less good, the unemployment rate (red line, right axis) – baring recession spikes – has been improving.

Figure 3 -Year-over-Year Growth Labor Force Participation Rate (blue line, left axis) and Unemployment Rate (red line, right axis)

This begs the question: Why there is a dual mandate?

The answer is obvious.

Congress cannot get their act together to do their part to begin to control employment growth, and are currently demonstrating they cannot even effectively handle fiscal policy which is the correct primary government tool for managing employment. They passed the 1977 dual mandate act to get the employment monkey off their back.

The Fed, on the other hand, is willing to accept any transfer of power from Congress.

There is no question that there is some correlation between monetary policy and jobs, but the effects are secondary. The primary drivers of employment comes from fiscal policy and private sector decisions.

So, monetary policy cannot drive jobs creation – with monetary policy only acting in support of jobs creation. Free market advocates in Congress want little government involvement in jobs creation. Congress appears willing only to regulate employment with taxes and employer burdens (regulations). And market forces have moved more and more to increase the extractive functions of the financial sector at the expense of the productive functions of the Main St. economy, which has been hamstrung by the increasing inefficient distribution of income out of the hands of consumers and into the hands of money hoarders.

Bottom line, it seems no one is responsible for creating jobs except the Fed which lacks the essential tools to create job growth dynamics. Does anyone wonder why jobs recovery since the end of the recession has been the worst in history?

Other Economic News this Week:

The Econintersect economic forecast for September 2013 improved but still shows the economy barely expanding. The concern is that consumers are spending a historically high amount of their income, and several non-financial indicators are weak.

The ECRI WLI growth index value has been weakly in positive territory for over four months – but in a noticeable improvement trend. The index is indicating the economy six month from today will be slightly better than it is today.

Current ECRI WLI Growth Index

Initial unemployment claims went from 292,000 (reported last week) to 309,000 this week. Historically, claims exceeding 400,000 per week usually occur when employment gains are less than the workforce growth, resulting in an increasing unemployment rate.

The real gauge – the 4 week moving average – improved from 321,250 (reported last week) to 314,750. Because of the noise (week-to-week movements from abnormal events AND the backward revisions to previous weeks releases), the 4-week average remains the reliable gauge.

Weekly Initial Unemployment Claims – 4 Week Average – Seasonally Adjusted – 2011 (red line), 2012 (green line), 2013 (blue line)

Bankruptcies this Week: Rural/Metro, FriendFinder Networks (fka Penthouse Media Group), ECOtality

Data released this week which contained economically intuitive components(forward looking) were:

- Rail movements growth trend is continuing to accelerate.

All other data released this week either does not have enough historical correlation to the economy to be considered intuitive, or is simply a coincident indicator to the economy.

Weekly Economic Release Scorecard:

Click here to view the scorecard table below with active hyperlinks