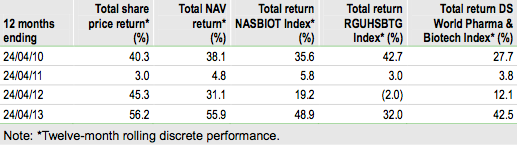

The Biotech Growth Trust (BIOG) has continued its strong track record of outperformance during the past 12 months. Share price and NAV total returns have been 56.2% and 55.9% respectively, which are both appreciably ahead of its benchmark, the NASDAQ Biotechnology Index (sterling adjusted) over the same period at 48.9%. Recent price gains have moved ahead of earnings growth so that average P/E ratios have moved up during the last two years, having fallen for the previous 10 years. However, the manager believes valuations remain attractive in a historical context, he reports that attractive opportunities remain and that, in their view, there is still strong growth potential for the sector.

Investment Strategy: Major And Emerging Biotech

Biotechnology investments in companies at the early stage of development can provide the highest returns over time but also carry substantial risk if drug developments prove unsuccessful. BIOG focuses on these early stage, emerging biotech companies (around two-thirds of the portfolio, with the balance invested in generally larger, established, and profitable companies). For the emerging part of the portfolio, OrbiMed will typically invest during the development process, two to three years before development success (product approval or launch) is likely to produce sales and sustainable profitability. The key to success in early-stage investments is to be able to manage the risk of development failure and in this respect OrbiMed is well resourced with a good track record.

Sector Outlook: Fuller Valuations

The biotech sector has provided a very strong performance during the past 18 months, when the sector has experienced a significant rerating. Initial price gains were broadly matched by earnings increases, keeping valuations near historic lows. Recently, valuations have expanded, making a correction more likely on any set back. The manager is comfortable with current valuations and continues to see attractive opportunities in the space. In addition, the longer term stories of favourable demographics and innovation remain intact.

Valuation: Currently Trading At A Mild Premium

BIOG’s discount has narrowed substantially during the past 18 months and the trust is currently trading at a 1.4% premium (three- and five-year discount averages are 4.7% and 5.5% respectively). However, the premium rating arguably reflects both strong performance and its clear discount maintenance policy. BIOG has been issuing new shares. This should benefit existing holders by stimulating liquidity and reduce ongoing charges by spreading fixed costs over a larger asset base.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

The Biotech Growth Trust

Published 04/29/2013, 11:41 AM

Updated 07/09/2023, 06:31 AM

The Biotech Growth Trust

Strong Performance Continues

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.