Technically Speaking For The Week Of March 18-22

Summary

- The EY granted a short extension for Brexit.

- The housing market received some strong news.

- The markets ended the weak in technically poor shape.

The EU has granted the UK and extension - a short one (emphasis added):

After hours of difficult and sometimes passionate talks, the leaders decided that Britain’s exit date will be pushed back to May 22 if next week Mrs. May can persuade lawmakers in Parliament to accept her plan for leaving the bloc, which they have already rejected overwhelmingly, not once but twice.

If she cannot persuade lawmakers to accept her plan, Mrs. May will get a shorter delay in exiting the European Union — until April 12. But Britain could stay in the bloc longer if it decides it needs more time for a more fundamental rethink of Brexit, as the process is known.

I'm more inclined to call this a temporary reprieve. May 22 is the latest this could drag out - and that's only if May can get Parliament to approve a deal it has twice rejected. We've still most likely kicked the can down the road to April 12. What this really shows is that the EU doesn't want to grant the UK any meaningful slack.

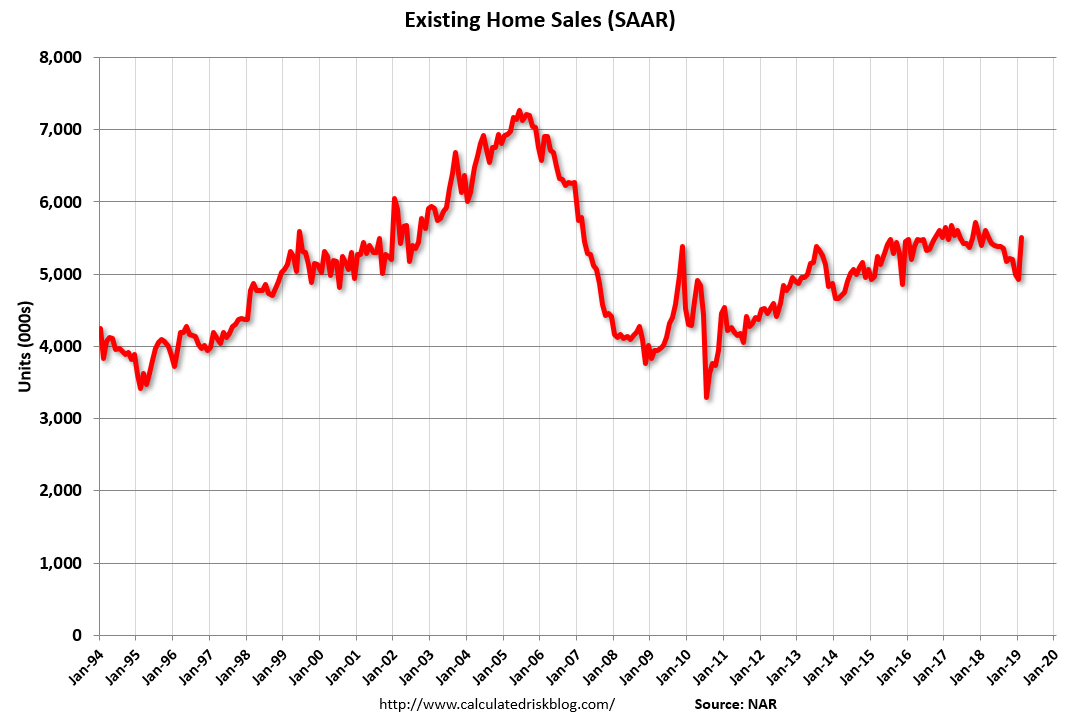

The US has a nice 11.8% pick-up in existing homes sales today. Here's the chart from Calculated Risk:

The housing market has been softer over the last year, so this is some welcome news.

The housing market has been softer over the last year, so this is some welcome news.

The latest Markit Economic data was not encouraging. The EU's headline number is still positive, but it fell 0.6 to 51.3. Manufacturing's PMI dropped from 49.4 to 47.7. New orders have been stagnant for two months and new export orders are down in the last six months. The service sector is still growing; its PMI dropped 0.1 to 52.7. Japan's PMI is negative as are production, new orders, and new export orders.

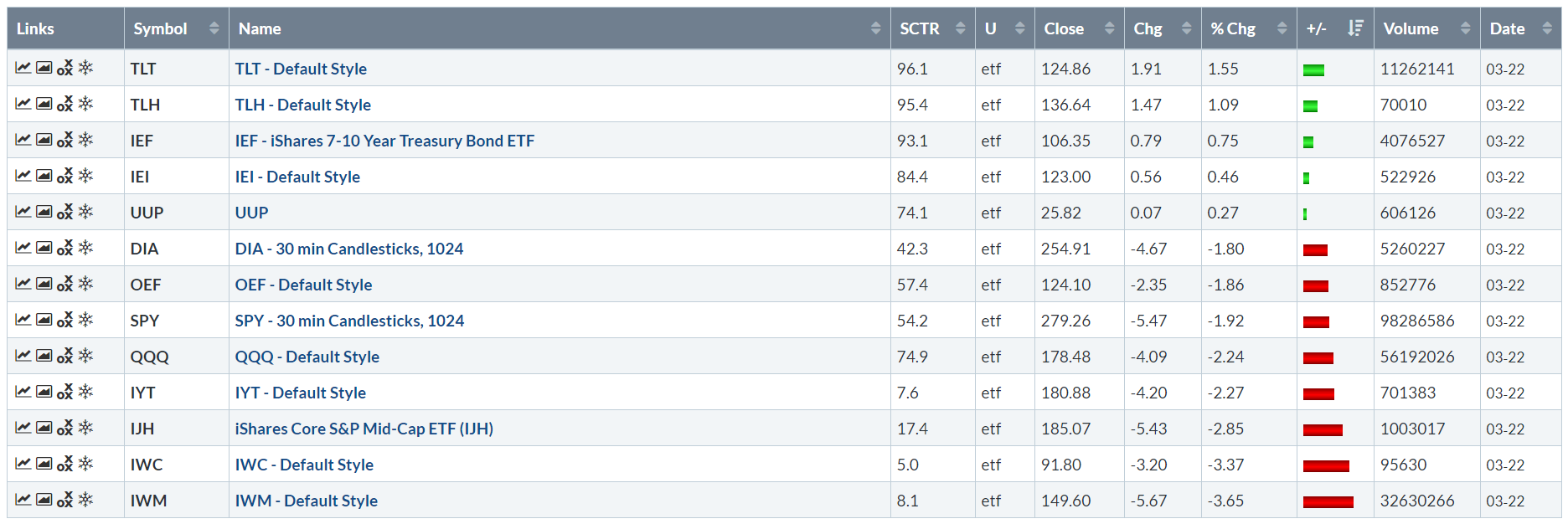

Let's turn to the markets performance table for the day:

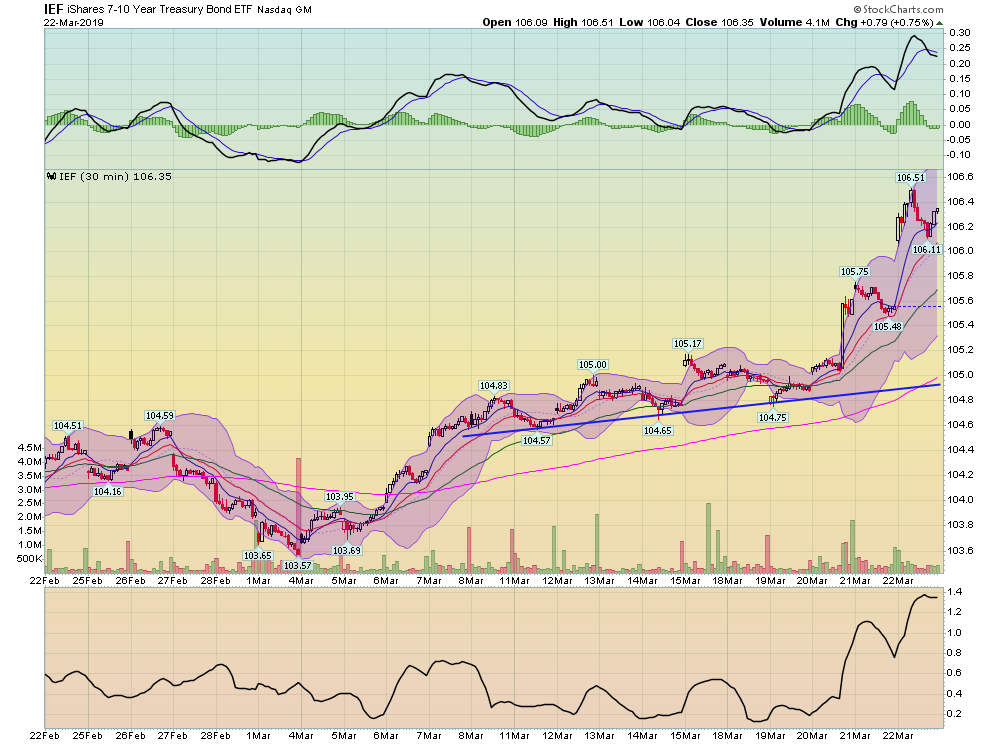

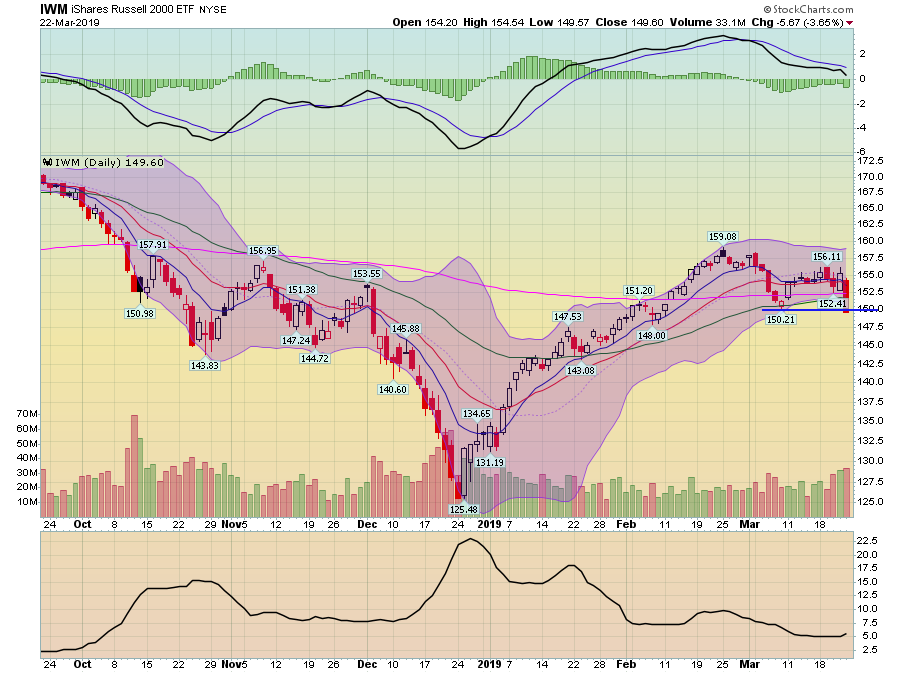

Weak Markit Economics data caused a drop in German bond yields which then hit U.S. bond yields. The long-end of the curve gained 1.55% - a pretty big move for the bond market. On the other side of the risk spectrum, stocks sold off sharply with the IWM leading the way; it cratered 3.65%.

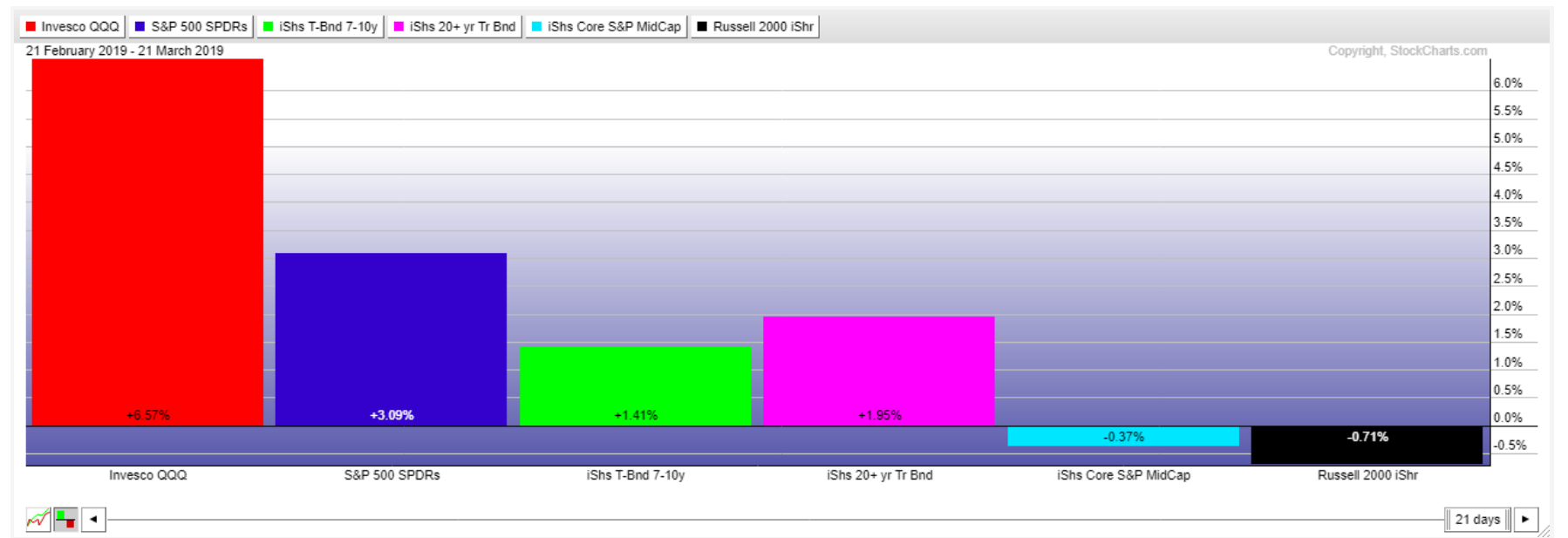

I've been concerned about the market for the last few weeks. The following table shows why:

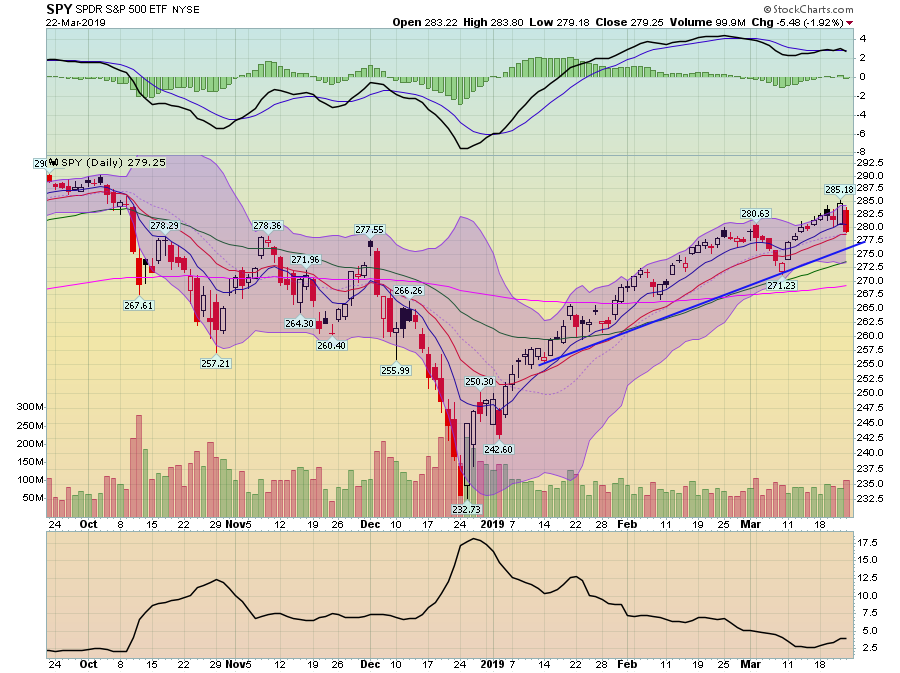

Over the last month, the QQQ and SPY have done well. But so has the Treasury market. However, the mid and small caps have lost ground - which runs counter to the story told by the bigger caps. This dichotomy in performance has been a huge problem for the market. I think today tilted the balance towards the bears.

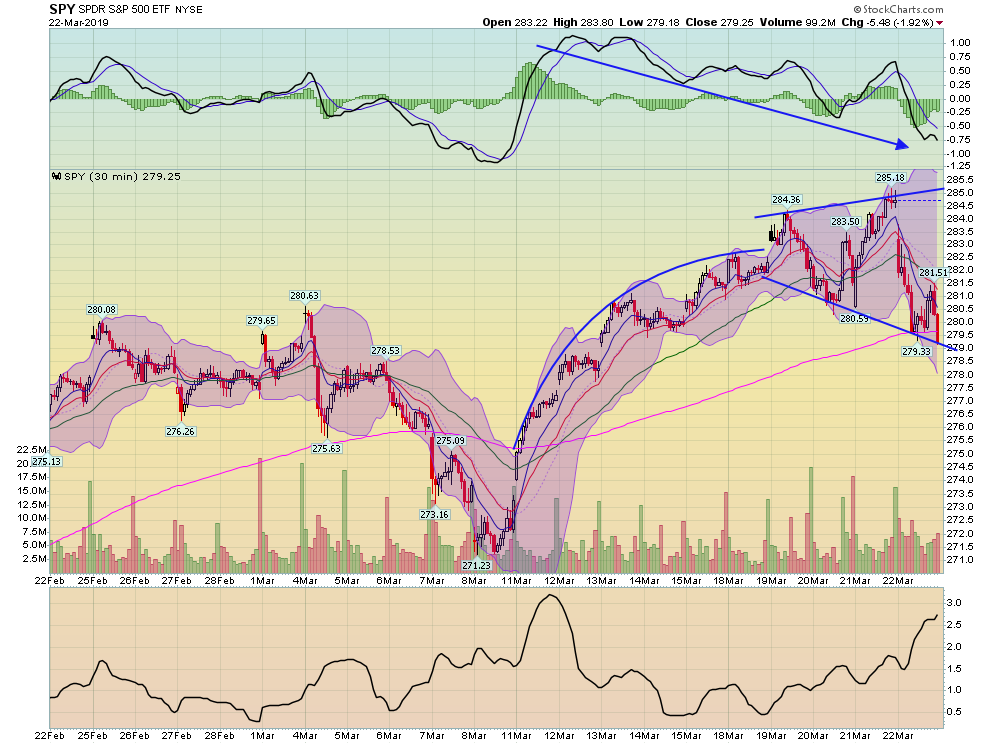

Let's start with today's chart of the SPY:

Stocks sold off all morning, hitting a bottom right after lunch. They caught a small bid in the early afternoon, but then sold off at the end of trading, ending the day near lows. End-of-the-day selloffs are very bearish, indicating traders don't want to hold positions over the weekend.

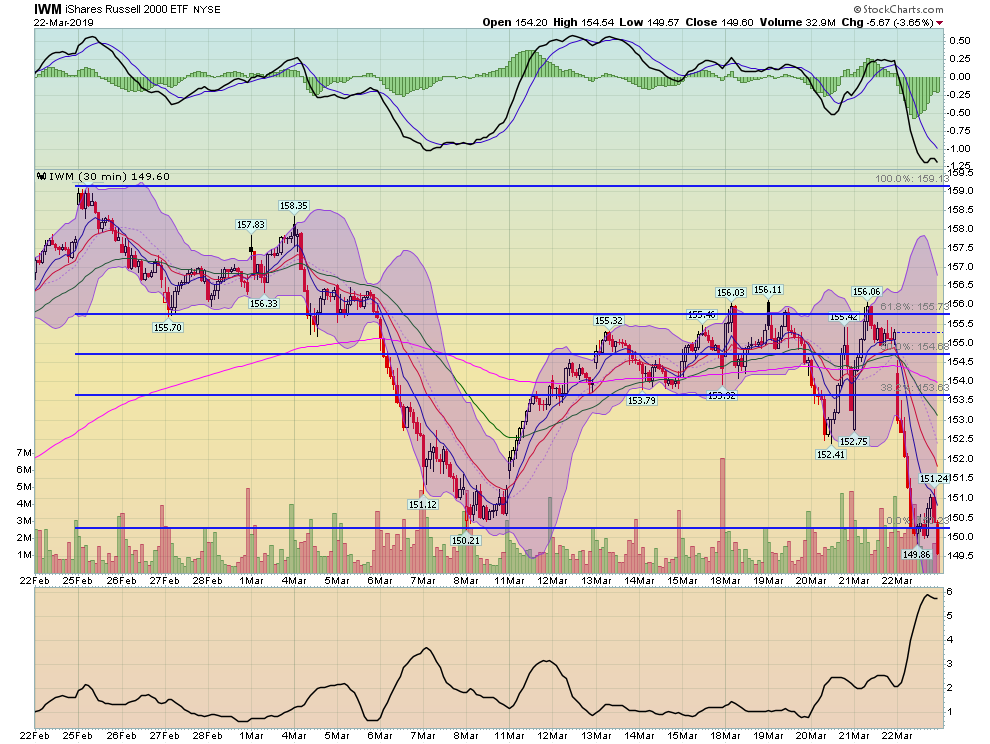

The 30-day charts shows how the market is changing towards the bears:

The IWM rebounded in mid-March but was mired in the mid-Fibonacci range for a few weeks. Today, prices dropped to monthly lows.

The SPY had rallied a bit after the early March selloff. But its prices were trading in a parabolic curve which turned into a broadening pattern - which is usually a topping formation.

Then there's the IEF (7-10 year Treasury bonds) which are in a rally and are near month-long highs.

The daily charts complete the story:

The IWM has fallen through technical support on declining momentum.

While the SPY is still in an uptrend, momentum is getting weaker. At this point, I'd expect the IWM to pull the SPY lower.

So, we end the weak in technically bearish territory. The bond market is rallying, the riskier equity indexes are selling off, and the bigger cap indexes are getting pulled lower.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.