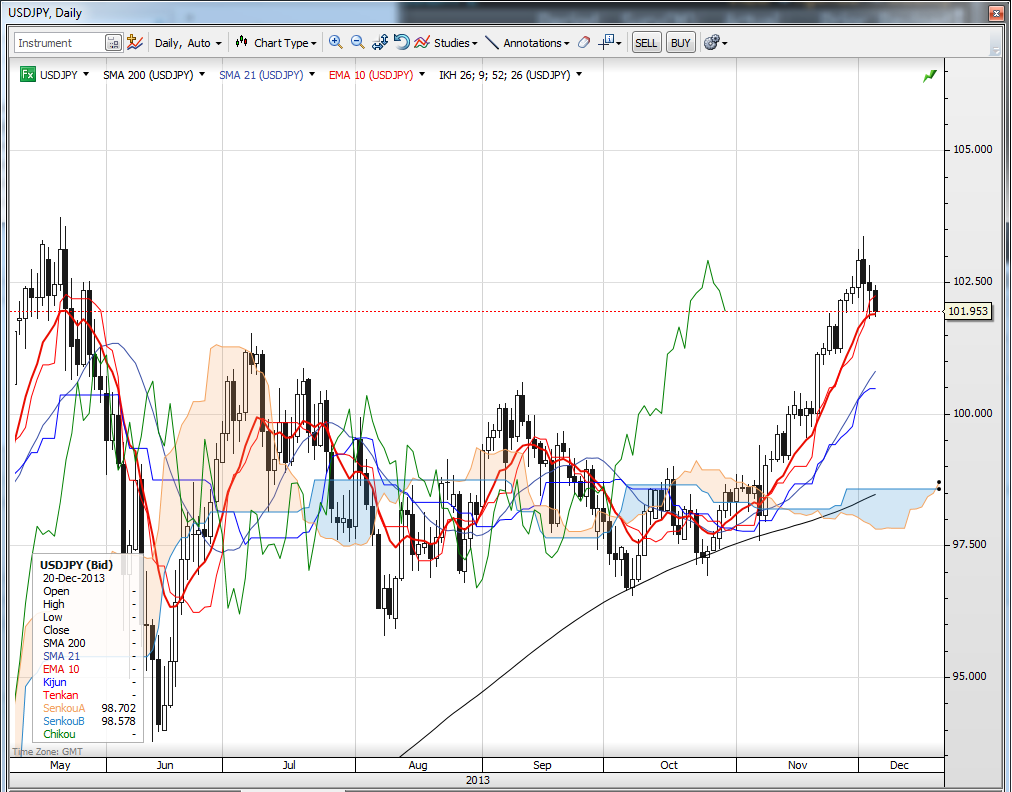

The US dollar rally attempt wilted quickly yesterday in the wake of a weak ISM non-manufacturing survey release, which drooped to a five-month low. This is an important survey for the strength of the US economy, as the service sector is so dominant, so one can easily argue that this release could delay US Federal Reserve taper prospects, though a fat upside surprise on payrolls on Friday might tilt the odds back the other way. The negative data is having the largest effect — no surprise here — on USDJPY, which is pushing at the local lows below 102.00 this morning.

USDJPY waiting on US jobs report

USDJPY is a high beta pair on the prospects for a Fed taper. The local supports come in at the previous salient high at 100.60 and then the 100.00 level. Tomorrow’s US employment release is likely to tell us whether this consolidation is halted in its tracks or whether we are headed toward a dramatic failure of the pair’s recent rally. A strong payrolls number tomorrow would likely see the pair finding a bid tone again.

USDJPY

EURUSD broke above local highs, running through stops in pre-European session hours just before the release of Q3 French employment figures. Those figures incidentally were somewhat supportive of the move higher, as the unemployment rate dropped while the unemployed count rose, though it was virtually unchanged if the downward revision to Q2 data was taken into consideration. This is old data and considering the move in EURUSD came before its release, it is tough to name it as the catalyst for the move higher this morning. It seems more likely the move was flow-induced and we do have that little thing called the European Central Bank meeting later in the day before we can draw any conclusions.

Yesterday’s Bank of Canada statement was rather dovish as the bank sees the risk of inflation to the downside and maintained a steady course otherwise, but with the generally weak USD picture late yesterday and into today, USDCAD was unable to sustain gains. It’s important from here for the 1.0600 area to hold on daily closes if we are to see the pair higher. Watch out for the Ivey PMI later today out of Canada.

Looking ahead

Sterling today will likely be more sensitive to Chancellor George Osborne’s fiscal forecasts than the Bank of England decision, which is not likely to produce a statement of any kind. The UK still has an enormous twin deficit problem, though the market remains happy to look through that for now. EURGBP will be the sterling pair in focus on the other side of the ECB press conference.

It’s all about the ECB today and the US payrolls report tomorrow. As I discussed in my post late yesterday on the EURUSD (when the technical picture looked a bit different than it does this morning!), ECB president Mario Draghi will need to come out firing on all dovish cylinders to put a fork in this EURUSD rally. More important for durable EUR downside will be forward guidance on the prospects for something resembling full-scale quantitative easing rather than tinkering with interest rates, negative or otherwise.

Watch out for the Norges Bank meeting this morning as the NOK is experiencing excessive punishment relative to the other G10 smaller currencies, though the OECD has said it was 26% too strong against the euro. NOKSEK has pushed down through 1.0600 as well to its lowest close in almost 10 years — the valuation is beginning to look absurd there — though we need to see a technical reversal to indicate that the market is discovering this. Perhaps today’s meeting serves as the catalyst?

Considering Norway’s total lack of labor competitiveness at current exchange rates, the easing of inflation concerns and signs that the Norwegian housing bubble is finally rolling over, the Norges Bank is happy to see NOK continuing lower, though the move is beginning to look a bit excessive around the edges. Meanwhile, the Riksbank is concerned about private debt, though the OECD says not to worry.

Economic data highlights

- Australia Oct. Trade Balance out at -529M vs. -350M expected and -271M in Sep.

- France Q3 Unemployment Change out at +31k vs. +15k expected

- Norway Norges Bank announces deposit rates (0900)

- UK Chancellor Osborne announces fiscal forecasts (1115)

- UK Bank of England Monetary Policy Committee Decision (1200)

- US Nov. Challenger Job Cuts (1230)

- Eurozone ECB Announces Interest Rate (1245)

- US Fed’s Lockhart to Speak (1315)

- US Weekly Initial Jobless Claims (1330)

- US Q3 GDP revision (1330)

- Euro Zone ECB’s Draghi to hold Press Conference after rate decision (1330)

- US Weekly Bloomberg Consumer Comfort Survey (1445)

- Canada Nov. Ivey PMI (1500)

- US Oct. Factory Orders (1500)

- US Fed’s Fisher to Speak (1715)

- Australia Nov. AiG Performance of Construction (2230)