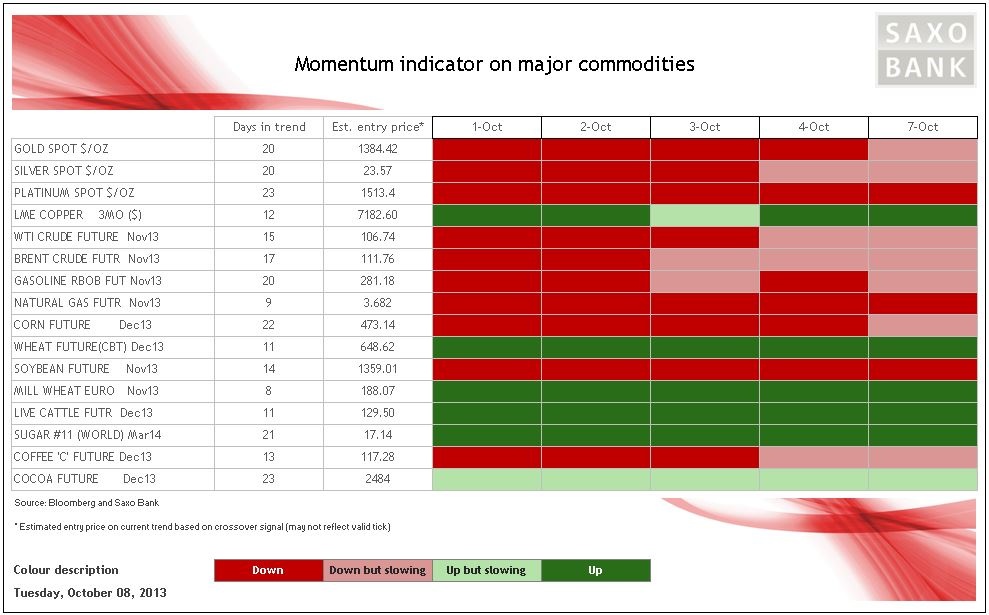

The government shutdown in the US which is into its second week and the potential impasse on raising the debt ceiling have so far only had a limited negative impact on commodities. A solution is still widely expected with the consequences of a failure receiving scant attention so far. Our momentum monitor is currently pointing towards a near-term improved price outlook with negative momentum in both metals and energy slowing over the past couple of days.

Silver bests gold

Gold and silver have both recovered from the selloff last Tuesday as the near-term uncertainty lends support. Silver has managed to out perform gold not least helped by the continued resilience among industrial metals. So far, however, key resistance in gold, today at 1,333 USD/oz being the trend-line from the August peak, has not been challenged and some light long liquidation from disappointed longs has been seen. The upside potential remains valid as long the price manages to stay above USD 1,300/ounce. Support was also provided by the International Monetary Fund this afternoon as it cuts the global outlook for growth this year and next as capital outflows had the potential to further weaken emerging market growth.

Oil selloff over

The selloff in crude oil following the easing of geopolitical tensions seems to have run its course for now with the price of both crude oils recovering despite the current threat to growth from the US political drama. The best performer is Brent crude with the premium over WTI currently at a one-month high. Ample supply in the US due to reduced refinery demand creates resistance for WTI while Brent crude is finding support from a slow return of Libyan oil and renewed far-east demand from South Korea.

Brent crude has subsequently regained positive momentum and has the potential of moving towards USD 111.30/barrel (50 percent over the September to October selloff) while WTI crude remains stuck in a 101-105.40/barrel range.

Wheat pulls corn up

Corn has seen its negative momentum slow after reaching the lowest level in three years. The small recovery seen so far has been driven by spill-over support from wheat which has rallied to a 3 1/2 month high on a combination of strong global US export demand and on expectations of production declines in Russia and Ukraine of high protein wheat as excessive rainfall has cut the planting of winter wheat.

Soft commodities maintain their overall bullish momentum, not least cocoa which has reached a 23-month high as demand is expected to outweigh supply over the coming year. Adding to this we have seen rain delays to bean deliveries from key producers in Ghana and Ivory Coast. Sugar momentum remains positive after the recent break of its multi-year downtrend.

The futures contract for March delivery is approaching the 19 cent/pound area which should offer some resistance not least considering the speculative net-long which would have seen quite an extension over the past couple of weeks thereby increasing the risk of long liquidation.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Signs Of Commodity Rebound As Market Bets On Budget-Deadlock End

Published 10/09/2013, 06:30 AM

Updated 03/19/2019, 04:00 AM

Signs Of Commodity Rebound As Market Bets On Budget-Deadlock End

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.