We issued an updated research report on Stanley Black & Decker, Inc. (NYSE:SWK) on Aug 26.

The industrial tool maker currently has a Zacks Rank #3 (Hold) and market capitalization of approximately $19.9 billion.

Below we discussed why it will be prudent for investors to hold on to this stock for now.

Factors Favoring Stanley Black & Decker

Tailwinds for Top and Bottom Lines: The company serves a vast customer base in various end markets, including retailers, educational, financial, healthcare, commercial, governmental and industrial. Its business segments are Security, Industrial, and Tools & Storage. The diversification helps the company to deal with weakness in some markets, with strength in others.

In addition, it stands to gain from strengthening foothold in emerging markets, favorable e-commerce trend and efforts to innovate products. Also, growing popularity of Craftsman, Lenox, Irwin and DeWalt FlexVolt products as well as benefits from a $250-million cost-reduction program and favorable pricing actions are likely to aid the company. Moreover, development of electronic security solutions and transformational activities will be beneficial.

For 2019, the company anticipates organic sales to rise roughly 4% and adjusted earnings per share to grow roughly 4-7% year over year to $8.50-$8.70.

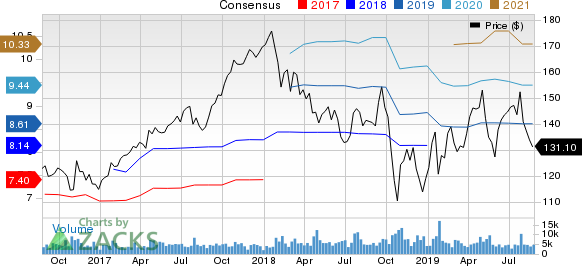

Year to date, the company’s shares have gained 9.5% compared with the industry’s growth of 4.9%.

Shareholder-Friendly Policies: The company effectively uses capital for rewarding shareholders handsomely through dividend payments and share buybacks. It is worth mentioning here that Stanley Black & Decker hiked the quarterly dividend rate by 4.5% in July 2019 while (in 2018) secured the option to purchase roughly 3.2 million shares by March 2021.

In the first half of 2019, the company paid out dividends amounting to $195.3 million and bought back shares worth $9.2 million. It wishes to follow the 50/50 capital-allocation strategy of acquisitions and rewarding shareholders. Dividend payout is predicted to be 30-35% in the long run.

Buyouts: The company has been fortifying its product portfolio and leveraging business opportunities through the addition of assets. It used $676 million (net of cash acquired) on acquisitions in the first half of 2019. Also, buyouts boosted sales by 3% in the second quarter.

In March 2019, the company acquired IES Attachments (now part of the Industrial segment) while bought 20% stake in the MTD Products in January. Prior to these, acquisitions of Newell Tools in March 2017, Craftsman in March 2017 and Nelson Fastener Systems in April 2018 are worth mentioning.

Factors Working Against Stanley Black & Decker

Over-Valued Stock and Earnings Estimates: Using the P/E (TTM) valuation method, the company’s shares currently seem overvalued compared with the industry. The stock’s current P/E multiple is 15.85x, higher than the industry’s multiple of 14.98x. Year to date, the stock’s highest level is 19.08x and lowest is 13.19x. This makes us cautious about the stock.

In addition, the company’s earnings estimates have been declined in the past 60 days. Currently, the Zacks Consensus Estimate for its earnings is pegged at $8.61 for 2019 and $9.44 for 2020, reflecting declines of 0.1% and 0.8% from the respective 60-day-ago figures.

Stanley Black & Decker, Inc. Price and Consensus

Stanley Black & Decker, Inc. price-consensus-chart | Stanley Black & Decker, Inc. Quote

Weakness in Industrial Segment: Stanley Black & Decker predicts that weakness in automotive and general industrial markets will adversely impact its Industrial segment in 2019. Organic sales for the segment are predicted to decline in a low-single digit on a year-over-year basis in 2019.

Within the segment, engineered fastening business’ organic sales are predicted to fall in a low-single digit. Also, the segment's margin is estimated to be down year over year due to external headwinds and lower volume.

Forex & Cost Woes: Geographical diversification is reflective of a flourishing business of the company. However, this diversity exposed it to headwinds arising from geopolitical issues and unfavorable movements in foreign currencies. In the second quarter of 2019, forex woes adversely impacted its sales growth by 3%. Also, commodity inflation and tariffs are issues for the company.

These three headwinds were the prime reason behind a 4.4% year over year rise in its cost of sales in the second quarter of 2019. Stanley Black & Decker predicts that adverse impacts of tariffs, foreign currency woes and commodity inflation will affect results by $390 million in 2019, higher than the previously mentioned $340 million.

Stocks to Consider

Some better-ranked stocks in the Zacks Industrial Products sector are Graham Corporation (NYSE:GHM) , DXP Enterprises, Inc. (NASDAQ:DXPE) and Roper Technologies, Inc. (NYSE:ROP) . All these stocks currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the past 30 days, earnings estimates for these stocks have improved for the current year. Further, earnings surprise for the last reported quarter was 100% for Graham, 4.29% for DXP Enterprises and 0.99% for Roper.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Roper Technologies, Inc. (ROP): Free Stock Analysis Report

Stanley Black & Decker, Inc. (SWK): Free Stock Analysis Report

DXP Enterprises, Inc. (DXPE): Free Stock Analysis Report

Graham Corporation (GHM): Free Stock Analysis Report

Original post

Zacks Investment Research