As noted yesterday, what’s typically behind these hopes about “green shoots” is a central bank, more often than not more than one central bank. In 2019, the Fed’s pause isn’t the only supposed dovish turn. The ECB is back at it, having canceled its rate liftoff. And the PBOC is doing things that nobody ever cares that much to truly understand.

Maybe it takes time for all that to work its way into the economic mix. Economists feel monetary policies come with a lag, which is why central bankers (who are all Economists) always have to look ahead. If only they were better at doing so.

Then again, perhaps monetary policy isn’t very accommodative no matter what the setting, or change in setting. Dovishness makes a nice news story, plays really well on CNBC, but that doesn’t necessarily mean it can fix what ails the actual economy. Sentiment isn’t enough; all central banks offer is sentimental management.

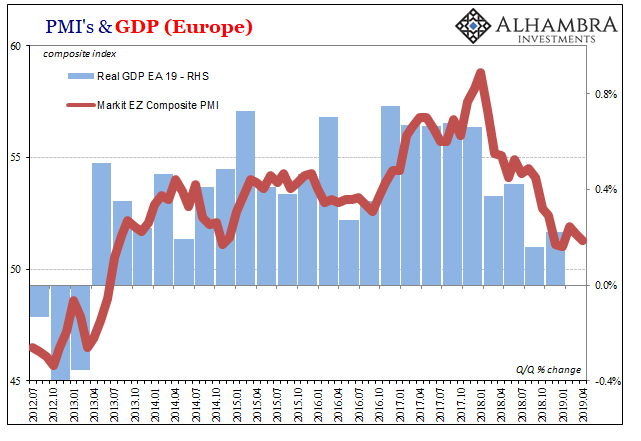

As for the green shoot narrative, IHS Markit just broke out its brown crayon. The flash PMI’s for all the key economies around the world are the opposite of vibrant.

Starting in Europe, in April the composite PMI (manufacturing and services combined) was just 51.6. Rather than rebound from the plunge in the second half of 2018, for the four months of 2019, it is stuck at around the same low level.

Not getting worse, not yet, anyway, isn’t quite the same thing as what one imagines to match the optimistic rhetoric.

Germany’s composite PMI picked up to a two-month high largely because the manufacturing piece increased in April, though not really. The final reading for March 2019 was a recession-like 44.1. This month, it “improved” to 44.5. The German economy moved by its manufacturing sector, its manufacturing sector moved by global trade. Euro$ #4 is most visible here in its goods economy.

The rest of the system is merely following down the hole.

As it is in Japan. At 49.5, Nikkei’s flash manufacturing PMI was below 50 for the third consecutive month. The press release for it for some reason attempts to mix in some good news with what is the real news. “Weaker demand from domestic and international markets persists, leading output to fall further…but manufacturing employment remains resilient.” The Japanese aren’t really known for mass layoffs in the face of contraction.

The subindex for new export orders in Japan hasn’t been this far below 50 for this long since Euro$ #3 three years ago. More and more, it looks like at best a repeat of that situation.

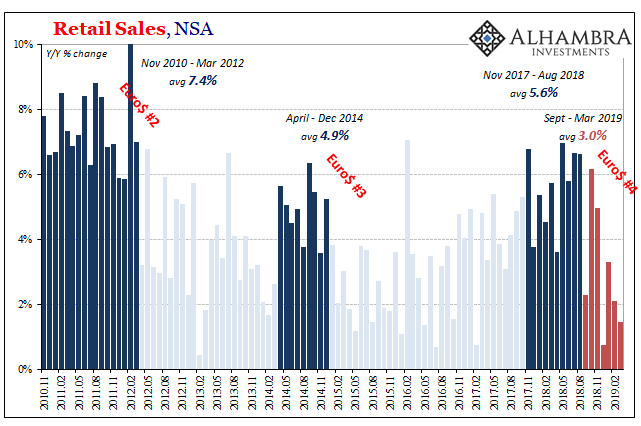

This includes the United States. First “they” said the US would decouple, a boom so strong it would easily withstand “overseas turmoil.” Now they are down to hoping that renewed central bank dovishness will deflect growing weakness back the other way.

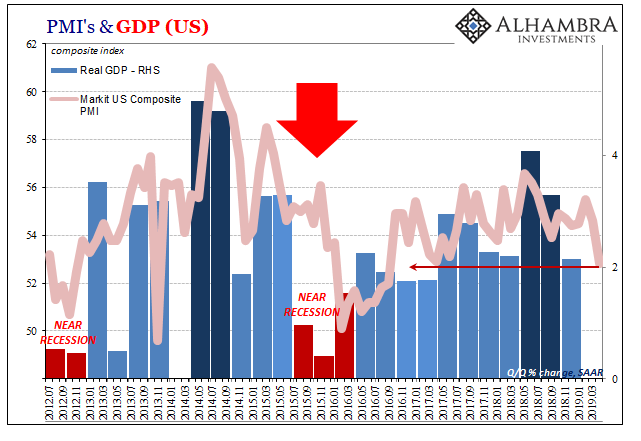

Instead, on the same day the Census Bureau reports the fourth straight really bad retail sales number, Markit puts its composite PMI for the US at a 31-month low. At 52.8, down from a final reading of 54.6 in March, this would further confirm how weakness is both getting serious and becoming widespread.

The manufacturing sector continues to be suspect, that particular PMI 52.4 for the second month in a row. It is hardly the same level of weakness as we find in Europe and Japan, but that simply means, as it has in each of these mini-cycles, that time, as well as intensity, are variable factors. The overall direction, globally synchronized downturn, is not.

Instead, it was the service sector which prompted the large monthly decline. From 55.3 last month, the flash services number for April was 52.9, the lowest in more than two years.

Combined, it all pictures a global economy still on the downswing some four months, one-third of the way, through 2019. Maybe dovishness does need more of a lag to show up. Then again, bond and money markets aren’t betting that way. They’ve been consistent for over a year in warning that the economic trajectory was turning. Globally. More and more the data this far into 2019 keeps confirming the view.

And as monetary conditions continue to be tight no matter what central banks do, the macro data continues to consistently display the economic results.