OTCM provides regulated marketplaces offering a cost-effective solution for targeting U.S. investors. Issuers wanting an informed and efficient U.S. market face less regulatory complexity and so incur lower costs. Its advanced electronic network model is low cost to traders by eliminating the middle man. This model, combined with high-quality, advanced- technology service has seen strong growth especially from international issuers. Despite challenging market conditions, it has grown revenue, much of which is non-market sensitive, every year since 2007.

Marketplaces Platform

OTCM is not an exchange, it is a technological network providing an “Open, Transparent and Connected” market saving issuers compliance costs and traders dealing costs. Issuers range from U.S. SMEs to global names such as Roche. OTCM offers three tiers of marketplace, with its highest-tier companies having exchange-comparable standards. OTCM generates revenue from: (i) OTC LINK ATS trading services (33% of 2012 revenue), mainly from charging brokers fixed monthly subscriptions with some variable month user and usage fees; (ii) market data licensing (39% of 2012 revenue), mainly from monthly fees from distributors such as Bloomberg; and (iii) issuer services (28% of 2012 revenue), mainly from annual information and communication services contracts to issuing corporates.

Why Issuers Use OTCM

OTCM’s marketplaces provide issuers with simple, technologically-advanced, regulated marketplaces, well connected to the investor and press communities, at a low cost. For broker-dealers, the SEC registered ATS trading systems are exchange equivalent in service but have lower intermediary costs.

The Key Sensitivities

The key sensitivities are regulation and technological development. Both present OTCM with challenges and opportunities. Current proposals to ease some of the rules for small U.S. companies could see greater demand to have their securities traded. There are market volume related revenues, but these are quite modest.

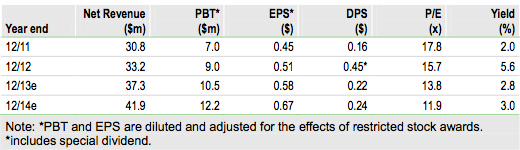

Valuation: Not Paying Full Value For Growth

OTCM is very profitable (c 40% ROE), has strong forecast growth (c 16% CAGR 2012-14) and generates cash (over $4m+ pa), and yet it trades on a 2013 P/E of just 14x. We believe this is partially due to low stock liquidity. Our conservative valuation approaches indicate a fair value of around $10.7.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

OTC Markets Group

Efficient U.S. SecuritiesMarketplaces

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.