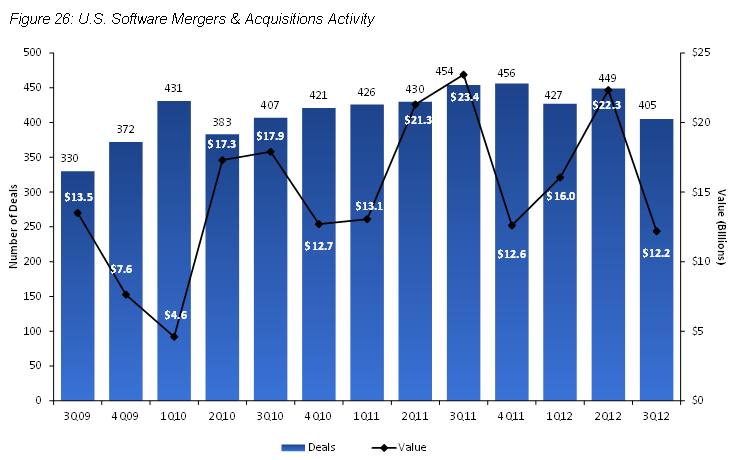

Oracle (ORCL) is still on the SaaS, Cloud acquisition move. Technology in SaaS and Cloud areas are expected to lead the M&A market for 2013. Today SaaS and Cloud are viewed as mainstream strategic imperatives for software vendors improving product and service areas. Third quarter SaaS company acquirers have included Oracle as well companies Autodesk, Mastercard, Rackspace, Citrix, Athenahealth, Google and IBM. SaaS accounted for 23.2% of all software industry acquisitions in 3Q12. Enterprises such as Oracle have adapted to social business solutions and more rapidly adopting initiatives. SaaS and Cloud will be used to strengthen Oracle’s strategies, product and services. IT spending forecasts for growth predicted a recovery in 2013 followed by accelerating growth in 2014

2013 M&A Growth

M&A is Oracle’s fastest growth path for 2013. In 2012, SaaS and Cloud was growing to more than 15% of global technology M&A deal volume. The company is one of the most persistent cloud organizations in the industry. Oracle agreed to buy Eloqua Inc for Marketing SaaS with social networking, which went public, for $871 million and purchased Taleo. SaaS included Oracle’s completed $2 billion purchase of Taleo which offerings of human capital through recruitment and managing talent through social networking and collaboration. The latest acquisition, Acme Packet (APKT) for $1.7 billion. It’s cloud strategy is focused on delivering enterprise-class applications and middleware however the customer wants. Oracle's integration of SaaS acquisitions in 2011-2012 have developed a full portfolio of SaaS services. Valuations for 2013 will be further measured on Oracle’s ability to sell its entirely new cloud applications to new customer markets. they’ve never sold to before. “ To help accelerate their adaptation to the innovation that technology is enabling in many industries, non-technology buyers increased technology-buying activity all year, ending with 10% of full-year aggregate value and 12% of volume.” via EY Report.

SaaS and Cloud Technology

Ernst & Young states that these areas specifically will be a hot bed for activity. "The macroeconomic pressures that returned in late 2011 held down global technology M&A activity in 2012. But, that pressure also helped clarify what's important. "We saw growth in the strength of transformative megatrends — social-mobile-cloud, big data analytics and accelerated adaptation — while the really big-ticket deals pulled back. Heading into early 2013, the short-term outlook suggests a soft couple of quarters but the long-term outlook for technology M&A remains strong, as both technology and non-technology industries have an ongoing need to adapt to disruptive technology innovation. Looking ahead: mixed signals for technology M&A with possible recovery in late 2013 In 4Q12, technology M&A data gave mixed signals, suggesting that the market might be approaching a near-term bottom. However, the report noted 22% growth in mid-priced deals (between US$100m and US$1b) in 4Q12, which suggests that the broad-based need for transactions that help companies accelerate their adaptation to transformative technology innovation has not changed. What has changed is that macroeconomic uncertainty increased throughout 2012 at the same time that many valuations increased. This was demonstrated by the 16% increase in the NASDAQ, driving up the valuation risk inherent in large transformative deals. We expect the first quarter of 2013 will be seasonally down. Overall we expect a relatively stable volume of strategic deals in 2013 as compared with 2012, but with growth weighted more toward the second half of the year." via Joe Steger, PWC.

The report also highlights Cloud and SaaS as leaders due to strong growth trends:

"Cloud/ (SaaS) deals dominate M&A: Largely on the strength of SaaS growth, the cloud/SaaS megatrend "ran away" from the rest of the pack of deal-driving trends in 2012, growing to more than 15% of global technology M&A deal volume. Cloud/SaaS deals ranged from supply chain management, marketing and retail SaaS to cloud-oriented networking gear. Big data analytics deal volume saw similar growth, but from a smaller base."

E&Y Global Top 10 2012 Deals List:

Cisco_Systems, Inc. acquired NDS Group Ltd.

SAP_AG acquired Ariba, Inc.

CGI_Group Inc. acquired Logica_plc

Dell_Inc. acquired Quest Software, Inc.

ASML_Holding NV to acquire Cymer_Inc.

Micron_Technology, Inc. to acquire Elpida_Memory, Inc.

ARRIS Group, Inc. to acquire Motorola_Mobility Holdings, Inc.

RedPrairie Corporation acquired JDA Software Group Inc.

Oracle_Corporation acquired Taleo_Corporation

The Blackstone Group LP acquired Vivint_Inc.

Rapid adoption contributes to strong growth factors. The volume of deals continues to remain steady. Growth in strategic technology deals by Cloud, SaaS and other leading trends will continue to also move forward innovation through the industries. These other trends include smart mobility, social networking, big data and analytics.The major catalysts driving cloud deals forward in 2013 are enterprise software companies’ need to redefine their business models and find sources of sticky revenue that can replace for many of them, dwindling maintenance revenue streams. Knowing that the annuity model of cloud computing works best with multiyear payments required at the beginning of a customer engagement, enterprise software companies are looking to strengthen this area of their product portfolios. Third, the faster cloud acquisitions can be integrated into their legacy systems, the more upsell can be achieved with their large installed bases of customers. The greatest challenge many of them face however is selling entirely new cloud applications to entirely new customers they’ve never sold to before. The potential of these entirely new markets however is going to be a valuation multiplier in 2013 and beyond.

2013 US Technology M&A Insights (PWC Free Report Download)

Price Waterhouse Coopers (PwC) report published The US Technology M&A insights: Analysis and Trends in US Technology M&A Activity 2013. This report highlights the detailed M&A activity within the technology sector and 2013 outlook of strategic acquisitions, private equity, trends, divestitures, deal environments, catalysts for Internet, IT Services, hardware and networking, software, and semiconductor sectors. PwC is seeing SaaS, mobile devices, analytics and Big Data as the drivers of current and future M&A growth and a fundamental shift in deal volumes to software and Internet deals based on these technologies. The report says the most promising areas of M&A activity in 2013 are mobile application development start-ups who have the intellectual property it would take years for enterprise software companies to create on their own.

Investors Outlook

SaaS, Cloud and Trends will continue to be M&A deals focus on enterprise software suppliers increasing offerings. As competition increases and traditional older software companies struggle with challenges of rapid adoption of customer growth in these services of SaaS and Cloud. Be on the lookout for 2013, a new generation of SaaS, Cloud and Technology trend applications that eventually will replace the on-premise competitors.