Above-trend growth

The Fed’s current round of tightening has been widely characterized as one of the most aggressive in its history. Yet, the US economy is on course to expand by almost 6% annualized rate in the third quarter – quite remarkable for this late stage of the tightening cycle and an acceleration on the second quarter’s 2.1% pace. Powell told audiences at Jackson Hole that a continuation of this “above-trend growth” could warrant some further policy tightening.

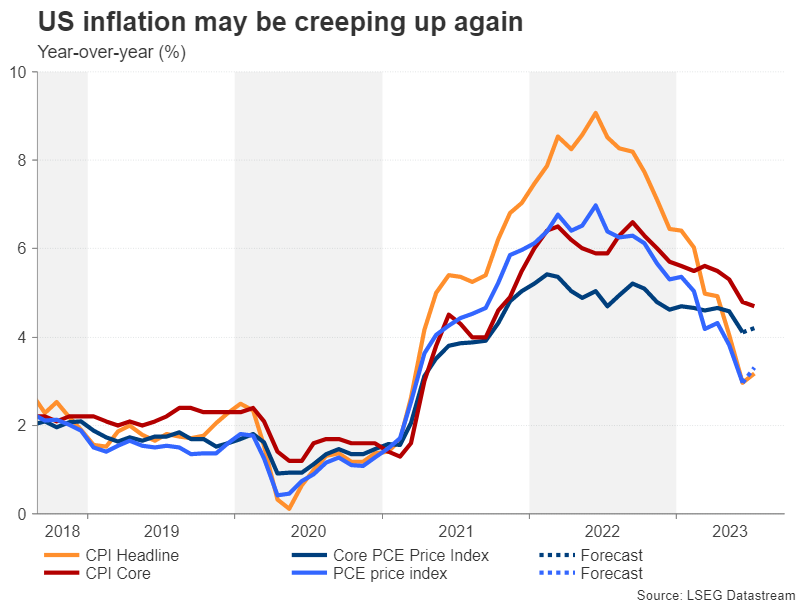

Will core PCE follow CPI higher?

On inflation, Powell repeated that it remains “too high” despite the recent declines. Non-housing services inflation in particular is a big concern, saying “some further progress here will be essential to restoring price stability”.

Overall services prices were 4.9% higher from a year ago in June according to the PCE measure. That’s notably higher than the core PCE price index reading of 4.1% y/y. For July, core PCE is forecast to have edged up to 4.2%. This would be in line with the rise in headline CPI during the same period, underlining the slow path to achieving 2% inflation.

Real wages are boosting consumption

With upward pressure on wages from a very tight labour market and consumer spending rebounding rather than slowing, it’s no wonder services inflation is elevated. Personal consumption is projected to have jumped by 0.7% over the month in July after increasing by 0.5% in June.

Personal income has also been growing steadily this year and it’s expected to have ticked up by 0.3% m/m in July.

Although higher borrowing costs have started to inflict some pain on many households, what’s likely boosting the consumer is the pickup in real wages in recent months as the rate of inflation falls below the rate of nominal wage growth. That trend looks set to continue for a while longer as wage increases are showing no sign of slowing amid a still hot jobs market.

Average hourly earnings are expected to have risen by 4.4% on a yearly basis in July, unchanged from the prior month.

Strikes could stoke wage-price spiral

However, that figure might only be headed higher in the coming months as there’s been a number of major strikes during the summer across America, many of which are ongoing, and firms have had to offer big pay deals to reach a settlement. American Airlines (NASDAQ:AAL) for example bumped pilots’ pay by as much as 46% over several years and UPS agreed a 17% pay hike for its drivers.

Headlines about double digit wage offers are bound to keep Fed policymakers awake at night. But for August at least, the latest strike actions, including the actors and writers strike in Hollywood, likely had a negative impact on employment.

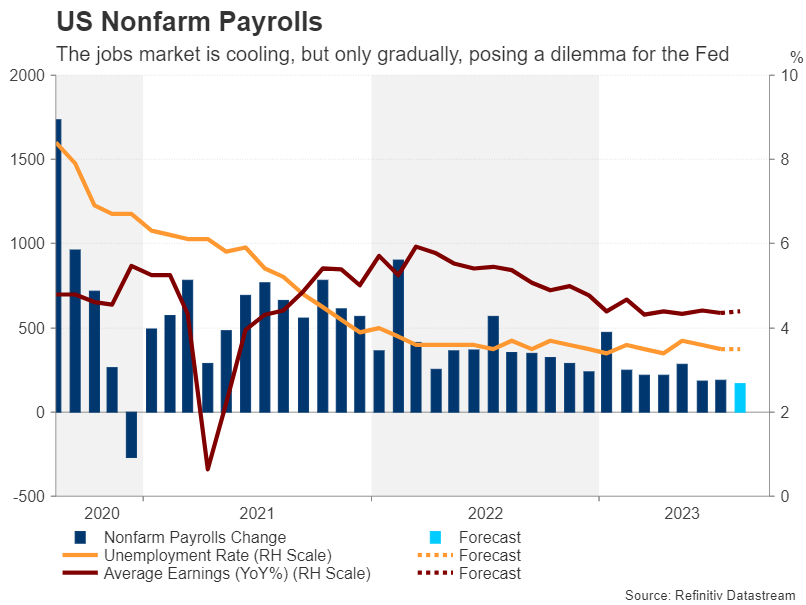

Payrolls increases are moderating

Nonfarm payrolls are forecast to have gained by 170k in August, down from 187k previously. The strikes pose a downside risk to the headline print so any positive surprises would probably shock markets and push up the odds for a 25-bps rate hike in September or November.

The unemployment rate is expected to remain steady at 3.5%.

Overall, the labour market does appear to be cooling and there was further confirmation of this after the Bureau of Labor Statistics reduced its estimate of the number of people on payrolls in March by 306,000 in its preliminary benchmark revision for 2023.

Excluding the wage pressures stemming from the labour disputes, the outlook for the jobs market has become somewhat gloomier, particularly in the manufacturing sector. The ISM manufacturing PMI due on Friday will be watched for more signs on what’s happening within the sector, specifically to output, employment and prices.

The deepening economic slowdowns in China and the euro area, which come against a backdrop of tighter credit conditions at home, are some of the other factors businesses have to consider before hiring new workers.

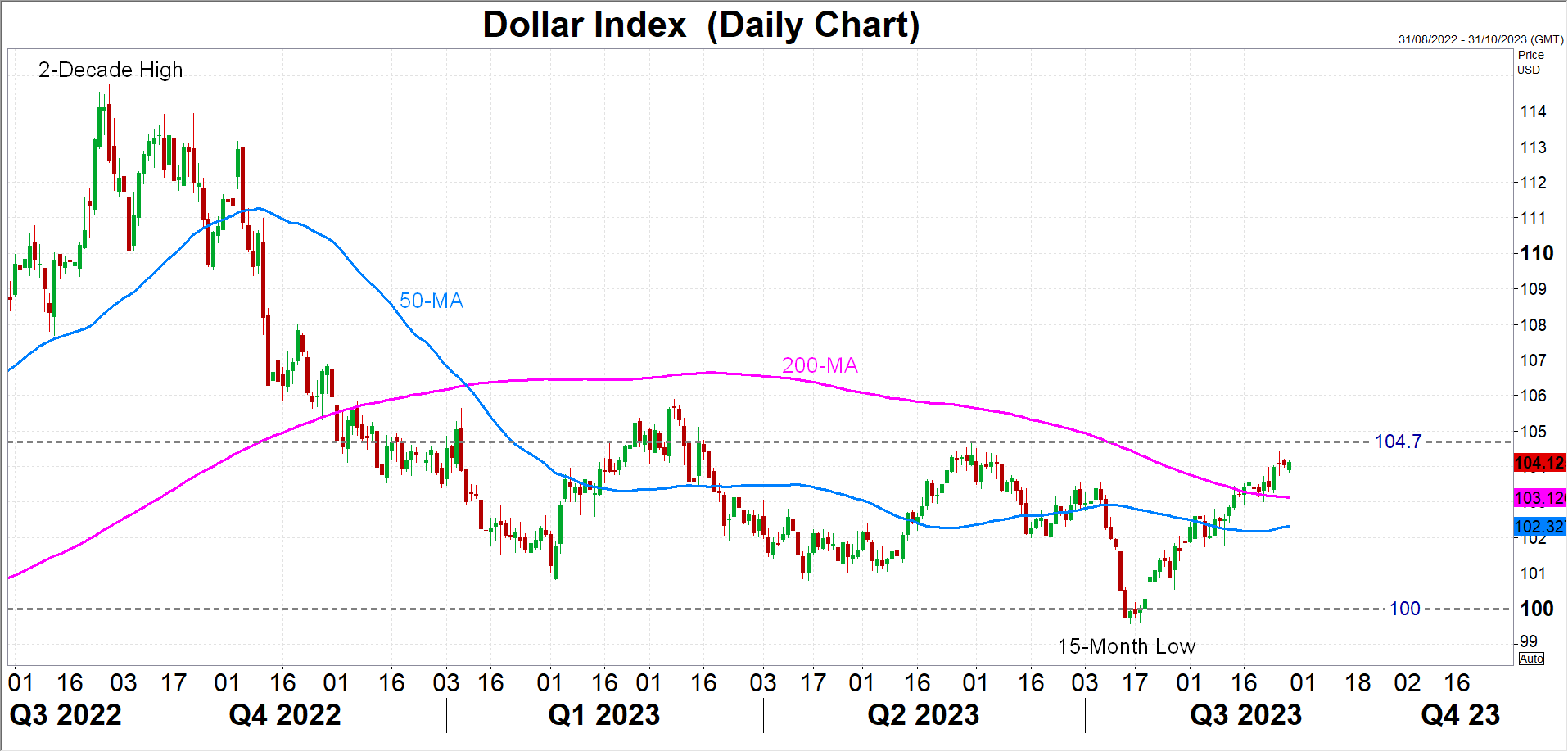

Dollar bulls hoping for September hike

For the US dollar, which is at a critical juncture against major pairs such as the yen, euro and pound, the data could determine whether its six-week-old rebound has more ground to cover. Whilst its gains have been impressive, the dollar index has yet to surpass its previous peak of 104.70 from May 31 and until it does, its medium-term outlook will stay neutral.

Powell has set the bar high for a September rate rise, making it clear that the Fed will “proceed carefully” when deciding on further tightening. Nevertheless, should both the core PCE and payrolls data beat expectations, it will be hard to justify a pause. However, if the week ends with a mixed batch of readings, policymakers are more likely to wait until November to get a clearer picture on what’s happening to prices and the economy.