To the disappointment of gold bulls, the yellow metal’s upward trend will not last long. Fundamentals have already taken their toll on gold miners.

While gold remains uplifted due to the Russia-Ukraine drama, the VanEck Junior Gold Miners ETF (NYSE:GDXJ) declined for the second-straight day on Feb. 22. Moreover, I warned on numerous occasions that the junior miners are more correlated with the general stock market than their precious metals peers. As a result, when the S&P 500slides, the GDXJ ETF often follows suit.

To that point, with shades of 2018 unfolding beneath the surface, the Russia-Ukraine headlines have covered up the implications of the current correction. However, the similarities should gain more traction in the coming weeks. For context, I wrote on Feb. 22:

When the Fed’s rate hike cycle roiled the NASDAQ 100 in 2017-2018, the GDXJ ETF suffered too. Thus, while the Russia-Ukraine drama has provided a distraction, the fundamentals that impacted both asset classes back then are present now.

Please see below:

To explain, the green line above tracks the GDXJ ETF in 2018, while the black line above tracks the Nasdaq 100. If you analyze the performance, you can see that the Fed’s rate hike cycle initially rattled the former and the latter rolled over soon after. However, the negativity persisted until Fed Chairman Jerome Powell performed a dovish pivot and both assets rallied. As a result, with the Fed chair unlikely to perform a dovish pivot this time around, the junior miners have some catching up to do.

Furthermore, while the S&P 500 also reacts to the geopolitical risks, the Fed’s looming rate hike cycle is a much bigger story. With the U.S. equity benchmark also following its price path from 2018, a drawdown to new 2022 lows should help sink the GDXJ ETF.

Please see below:

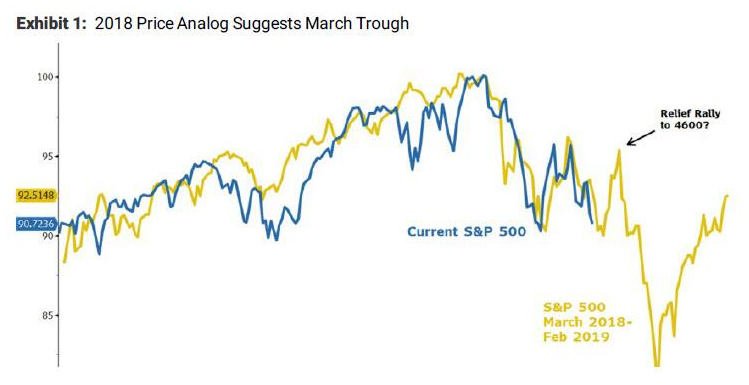

Source: Morgan Stanley (NYSE:MS)

To explain, the yellow line above tracks the S&P 500 from March 2018 until February 2019, while the blue line above tracks the index's current movement. If you analyze the performance, it's a near-splitting image.

Moreover, while Morgan Stanley Chief Equity Strategist Michael Wilson thinks a relief rally to ~4,600 is plausible, he told clients that "this correction looks incomplete." "Rarely have we witnessed such weak breadth and havoc under the surface when the S&P 500 is down less than 10%. In our experience, when such a divergence like this happens, it typically ends with the primary index catching down to the average stock," he added.

As a result, while a short-term bounce off of oversold conditions may materialize, the S&P 500's downtrend should resume with accelerated fervor. In the process, the GDXJ ETF should suffer materially as the medium-term drama unfolds.

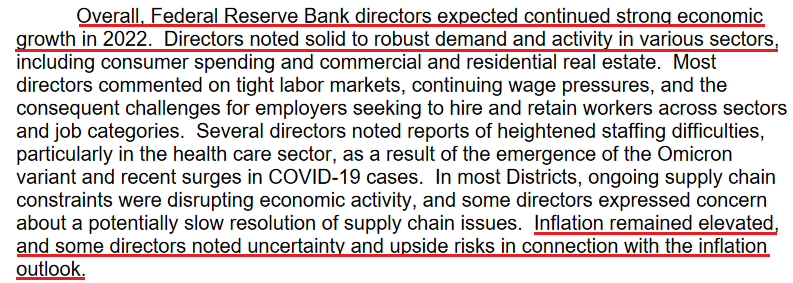

To that point, the Fed released the minutes from its discount rate meetings on Jan. 18 and Jan. 26. While the committee left interest rates unchanged, the report revealed:

“Given ongoing inflation pressures and strong labor market conditions, a number of directors noted that it might soon become appropriate to begin a process of removing policy accommodation. The directors of three Reserve Banks favored increasing the primary credit rate to 0.50%, in response to elevated inflation or to help manage economic and financial stability risks over the longer term.”

For context, the hawkish pleas came from the Cleveland, St. Louis, and Kansas City Feds. Moreover, the last time Fed officials couldn’t reach a unanimous decision was October 2019. As a result, the lack of agreement highlights the monetary policy uncertainty that should help upend financial assets in the coming months.

As evidence, the report also revealed:

Source: U.S. Fed

Thus, while I’ve highlighted on numerous occasions that a bullish U.S. economy is bearish for the precious metals, the Russia-Ukraine drama has been a short-term distraction. However, with Fed officials highlighting that growth and inflation meet their thresholds for tightening monetary policy, higher real interest rates and a stronger USD Index will have much more influence over the medium term.

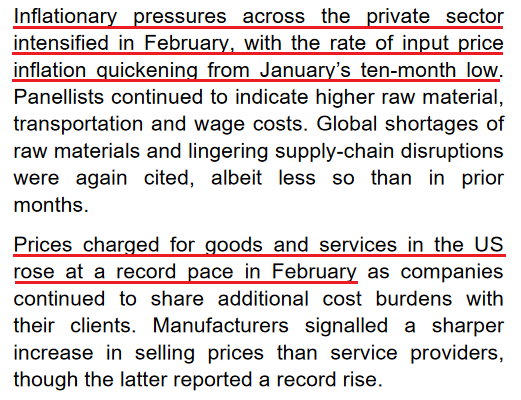

To that point, IHS Markit released its U.S. Composite PMI on Feb. 22. With the headline index increasing from 51.1 in January to 56.0 in February, an excerpt from the report read:

“February data highlighted a sharp and accelerated increase in new business among private sector companies that was the fastest in seven months. Firms mentioned that sales were boosted by the retreat of the pandemic, improved underlying demand, expanded client bases, aggressive marketing campaigns and new partnerships. Customers reportedly made additional purchases to avoid future price hikes. Quicker increases in sales (trades) were evident among both manufacturers and service providers.”

More importantly, though:

Source: IHS Markit

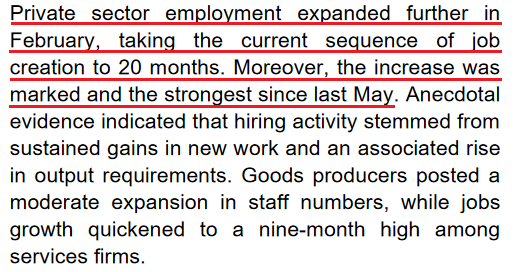

In addition, since the Fed’s dual mandate includes inflation and employment, the report revealed:

Source: IHS Markit

Likewise, Chris Williamson, Chief Business Economist at IHS Markit, added:

“With demand rebounding and firms seeing a relatively modest impact on order books from the Omicron wave, future output expectations improved to the highest for 15 months, and jobs growth accelerated to the highest since last May, adding to the upbeat picture.”

If that wasn't enough, the Richmond Fed released its Fifth District Survey of Manufacturing Activity on Feb. 22. While the headline index wasn't so optimistic, the report revealed that "the third component in the composite index, employment, increased to 20 from 4 in January" and that "firms continued to report increasing wages."

For context, the dashed light blue line below tracks the month-over-month (MoM) change, while the dark blue line below tracks the three-month moving average. If you analyze the former's material increase, it's another data point supporting the Fed's hawkish crusade.

Source: Richmond Fed

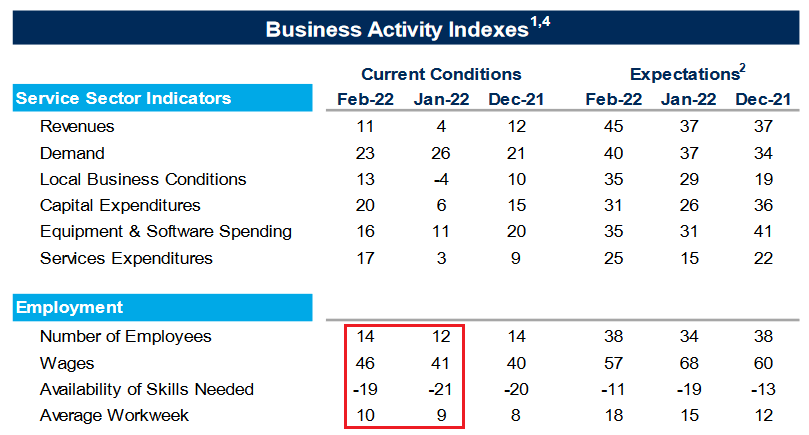

Finally, the Richmond Fed also released its Fifth District Survey of Service Sector Activity on Feb. 22. For context, the U.S. service sector suffers the brunt of COVID-19 waves. However, the recent decline in cases has increased consumers’ appetite for in-person activities. The report revealed:

“Fifth District service sector activity showed improvement in February, according to the most recent survey by the Federal Reserve Bank of Richmond. The revenues index increased from 4 in January to 11 in February. The demand index remained in expansionary territory at 23. Firms also reported increases in spending, as the index for capital expenditures, services expenditures, and equipment and software spending all increased.”

Furthermore, with the employment index increasing from 12 to 14, the wages index increasing from 41 to 46, and the average workweek index increasing from 9 to 10, the labor market strengthened in February. Likewise, the index that tracks businesses’ ability to find skilled workers increased from -21 to -19. As a result, inflation, employment and economic growth create the perfect cocktail for the Fed to materially tighten monetary policy in the coming months.

Source: Richmond Fed

The bottom line? While the Russia-Ukraine saga may dominate the headlines for some time, the bearish fundamentals that hurt gold and silver in 2021 remain intact: the U.S. economy is on solid footing, and demand is still fuelling inflation. Moreover, with information technology and communication services’ stocks – which account for roughly 39% of the S&P 500 – highly allergic to higher interest rates, the volatility should continue to weigh on the GDXJ ETF. As such, while gold may have extended its shelf life, mining stocks may not be so lucky.

In conclusion, precious metals were mixed on Feb. 22, as the news cycle continues to swing financial assets in either direction. However, while headlines may have a short-term impact, technicals and fundamentals often reign supreme over the medium term. As a result, lower lows should confront gold, silver, and mining stocks in the coming months.