This G20 meeting is a real test of where global markets stand as the currency war theme links directly to the developments in risk appetite as well. Action is likely to stay heated in coming trading days.

The ECB’s Weidmann got things off to an early start this morning, sending EURUSD 40 pips higher as the details of an interview were published early this morning in which the Bundesbank chief made a number of comments consistent with his hard-nosed rhetoric of late. See my squawk for a rundown of the highlights of this interview. The most interesting bit were in his speaking on behalf of Draghi and saying that the ECB president wasn’t trying to talk down the Euro. The other statement of note was the one speculating that the ECB may be forced to “show its hand” (employ?) the OMT, though the Bundesbank president said he hopes the ECB won’t have to buy bonds.

G20 to spark the next move…

At the same time, we have the JPY correcting stronger in the wake of the G20 draft communique from yesterday that makes a direct statement against competitive devaluations. The question to resolve in the coming days is the degree to which other statements from individual participants (particularly non-G7), whether in unidentified statements to reputable news agencies or in on-the-record communication with the press, reveal how far the worlds of reality and the official communique are apart. Good coverage from Reuters here on the currency war with very pithy quote from a SocGen analyst – “it’s not so much G6 versus Japan as it is G7 vs. G13".

Depending on the markets read of the G20 proceedings, we will likely see a significant pivot in the coming few sessions. If the market feels emboldened by a toothless G20 outcome (one which ticks all the rhetorical boxes in the major headlines and in the final communique but fails to offer any clue that anything will actually be done about the situation – i.e., talk is cheap and has nothing to do with the reality of likely Japanese policy), the pro-carry trade/risk appetite crowd could swoop in for one more big push lower in the JPY (USDJPY to 95.00 or even to 100.00) and push higher in risk appetite before we begin to see a consolidation in this big move. The other scenario is the sell-the-rumor, buy the fact one that merely see consolidation regardless of the outcome, simply on profit taking and almost regardless of the outcome. The other option is that we get some version of both, with wild swings both ways over the next couple of days, which perhaps has the highest risk as the market energy is as high as it’s been in a long time lately.

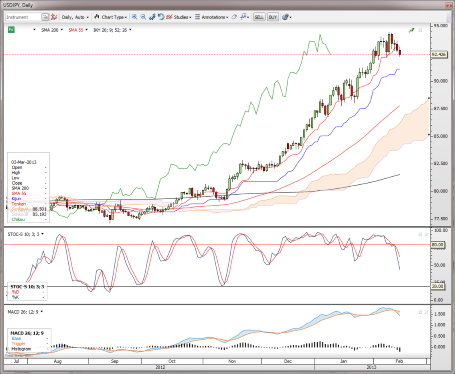

Chart: USD/JPY

It’s all about the JPY crosses surrounding this G20 event over the weekend and this market is far more about “mentals” than it is about technical – but a couple of points of note include the degree to which momentum has come off this week after the brief new high on Monday, and even the MACD is turning. Note that the Kijun line (blue) on the Ichimoku techs, has not been touched since last November – this could be an interesting first support if the pair corrects a bit lower through 92.15. To the upside, it’s perhaps more about whether the pair makes a stand – a strong up-tick back above 93.00 would argue for a new range forming at higher levels rather than a deeper correction in the near term. Per default, I’m usually a fan of event risks providing an opportunity for a near term correction – but it’s tricky when some of that correction has set in before the fact… Stay tuned… Perhaps most likely scenario is a big choppy fall of a few hundred pips in coming days, but with huge backup rallies all the way down as the big player (Soros and other big hedge funds are in on this move) add to their JPY shorts. USD/JPY" title="USD/JPY" width="455" height="374">

USD/JPY" title="USD/JPY" width="455" height="374">

And whatever you do, stay careful out there.

Economic Data Highlights

- New Zealand Q4 Retail Sales rose +2.1% QoQ vs. +1.4% expected and vs. -0.2% in Q3

- UK Jan. Retail Sales (0930)

- Euro Zone Dec. Trade Balance (1000)

- Canada Dec. Manufacturing Sales (1330)

- US Feb. Empire Manufacturing (1330)

- Canada Jan. Existing Home Sales (1400)

- US Jan. Industrial Production and Capacity Utilization (1415)

- US Fed’s Pianalto to Speak (1450)

- US Feb. preliminary University of Michigan Confidence (1455)