The G7 statement and surrounding confusion dominate the headlines for FX, with comical reading of the statement from a Japanese Vice Finance Minsiter Nakao, repeating the portions aimed at “domestic objectives” using “domestic instruments” a month after Japan purchased 10% , or EUR 400 million of eurozone ESM bonds in January. Nakao refused to comment on the unnamed official’s claim that the market was misinterpreting the G7 statement. It is clear from the various inspection of the G7 statement under the microscope that, while the G7 statement doesn’t look particularly critical on the surface, the rhetoric related to exchange rates has been stepped up, particularly the emphasis on the domestic instruments. From here, Japan will have far less room to manoeuver without triggering considerable hostility. And now we have the G20 tomorrow and Friday, an unwieldy organisation if ever there was one. It is clear that Russia has been the most vocal in flagging the risks of currency wars, with the Mexican central bank chief also chiming in recently. China has yet to sound off in any considerable way and remains the biggest question. As for G20 outcomes, it is hard to imagine any dramatic new agreement – rather, it will be interesting to see how bitterly some of the participants complain - and who otherwise will complain as the summit most likely releases a rather bland statement on exchange rates.

I would suspect that with tomorrow’s Bank of Japan meeting unlikely to produce anything of note and with a weak G20 statement, we are very likely to see a near-term consolidation in JPY crosses. Further extensive JPY weakening is only likely from here in the near term if both the G20 fails to issue any kind of statement or an extremely weak one with many participants walking away in clear dissatisfaction and world bond markets continue to sell-off while risk assets remain bid. That’s right – even from these levels there are two-way risks.

Fed’s Plosser and Lockhart discuss end of QE – market yawns

The cavalcade of unemployment rate projections continues from Fed officials, this time from the non-voting FOMC member Charles Plosser, president of the Federal Reserve Bank of Philadelphia, who said he expects the unemployment rate to decline toward 7.0% by year end, which will allow the Fed to reduce the rate of bond purchases. He also even said that a reduction in bond purchases should already be taking place. His (also non-voting) colleague Dennis P.Lockhart, the president of the Federal Reserve Bank of Atlanta, was also out speaking and said that the Fed wil probably continue buying bonds into the second half of the year – but has to be wary of the risks of asset bubbles.

A glance at the currency charts shows that this has been thoroughly ignored – but there is relatively consistent noise from a variety of Fed officials – not only in discussing the timing of a QE reduction, but also risks in asset markets. So from here, one has to imagine that if asset markets continue to rally apace without more marked improvement in the economic data, then the rhetorical headwinds could pick up even further.

Riksbank – no move

The RIksbank left the rate unchanged at 1.00% - surprising me and about half of observers. Let’s see what Ingves has to say at the press conference . There were two dissenters to the move – one looking for a 25 bp cut and another looking for a 50-bp cut. Swedish 2-year Swaps jumped 5-6 bps in the wake of the decision. With a strong krona on top of a strong Euro- SEK is getting extremely rich across the board. Stay tuned. I’m look at the recent lows in USD/SEK with interest for whether they hold and 8.50 is an important area for EURSEK.

Looking ahead

The BoE Inflation quarterly inflation report is up at 1030. The thinking that has driven the pound lower (though I think mostly it has been a popular punching bag versus the surging Euro as the GBP safe haven trade has unwound) is that the BoE is willing to tolerate a good deal of inflation in order to get the economy going again - something it has already done in recent years anyway, and that the BoE might revise down forecasts for growth. Even so, I suspect the pound selling has gotten way ahead of itself in the nearest term even if there is little recommend the currency and wouldn’t be surprised to see a very sharp rally in the near term versus the Euro and maybe even a little against the US dollar after yesterday’s attempt at a comeback.

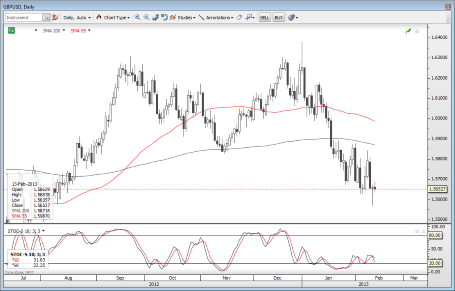

Chart: GBPUSD

An interesting bullish candlestick yesterday from GBP/USD – but it’s all about today’s quarterly inflation report from the BoE. The 1.5575 area lows were a clear Fibo extension target and the rally back above the previous lows puts in a bit of momentum divergence and softens the strength of the sell-off. Still, let’s see the other side of the BoE report and the new G20 statement on exchange rates if any. Any rally may not have much in the way of ambition beyond the 1.5900 area, though 1.600 is perhaps the “final” resistance for a consolidation of any size. EUR/GBP is likely to remain the more volatile way to trade a sterling view, which these days is implicitly a EUR view. GBP/USD" title="GBP/USD" width="455" height="291">

GBP/USD" title="GBP/USD" width="455" height="291">

Today’s main event is the US Retail Sales number, the first of the year that started with the bitter battle over the fiscal cliff, with the sequestration portion of that cliff still an open question, and the tax portion of it already decided (quick review of highlights: bump higher in income and capital gains tax for highest incomes, end of 2% payroll tax cut, and rise in estate taxes and the elimination of certain deductions for higher earners) While many workers won’t have received their first paychecks until the end of the month, it will still be a very interesting data point to watch for the degree to which the famed US consumer has been psychologically affected by the changes. The vicious dip in consumer confidence and the highest petrol prices for this time of year ever suggests some reason for caution, though we did see a strong ISM non-manufacturing data point in January – so I’ve got little if any confidence in calling this one. Expectations are running for a weak +0.1% growth in the ex Food and Gas number.

Economic Data Highlights

- Australia Feb. Westpac Consumer Confidence out at 108.3 vs. 100.6 in Jan.

- Japan Jan. Domestic CGPI out at +0.4% MoM and -0.2% YoY vs. +0.2%/-0.3% expected, respectively and vs. -0.7% YoY in Dec.

- Switzerland Jan. Producer and Import Prices fell -0.1% MoM and rose +0.8% YoY vs. 0.0%/+1.0% expected, respectively and vs. +1.0% YoY in Dec.

- Sweden’s Riksbank left rate unchanged at 1.00% as slim majority expected

- Norway Q4 GDP rose +0.4% QoQ as expected and mainland GDP rose +0.3% QoQ vs. +0.5% expected

- Euro Zone Dec. Industrial Production (1000)

- Sweden Riksbank’s Ingves Press Conference (1000)

- UK BoE Quarterly Inflation Report (1030)

- US Jan. Import Price Index (1330)

- US Jan. Advance Retail Sales (1330)

- US Dec. Business Inventories (1500)

- US Fed’s Bullard to Speak (1610)

- New Zealand Jan. Business PMI (2130)

- US Fed’s Dudley to Speak (2200)

- Japan Q4 GDP (2350)

- New Zealand Feb. ANZ Consumer Confidence (0000)

- Japan BoJ statement (no time given – last Asia hours)