The news you haven’t been waiting for… the sixth consecutive quarter of contraction in the euro zone! And that’s not likely to be the end of it; the market is forecasting that Q2 and Q3 will be negative as well. This morning we got provisional GDP figures from France and Germany, with the former officially in a recession following the second consecutive quarter of declining GDP, and the third negative quarter the past year. Germany narrowly avoided a recession as it showed ailing 0.1% growth missing the 0.3% estimate, yet showing an improvement from the 0.6% contraction in the previous quarter. Later in the day we get provisional, recessionary GDP data from Italy, Greece, Portugal, and the euro zone as a whole. The big question is how bad will they be? And for the markets, what is in the price? Euro zone GDP is expected to be down 0.1% qoq, which would be an improvement from the -0.6% qoq decline in Q4 of last year. Italy and Portugal are expected to have contracted mildly (-0.4% and -0.6% respectively), and Greece is heading for a fifth consecutive year of contraction.

On the day, the usual pattern is that a stronger-than-expected GDP figure means a stronger currency. But over the longer term, it doesn’t always work like that. In fact for much of the time, the dollar was actually weaker against the DEM and then the EUR when U.S. growth was above euro-zone growth, as the graph below shows. But there were also times when it wasn’t -- and can you hold a losing position long enough to tell which regime we’re in now?

Growth is important now as an indicator of where monetary policy is headed – countries with weaker growth are going to use monetary policy to boost it, as few countries have room to implement fiscal boosts right now (although Australia just yesterday renounced austerity in its budget for the next FY). In this case, weak euro-zone growth is likely to feed in to weak Eurozone inflation and push the ECB toward taking more steps to boost growth, with yesterday’s yoy downward revision of the German CPI for April adding to the worryingly low inflation figures coming out of the currency bloc. On the other hand, stronger-than-expected growth and at least maybe a negative deposit rate moves off the table and EUR/USD rises somewhat.

In the UK, the release of the Bank of England’s Inflation Report will overshadow the unemployment figures. Sterling fell 0.8% when the February report said risks to the recovery were weighted to the downside; similarly dovish comments again could knock the pound after its recent rises vs USD and EUR (although from the looks of things, people are still positioned for a weaker GBP; the Commitment of Traders report shows net short positions of 63.1k contracts, not far off the record short position of 76.8k). As for the employment data, the market is expecting no change in the ILO unemployment rate for March (7.9%) while the jobless claims is forecast to decline by 3k, vs a 7k decline in March.

There’s a busy day in the US, too. The Empire Manufacturing Survey for May is expected to rise slightly to 4.0 from 3.05. Industrial production for April is expected to have fallen 0.2% mom after a 0.4% mom rise in March, with capacity utilization falling to 78.3 from 78.5. Core producer prices are seen rising 0.1% mom in April, down from 0.2% mom in March, which would leave the yoy rate unchanged at 1.7% -- not low enough for the Fed to start worrying about deflation. After all this, will anyone be watching the NAHB housing market index? It’s expected to rise to 43 from 42. And there’s also the Treasury International Capital (TIC) data, which will be analysed to see just how the US is paying for its trade deficit.

Overnight there’s a slew of Japanese data, including GDP, which is expected to be +0.7% qoq in Q1, up from 0.0% (no change). But the real point of interest will probably be the GDP deflator, which is forecast to fall further into deflationary territory (-0.9% yoy vs -0.7%). In addition to these weighty quarterly figures, investors will be watching the weekly international portfolio statistics that come out at the same time to see if Japanese investors, who just recently became net purchasers of overseas assets, continued buying.

The Market

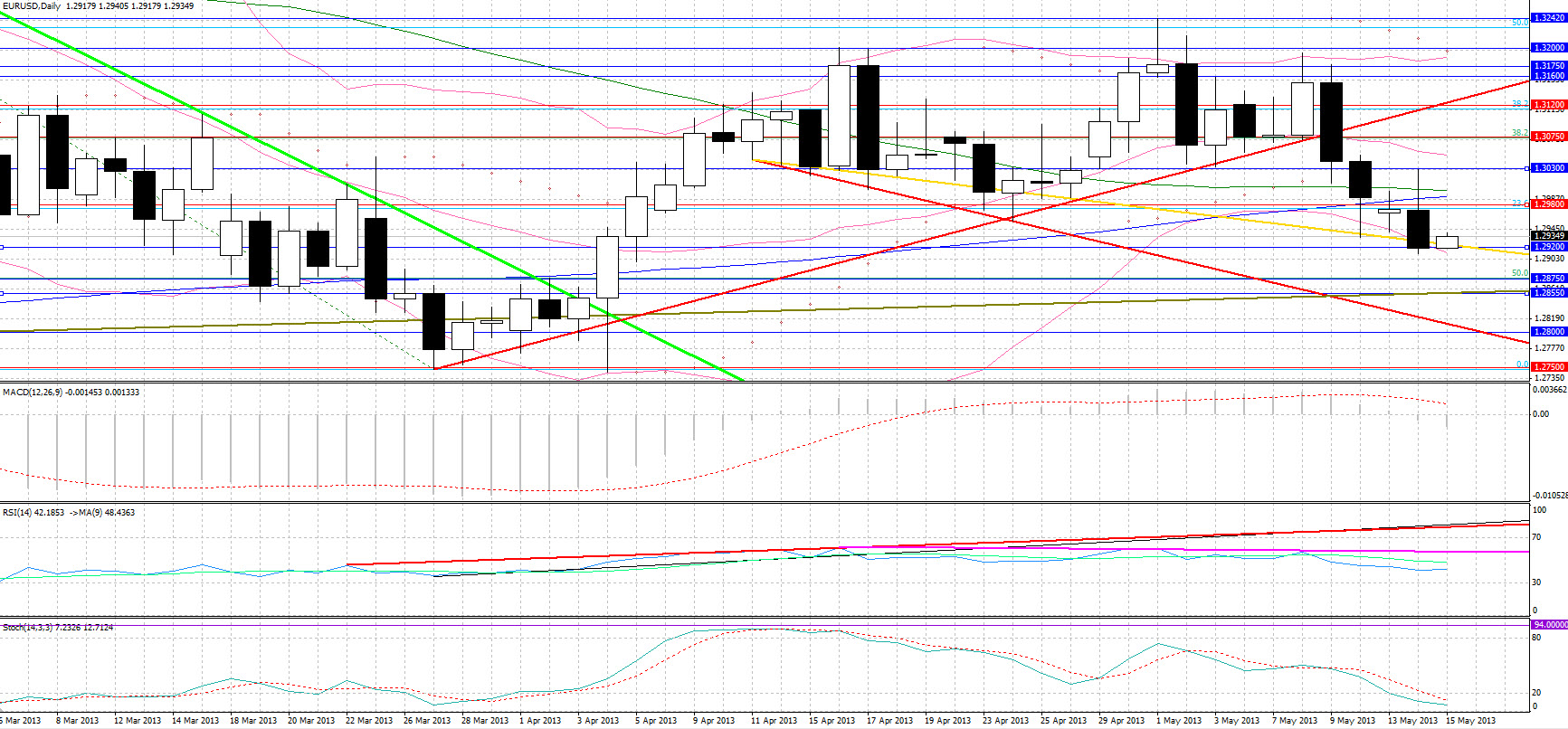

EUR/USD  EUR/USD" title="EUR/USD" width="648" height="474">

EUR/USD" title="EUR/USD" width="648" height="474">

• The US dollar gained from yesterday morning against all 24 currencies we track. Versus the euro, the greenback managed to reverse the breakout to 1.3030 resistance following the bullish crossovers on the 1-hour chart and the break above the 200- and the 50-day MA. The better-than-expected euro zone industrial production for March caused a retest of resistance but this was short-lived as the worse-than-estimated German and euro zone economic sentiment for May were given a greater weighting, triggering a decline to 1.2930 support, briefly spiking to 1.2920. With the euro-zone states set to publish weak, yet improved, GDP figures, and with today’s indicators from the U.S. likely painting a mixed picture the pair is likely to experience volatility today as it lies in oversold levels as seen in the daily, 4-hour, and 1-hour charts. Initial resistance looks to come again around 1.2980, which sees its 200-day MA and the 23.6% retracement level of the February – March decline, with further resistance levels coming at 1.3030 and 1.3075. Very strong support comes in the 1.2855 – 1.2875 area that concentrates the 50% retracement level of the July – February bull market as well as the neckline of a head-and-shoulders pattern that has been forming since September 2012.

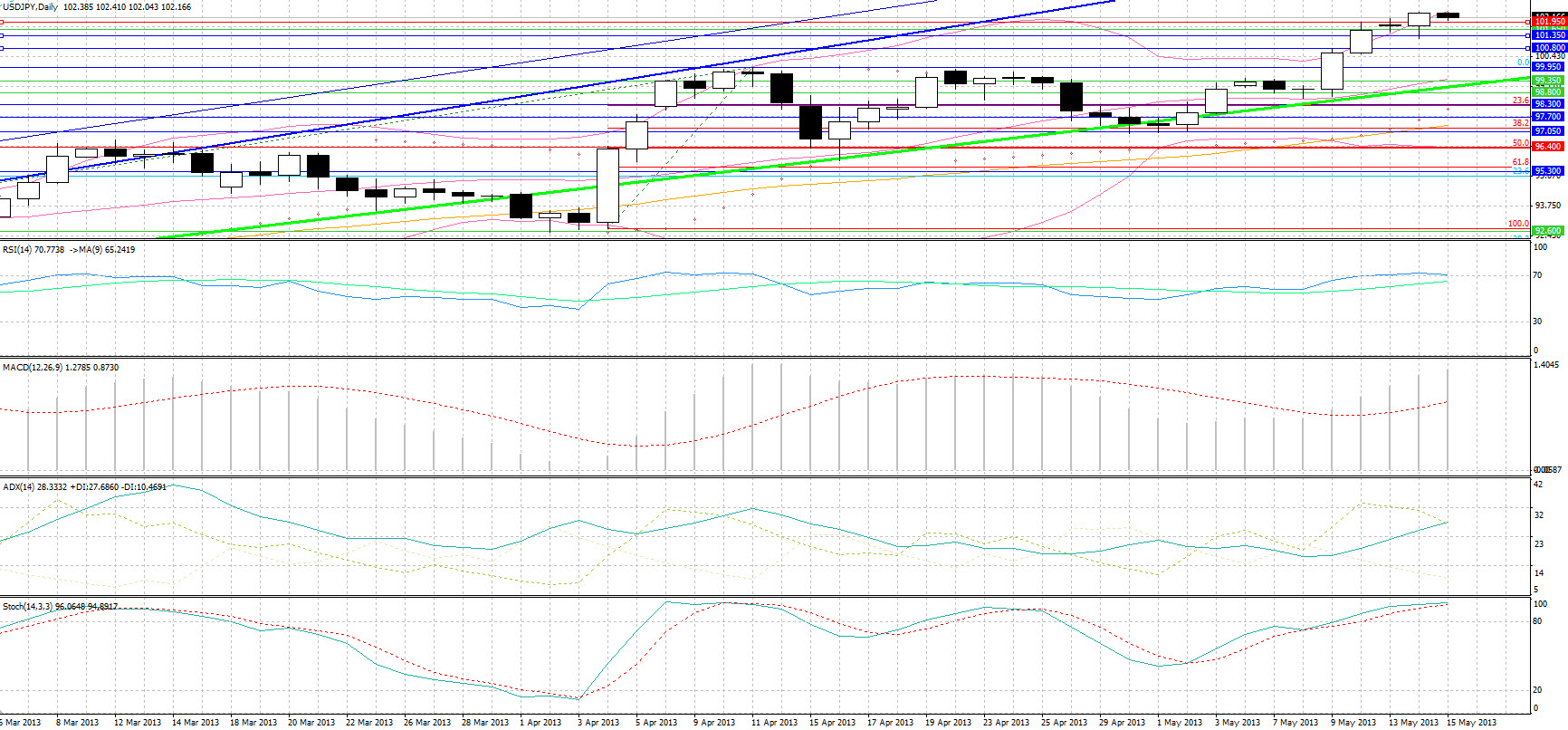

USD/JPY  USD/JPY" title="USD/JPY" width="520" height="474">

USD/JPY" title="USD/JPY" width="520" height="474">

• USD/JPY climbed to 102.4 on yesterday’s weak euro-zone figures, and the across-the-board dollar strengthening, as the unrelenting risk-on sentiment in the U.S. equities markets continued boosted all three major indices. Some profit-taking may be seen today as the overbought daily RSI and the Stochastics may signal a cap on the pair gains, similar to the two previous times this was the case. The flurry of Japanese data released overnight also adds to the risk, especially since the GDP deflator, an alternative to the CPI metric for inflation, may signal deteriorating deflation. Initial support may come at 101.95 with stronger support at 101.65 and weaker support at 101.35 and 100.80, with the next major resistance level coming at 103.90.

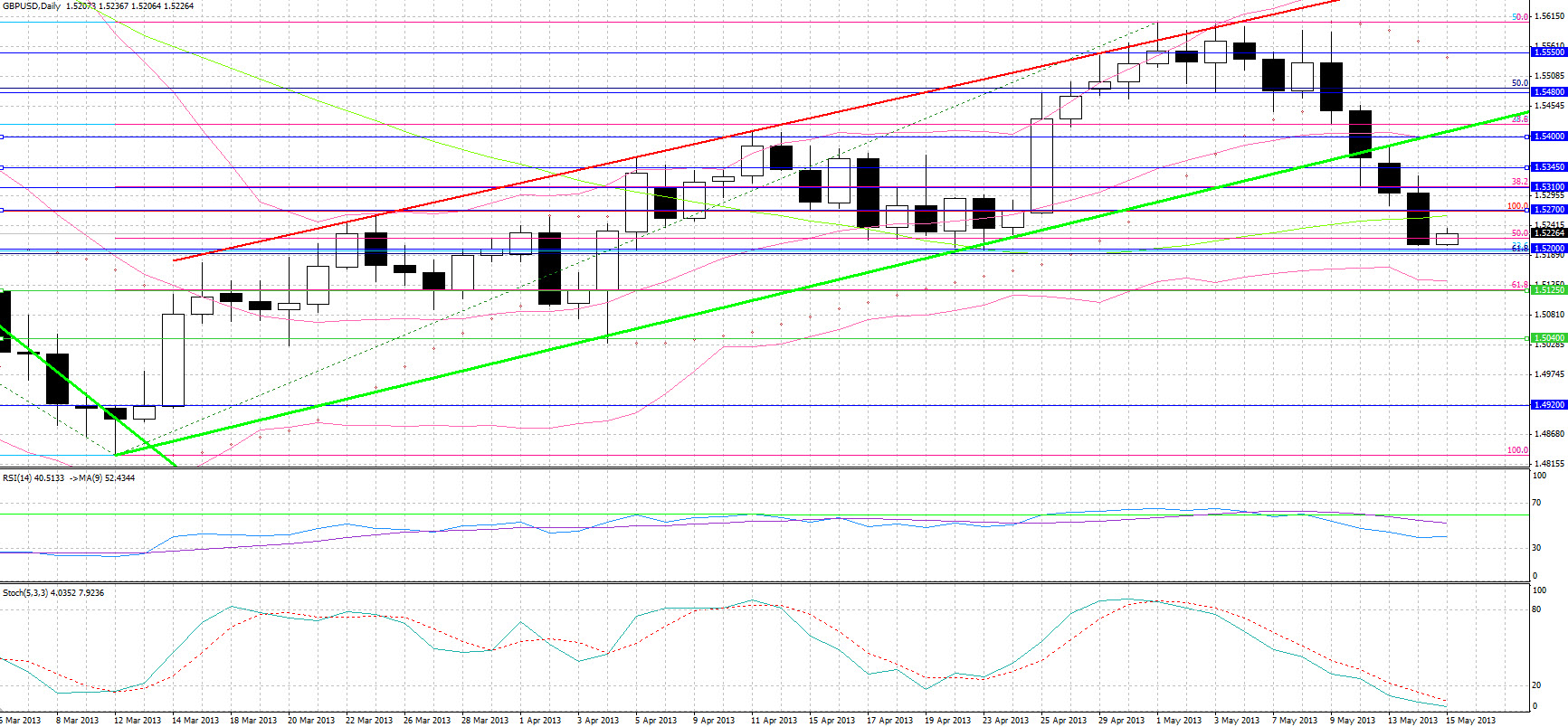

GBP/USD GBP/USD" title="GBP/USD" width="520" height="474">

GBP/USD" title="GBP/USD" width="520" height="474">

• Cable had a sustained downtrend yesterday, trading within a downward channel for the greatest part of the day. The plunge to the 1.5200 – 1.5220 strong support area that sees three Fibonacci levels placed a halt to the decline. Resistance may come in the 1.5260 – 1.5270 area that sees a reversal level as well as the 50-day MA. A breakdown from the strong support, which is likely given the significance of the BoE’s inflation report today, may drive price to 1.5125 support, the 61.8% retracement level of the March – May rebound, with a breakdown from that level driving price toward 1.5040.

Gold

• Gold weakened despite the poor euro-zone sentiment, hinting yet again characteristics of a risky asset. Support came at $1423, the 38.2% retracement level of the rebound, with the bounce that followed failing to reach $1445 resistance, adding to the successively lower peaks for the asset during rebounds, which tend to take place during the Asian sessions when physical demand supports the price. Later in the trading session, the dollar gains on the risk-on sentiment caused a further test of support, with the asset losing the past 24-hours more than the dollar index gained (-0.93% vs. 0.71% respectively). A breakdown may see support at $1400, with $1385 being the 23.6% retracement level of the post-plunge rebound. Further resistance may come at the well-tested $1476 level.

Oil

• WTI was driven to $94.50 support following the release of the euro-zone figures yesterday, which boosted the USD dollar. A break of support was triggered as the dollar furthered its gains, with the likely further increase in U.S. crude stockpiles announced later today adding to the downward pressures. $94.50 and $95.50 are likely to act as resistance levels with strong trendline, Fibonacci, and 50-day MA support coming at $93.40, with $92.35 seeing the 200-day MA.

BENCHMARK CURRENCY RATES - DAILY GAINERS AND LOSERS

MARKETS SUMMARY

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

It's GDP Day

Published 05/15/2013, 07:51 AM

Updated 07/09/2023, 06:31 AM

It's GDP Day

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.