GW is advancing a broad pipeline of early-stage cannabinoid therapies targeting cancer, metabolic and central nervous system (CNS) diseases. These five programmes (three funded by Otsuka) are based on strong preclinical data and/or promising clinical results. In 2013, we expect substantial pipeline progress with Phase II trial starts, Phase II readouts, initial human trials and potential Otsuka licensing deals. All this offers pure upside to our DCF valuation of £195m or £1.46p/share.

Deep Dive Uncovers Hidden Treasures

Our detailed review of GW’s early-stage pipeline reveals five programs with robust preclinical data and/or promising clinical results. In 2012, GW announced promising Phase II data for GWP42004 in Type II diabetes, demonstrating that the early-stage portfolio is starting to deliver. In 2013, we expect substantial pipeline progress as GWP42004 enters a Phase IIb trial, GWP42003 delivers Phase IIa data, three drugs enter the clinic, and potentially, Otsuka in-licenses CNS and/or cancer candidates.

GWP42004: Encouraging Anti-Diabetic Activity

Phase IIa data for GWP42004 suggest encouraging anti-diabetic effects, good safety and tolerability in patients with Type II diabetes. In particular, GWP42004 delivered consistent improvements in measures of glucose control, insulin production and beta- cell protection. In our view, these results provide a clear rationale for advancing the drug into a Phase IIb dose-ranging trial in Type II diabetes.

Spotlight On Epilepsy And Cancer Programs

GW’s research into cancer and CNS, which is funded under the Otsuka collaboration, has generated three promising candidates – GWP42002/GWP42003 for primary brain cancer (glioma), GWP42006 for epilepsy and GWP42003 for schizophrenia. The preclinical data for glioma and epilepsy are particularly promising and in our view could be sufficient to catalyse an Otsuka partnership for both programmes.

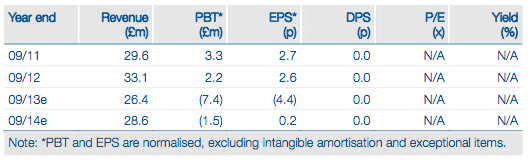

Valuation: R&D Pipeline Offers Pure Upside

We value GW at £195m, or £1.46 per share, based on a DCF analysis. Our base-case valuation comprises Sativex for MS spasticity (53p/share), Sativex in Phase III studies for cancer pain (79p/share) and projected FY13 cash (14p/share). On our valuation, the current share price of 55p appears to discount any new Sativex indications, the early-stage pipeline, or potential licensing deals. GW’s current market valuation, when combined with potential near-term value inflection points (German Sativex pricing/launch, Italian launch) in H113, represents a clear buying opportunity.

To Read the Entire Report Please Click on the pdf File Below.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

GW Pharmaceuticals: Early-Stage Pipeline

Published 03/13/2013, 01:43 PM

Updated 07/09/2023, 06:31 AM

GW Pharmaceuticals: Early-Stage Pipeline

Stirring The R&D Pot

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.