• German confidence a key matrix amid lowflation threat

• US retail demand seen improving

• US house prices expected to creep lower

An update on sentiment in Europe’s biggest economy will set the tone for trading on Tuesday with the June release of the Ifo Business Climate data, which has been softening lately. We’ll also see the weekly release of chain store sales for the US – numbers that should shed light on the outlook for retail spending this summer. For the moment, the trend looks encouraging. Later, an update is scheduled on US house prices with the monthly report on the Case-Shiller House Price Index.

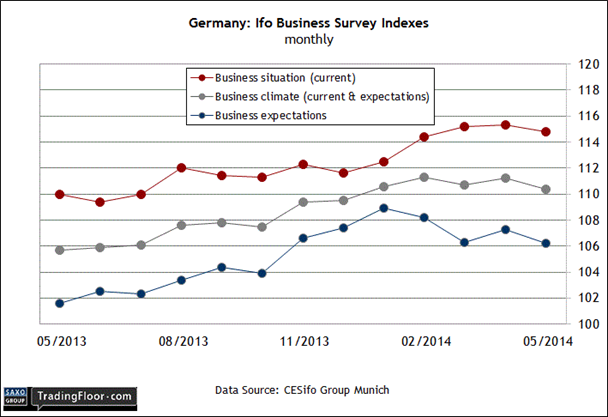

Germany: Ifo Business Climate Index (08:00 GMT):

Confidence in Europe’s largest economy is at its lowest level since late-2012, according to the June survey data from the Centre for European Economic Research/ZEW. “The German economy is currently in very good shape but further increases are becoming more difficult,” the group reported last week. “We had a strong first quarter in 2014 due to favourable weather conditions but signs are that the second quarter will be weaker.”

There’s still enough upbeat data overall to project that Germany’s macro trend will remain comfortably positive for the near term. The latest EY Eurozone forecast, for instance, sees GDP rising 2.0 percent in Germany, slowing to 1.5 percent next year. But the group added that “the threat of deflation is mounting” for the Eurozone. The European Central Bank may be prepared to nip the threat in the bud but the potential for trouble is still lurking. “Deflation, or even a period of very low inflation, would add to the problems of sluggish growth by raising real levels of debt and by delaying spending and investment decisions,” EY reminded us.

Deciding how big a problem “lowflation” poses to Germany and the rest of Europe is evolving, based on a range of factors. Sentiment is obviously a key metric since the crowd’s expectations could, under the right conditions, end up as a self-fulfilling prophecy, for better or worse. With that in mind, today’s Ifo release deserves close attention for insight on the mood in the business community. Recent updates show that sentiment has been slipping a bit, albeit marginally. The expectations component will be particularly valuable in the current climate.

For context, consider that the previously released ZEW data for June shows that the outlook among institutional investors continues to fall (the current situation numbers, by contrast, are still rising). Today’s Ifo release will provide another perspective on whether businesses generally are becoming increasingly gloomy about the near-term future.

Source: CESifo Group Munich

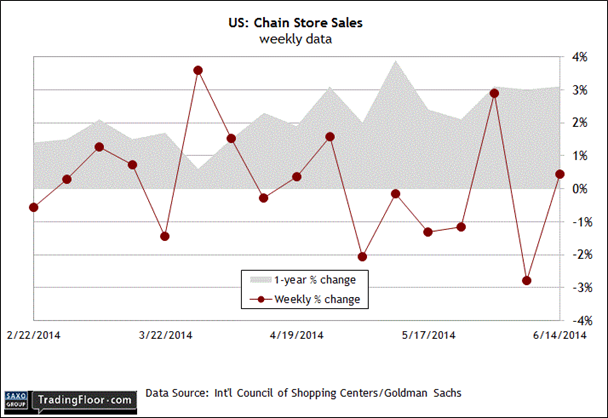

US:ICSC-Goldman Chain Store Sales (11:45 GMT):

Retail sales in April grew by a slower-than-expected 0.3 percent vs. the previous month, based on the monthly data from the government. The news weighed on the narrative that a spring rebound in consumer spending is unfolding. On the other hand, the weekly numbers from the International Council of Shopping Centers suggests that the revival, although delayed, is now well underway.

The smoking gun: year-over-year comparison for comparable store sales at major retailers has turned higher lately. Even better, the stronger run of spending on an annual basis has been consistent, running at an average of three percent across the last six weekly reports through June 14.

If today’s year-over-year rate delivers a comparable gain, the outlook will strengthen for anticipating progress in this summer’s monthly retail sales season. One hefty clue for optimism is the critical input for consumer spending – employment, which is looking moderately stronger lately. That bodes well for anticipating that retail demand on Main Street will remain firm, if not improved. Indeed, non-farm payrolls increased by more than 200,000 in each of the four months through May – the best four-month run of growth for employment in five years.

Source: Int'l Council of Shopping Centers / Goldman Sachs

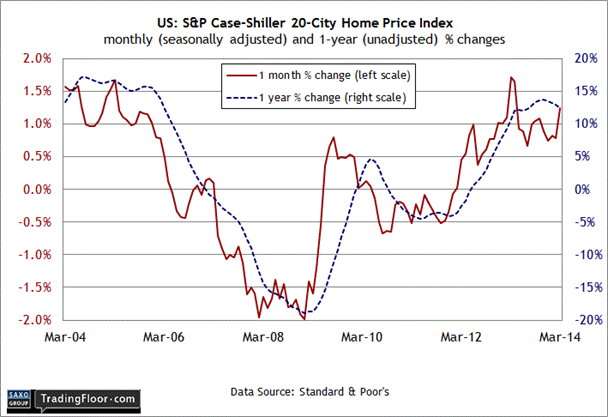

US: Case-Shiller House Price Index (13:00 GMT):

The robust increase in home prices in recent years has started to pinch demand, according to analysts. The bull market is said to be a factor in last week’s downgraded forecast for home sales for 2014. The Mortgage Bankers Association revised its 2014 prediction, projecting a 4.1 percent decline in existing home sales for the year overall. If the outlook holds, it will be the first calendar-year slide in four years.

“It’s no surprise that the spring buying season isn’t moving the needle this year,” said the vice president of research and analytics at Clear Capital, a real estate analytics firm. "The rising price floor in the low-tier sector of the market has squeezed investor returns, thereby removing a key demand segment. We don't expect to see a large pop in prices through the summer buying season.”

But if hefty price gains are part of the problem, some relief is coming. Economists think that today’s monthly update of the S&P/Case-Shiller House Price Index for April will show another retreat in the year-over-year growth rate. The consensus forecast anticipates home prices will advance 11.4 percent (in unadjusted terms), a relatively sizable deceleration from the previously reported 12.4 percent annual gain through March.

Based on raw year-over-year increases, price momentum peaked last November with a 13.7 percent rise and it’s been trending lower ever since. If today’s forecast is accurate, prices will be growing at its slowest pace in more than a year.

Looking ahead, Clear Capital expects the slowdown to continue. “May marks the fifth consecutive month national yearly home price growth has softened,” the consultancy advised in its June report. “By year’s end, home prices are expected to normalise in the sub-5 percent annual growth range.” That’s almost half as much as the current 9.2 percent year-over-year increase through May, based on Clear Capital’s numbers.