The price of gas at the pump is once again triggering many angry blame-throwers. I just heard Bill 'O Reilly of The O' Reilly Factor on my TV last night heatedly attacking the oil companies saying that our current $70 fill-up is the fault of a warm winter and some greed inspired exporting of our resultant oil surplus to China. Every time the oil price alarms us, you hear blame aimed at the evil oil companies, the evil speculators, El Nino, or whatever diverts our attention away from the real problem.

We are seeing a lot of buzz about blaming whoever is president for a shocking run-up in gas prices. But this blame game is mostly a myth as an article in the New York Times online by Nate Silver shows. It's silly to blame short-term moves in price on a president. Why not just blame El Nino? It's the long-term (multi-year) price behavior that should be blamed on our government's energy policy - and on that point I feel the past several presidents should be put on trial and shot for crimes against humanity.

'O Reilly's fit reminds me of the explanations of the out-of-control price of oil when it first went over $60 a barrel. It was speculators and, even though there was no real demand, Steve Forbes boldly explained that a new supply would be forthcoming because of basic supply and demand, and he issued his now infamous prediction of the return of stable $35 oil.

Well, oil went through a brief speculation enhanced gyration in 2008, but as it moved slowly back up through $80 in 2010, oil was the under-performing dog of a nice market and it was hardly the object of the hot money. And Forbes' supply fix for $35 is now laughable. As for 'O Reilly's blame on a weird winter, where was this explanation about this time last year, when Brent was even higher at $125 ? Iran's shenanigans were relatively quiet then too.

Why can't we understand we have a bigger problem than all this? About 2 years ago, CNBC began airing it's special "Beyond The Barrel - The Race To Fuel The Future". It prompted me to write an article about just this problem - the real reason we must spend $70 to fill up and why it's going to get much worse. If you believe, as our president does, that high oil will just accelerate a dive into non-fossil energy and that will save us, then read on. I called the article "Beyond The Barrel And Over the Cliff" and I repeat it here, because it bears repeating:

Tonight, CNBC premiers "Beyond the Barrel - the Race to Fuel the Future". This is a look at the alternatives to the crude oil bursting forth from the ground that has spoiled us for decades with cheap, abundant energy. One thing that will probably be missing in the discussion is the major issue EROEI. What is EROEI? How do you pronounce it? Well, I don't concern myself with pronouncing it, but I do get vexed by how much attention is being paid to it.

EROEI is simply Energy Returned On Energy Invested. It was not even a word back when Jed Clampett could start a bubblin' crude when he was out shootin' for some food. But as we started drilling deeper to recover oil, people like Cleveland and Hall began tabulating estimates on how much of our energy supply was being used to find, drill, and use our new energy finds. They come up with about a 100 figure for oil of the 1930s (1 barrel of oil burned to get 100 new barrels online). This had dropped to around 30 by the 1970s as so much of the easy to find oil in the world's elephant fields in naturally pressurized reservoirs has already been exploited. EROEI for oil and natural gas now is running around 8 - 11 depending on locale.

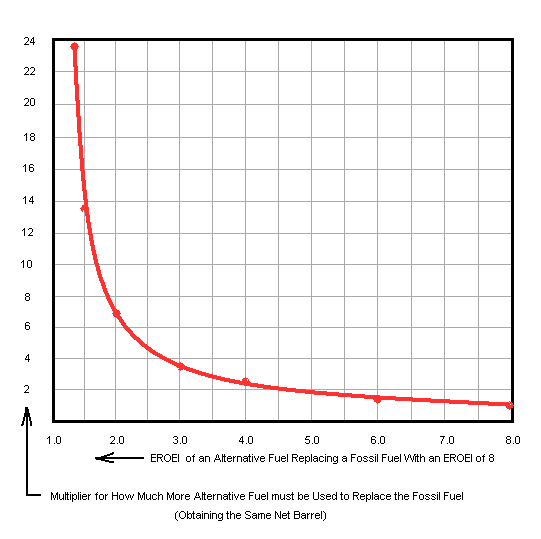

That is a huge drop from the 100 EROEI of the 1930s, but as it turns out in the math of net energy, it's not that big a deal. What is a big deal is what happens as this EROEI number goes from around 8 to below 4. (click on chart to view charts)

This chart, constructed by Dr. Euan Mearns, an editor at theoilddrum.com, plots net energy as a percent from 100 down to zero over EROEI's range from very high down to one, where it is taking a barrel of recovered energy to obtain a barrel of new energy (no net energy to use). As you can see, we're in fine shape as long as EROEI keeps north of 8, but we fall and we can't get up as we go over the cliff as EROEI goes to 4 and below. This is an exponentially increasing problem as we try to replace peaking crude production with things like corn ethanol, which is a worthless solution. Consider the following oil replacement scale showing the math of replacing the net usable energy content of an 8 EROEI fuel (like oil) with alternatives of less than 8:

Corn ethanol, at an estimated EROEI of 1.3, must be produced at a rate of over 20 barrels for each barrel of oil it replaces! Yet this is our Congressman's high dollar solution to peak-oil. Many biodiesel, solar, and electric EROEI estimates aren't much better.

You see a lot of barrel count estimates of future oil production as we deal with peak oil, but as we go over the top of the conventional oil production peak (the evidence suggests we already have) the flood of "alternative" liquids such as tar sand oil, deepwater, etc. are severely challenged to come close to matching crude's EROEI. This makes a big difference in how much net energy is actually being delivered to society despite the raw barrel count. This makes a good EROEI estimate of any new alternative fuel critically important - its most important feature. It should be the first thing discussed in all the news coverage and political speeches on alternative energy. But nobody is paying any attention as we approach the net energy cliff.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Gas Prices: Beyond The Barrel

Published 02/21/2012, 12:43 PM

Updated 07/09/2023, 06:32 AM

Gas Prices: Beyond The Barrel

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.