With tomorrow’s FOMC projections and announcements being such a big deal, it’s only natural that the markets priority at this stage is caution – dealers do not want to be taken out of, or even given positions that they have not initiated at such a late stage in the game. Today officially marks the first day of the Federal Reserve's two-day policy meeting, so investors are mostly in a wait-and-see mode ahead of the outcome.

Consensus this far expects the FOMC to announce its first reduction of asset purchases this week – a token taper of $10b – but Ben and the “boys” are expected to paint their decision as dovish as possible. To really do that, policy makers should only be tapering in Treasury’s rather than mortgage-backed securities, and by tweaking their rate guidance to include a lower inflation threshold. At this stage, the biggest wildcard is the FOMC’s forecast for Fed funds rate in 2016. Various fixed income dealers are calling for 2.75%-3%, putting it significantly above current rates. The market will also be looking for further clarity on asset purchase guidance, whose end has been tied to a +7% unemployment rate.USD/JPY" title="USD/JPY" src="https://d1-invdn-com.akamaized.net/content/pic289cc8b575e3759b9fb726e630d2ea0e.png" height="300" width="400">

In pricing, all of the above is now probably priced “in” by the majority and should not be seen as too big a surprise to the market. The shocker, if any, could come in the FOMC’s economic projections. The risks could be skewed to a more hawkish outlook.

There were little in the way of surprises from the UK’s inflation data for August this morning. It has come in as expected, +2.7%, down from the previous month’s print of +2.8%. The core measure of inflation was unchanged at +2%, y/y. Both Gilts and Sterling saw small changes on the reports. The “real” attention now turns to the release of tomorrow’s Bank of England MPC minutes for this months meeting. Any indication of a surprise then both Gilts and the currency will be on the move ahead of any Fed rhetoric. EUR/GBP" title="EUR/GBP" src="https://d1-invdn-com.akamaized.net/content/pic2e67b2b1b6ed974d015ada55181ec4dd.png" height="300" width="400">

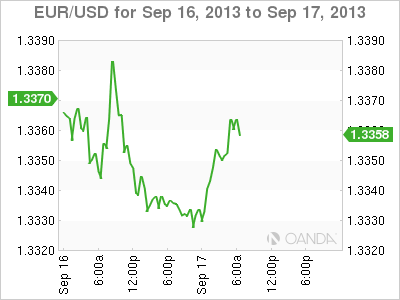

Investor sentiment on the German economy is at its highest level in three-years (49.6). This morning’s improved release should not be too big a surprise to the market – the DAX trading at a record could encourage market sentiment to push further on. However, one should also consider that despite more positive sentiment been seen on the PMI’s this also requires a follow-through from the “real” sector data. This is not the case as analysts note that July’s IP numbers show clearly that the German economy lags the improvement in market sentiment – the wish is greater than the reality! EUR/USD" border="0" height="300" width="400">

EUR/USD" border="0" height="300" width="400">

The stronger than forecast German ZEW should boosts any market inclination to buy the ‘single’ currency on dips. So far it seems that bullish technicals have been the main driver of a long EUR market this morning. It’s been reported that there are some heavy layered market offers touted between 1.3380 and the option protected 1.34 level. Speculators are unlikely to build momentum for a break either side before the FOMC meet. The market risk reward at current levels would suggest that selling the EUR’s on rallies is a preferred trade. However, given the lackluster nature of financial markets in the run up to any Fed announcement, the large vanilla EUR option expiries at 1.3350 will look even more attractive to the spot market later this morning.

The dollar has held on to most of the overnights gains against most of the G10 currencies ahead of US numbers and a number of buybacks later this morning. The market expects another benign inflation report with August US CPI rising +0.2%, the same as in July, while the core is expected to advance a modest +0.1%. With the majority of the impact of tapering having already been priced in – this summer's Emerging Market liquidation sale – a surprise $20b taper announcement tomorrow would likely trigger a bullish USD near-term reaction. If not, then the market should be expecting fairly limited price action from an announcement.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

FOMC: The Dollar's Risks And Rewards To Be Delivered Soon

Published 09/17/2013, 07:11 AM

Updated 07/09/2023, 06:31 AM

FOMC: The Dollar's Risks And Rewards To Be Delivered Soon

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.