The Federal Open Market Committee (FOMC) meets this week, and all eyes, ears, noses, and thumbs are at the ready to execute trades before, during, and after the event. A year has passed since the last tightening move by the Fed, but, way back then, our august bunch of banking buddies had also forecasted a wave of four separate rate hikes for 2016, each one to be 25 basis points. The catchphrase of “Interest rate normalization” was coined at the time, but 2016 did not turn out to be as “normal”, as it was once perceived. The global economy sputtered, and the Fed backed off on cue.

Fast forward to today, and you have a market that has priced in a rate hike without any doubts, nearly 100% by most estimates, a lead-pipe cinch, if you will. There has also been the very predictable run-up in the US Dollar Index, as traders factor in emotional sentiment to the hilt. Will the Dollar go higher after a rate hike? For such a highly anticipated outcome, you might very well witness one of the largest “sell-on-the-news” reactions in history. The momentum shift has more than likely been overblown, a reason why most forex brokers have been adjusting margin requirements before the chaos.

Where is the Almighty Dollar today? Here is a current chart portraying a broad measure:

This single chart depicts the torment that emerging market economies have had to endure since 2011, and, more importantly, from 2015 forward. The USD has been on a tear, once it became obvious that a divergence in central banking policy would become the predominant theme driving foreign exchange valuations for years to come. The rise in the greenback’s fortune began its a sharp asymptotic surge in early 2015, when the Fed began to ruminate its plan to cut back on quantitative easing and eventually begin the arduous task of adjusting its benchmark rates north of zero.

When the Fed backed off its ambitious plan of four rate hikes in 2016, the index fell like a rock, but it has gathered steam ever since. King Dollar is once again approaching the strongest its been during the new millennium, which coincidentally followed the infamous Internet bubble bursting episode of 2001, when irrational exuberance had taken control of investor mindsets. Are we positioning for a similar recessionary occurrence in 2017? It is a real possibility that seems to be gathering steam within the analyst community, judging from the number of articles and dire predictions that are flooding the airwaves at present.

What is the longer-term view on the prospects for the U.S. Dollar? Another chart is now in order, more to do with major currencies over the long term:

The general slide in the value of the Dollar versus other major currencies is readily apparent. It began in the seventies, when Nixon jettisoned the Gold Standard and a floating foreign exchange system began to take shape. Subsequently, the Fed literally expanded credit on a global basis, thereby enabling the growth of international trade and its ultimate consequences. From this longer perspective, the USD appears to have hit a diagonal ceiling of strong resistance at its present valuation. In other words, if the Dollar continues to strengthen, it may be putting sensitive international trade balances in jeopardy. Something will have to give, a concern shared by members of the FOMC and central bankers across the globe.

What changes are likely to come from this week’s FOMC meeting?

Everyone and anyone that has ever heard of the Fed is expecting a 25 basis point hike in its Federal Funds Rate target, following the completion of meetings on Tuesday and Wednesday of this week. The current target is 25 to 50 basis points, and the expected move would move the ceiling to 75 (current rates are actually a little above the 40 range). It is rare that the prevailing consensus is nearly 100%. In fact, it is difficult to find a single contrarian, who is willing to stake his or her reputation on the prediction that the “herd” has misread the tea leaves for this December.

The recent report out of the Department of Labor was right on target, 178,000 net new jobs were created last month, and the unemployment rate fell to “4.6 percent, in November, the lowest rate in monthly rate in nine years.” More importantly, the Fed has also been gradually reducing excess banking reserves in the system through its open market activities, a process that it also followed a year ago before the historic rate hike in December 2015.

For all intents and purposes, it would truly appear that the Fed has the “green light” to proceed. Per one analyst, “As far as the market goes, I would argue that the market has already priced in most of this increase in market interest rates. Furthermore, I believe that the foreign exchange market has also priced in this increase in determining the current level of the U.S. dollar.”

What could deter Fed action now? A strengthening USD is one possibility, but it has followed the rise in stock prices in lockstep. Otherwise, international tensions or the unknown could upset this apple cart: “Of course, something else could happen in Italy, in Venezuela, in Syria, in Greece, in India, or somewhere else in the world, or, in the United States, that would change the picture. But, then we have the question…what is the Federal Reserve going to do about interest rates in 2017?” No one has yet been willing to go out on a limb to suggest an answer to this poignant query.

Sir John Templeton would have viewed “Trump-phoria” with trepidation.

The recent market rally in stock prices has renewed a feeling of optimism among investors, bordering more on euphoria, if you check sentiment gauges and basic fundamentals. Before you run out and get fully invested, you may want to check insights of wisdom from the likes of Sir John Templeton, an American-born British stock investor, who became a billionaire by being a pioneer in globally diversified mutual funds.

Known as a savvy businessman and one of the leading philanthropists of his day, Sir John was never shy to share his prudent thoughts on market behavior. He actually shunned technical analysis, preferring to trust the fundamentals and his own intuition when it came to assessing trends in the financial marketplace. One of his observations most often cited is: “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” We doubt if Sir John would be “all in” at this stage.

Templeton would not be alone. There is a growing throng of doubters that see 2017 as a pivotal year, where equities may finally lose ground. The nature of the current euphoria became suspect after analysts began to take a closer look at its contributing factors. The rise in stocks was primarily a U.S. phenomenon. Global stock indices had actually remained flat or gone a bit negative. The S&P 500 reaction was predicated on a more business-friendly environment under a Trump administration, consisting of tax cuts, less regulatory red tape, and increased government spending on infrastructure projects and an expanded military presence.

Senate leaders are already claiming any tax amendments will be revenue neutral. Tax cuts to smaller domestic businesses may do nothing for the economy. Analysts believe the small changes will quickly be dissipated by competition. Multinational corporations have already figured out how to beat the tax code. Their effective tax rates are below other global competitors. In other words, the benefit of business tax cuts could be ephemeral. As for reducing regulations, this process will take time, and the benefits could take time to materialize, as well.

The Trump group will be hard pressed to deliver immediate job wins for their supporters. Any measure that smells like a stimulus package will only deal with the supply side of the ledger, but the continuing saga of the present economic doldrums is one that is lacking on the demand side. Repatriating corporate profits from foreign jurisdictions in hope of re-investment may be ephemeral, too. Previous attempts to tap into this $2.5 trillion treasure chest have only renewed efforts related to stock buyback programs, large bonuses and dividends, or M&A activity that resulted in job cuts, not the reverse.

That leaves the bulk of the work of carrying a populist tide to victory in infrastructure spending and a military build up that may ignite global tensions. Both measures will require deficit spending, unless matched with spending cuts. If the latter occurs, the economic benefit may again be, as with the other ideas, ephemeral. In other words, if it were easy to create new jobs in a hurry, it would have been done by now.

If you have followed the reasoning to this point, you might be seeing the handwriting on the wall for 2017. The headwinds are building, right in line with what has been termed “Presidential Election Year Principles”. In order to cut to the chase, the last dictum in this historical perspective states that an all-encompassing euphoria drives stock prices north, before the new president can even assume office. His first year in office is then plagued with making headway immediately, when reality resists him at every turn. The inevitable outcome is a depressed stock market and all that goes along with that collapse.

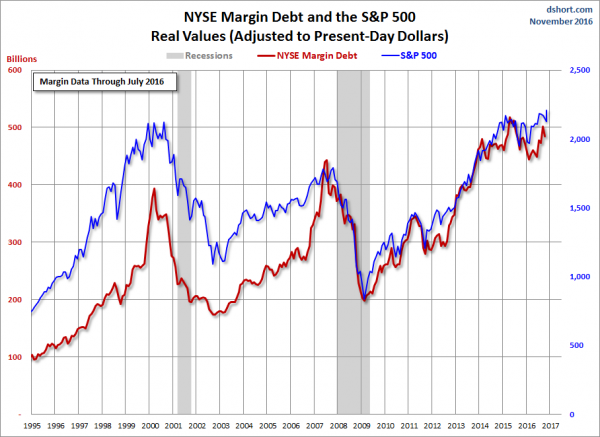

Is there another leading indicator, which foretells this outcome? As a matter of act, there is. Margin debt has a way of predicting possible pullbacks in stock valuations. Here is a representative chart that depicts this correlation:

Margin debt has peaked once more. Is a collapse in stock prices an inevitable outcome for the coming year? Many analysts are jumping on this train of thought, but we have seen many charts like this one that communicate a correlation, only to break down or become in a word, ephemeral. Correlation does not equate to causation!

Concluding Remarks

Will a Fed rate hike trigger a stock reversal? Many analysts feel that we are at a tipping point. Even a small nudge in rates could topple this house of cards. There is a band of optimists, however, that believes this bull has more to run, but not that long a run at that.

Something has got to give at some point. No matter how you measure it, this market is overheated. As we head for the FOMC’s long-awaited decision, one headline stands out: “A final burst of volatility may bookend a tumultuous year for the financial markets as the Fed delivers a much-anticipated policy announcement.” Stay tuned!

Risk Statement: Trading Foreign Exchange on margin carries a high level of risk and may not be suitable for all investors. The possibility exists that you could lose more than your initial deposit. The high degree of leverage can work against you as well as for you.