Fed holds rates steady but signals 2 more rate hikes this year

Yet investors were not convinced, dollar weakens, stocks jump

ECB decision in focus today, BoJ will follow early on Friday

Fed surprises, markets skeptical

As widely anticipated, the Federal Reserve hit pause on its tightening campaign yesterday, keeping interest rates unchanged. Nevertheless, the FOMC added a hawkish twist to the decision by signalling two additional rate increases for this year in its ‘dot plot’ of rate projections, helping to frame this as a temporary break in the hiking cycle instead of a complete stop.

Economic forecasts were upgraded as well, with the Fed now seeing stronger economic growth and a more resilient labor market this year, albeit at the cost of higher core inflation. Almost everything pointed towards a higher-for-longer path for rates, and in an attempt to cement this notion, Chairman Powell even said that any rate cuts are “a couple of years out”.

Yet, market participants did not ‘buy it’ and essentially reacted as if the Fed was bluffing. Market pricing implies only an 80% probability for another rate increase, which is a far cry from the extra two hikes the Fed pencilled in. The disbelief was reflected in most asset classes, with the dollar closing the session in the red and stock markets erasing some early losses to storm higher, despite the hawkish message.

One way of reading the market reaction is that investors are not as rosy as the Fed about the economy, and think a weaker data pulse in the second half of the year will prevent the Fed from executing its plans to raise rates further. So once again, it’s a game of chicken between the Fed and the market, shifting the emphasis on incoming data to decide who’s right.

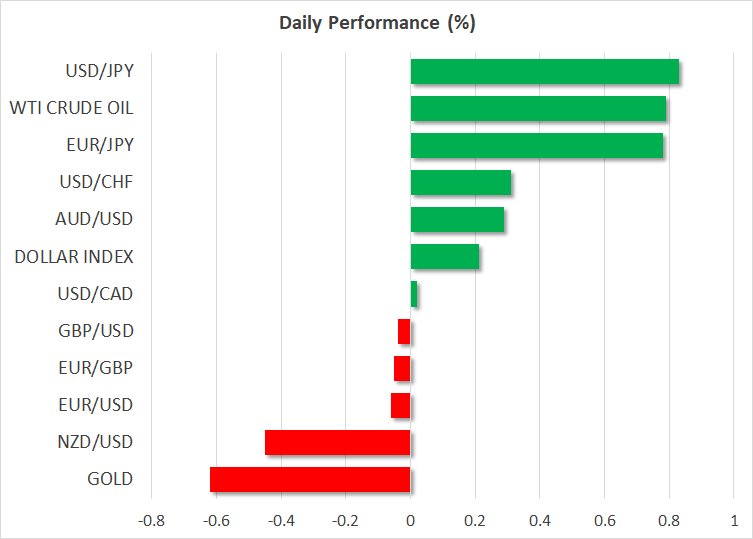

Dollar recovers as yen tanks, gold slips

The dollar index managed to recover some ground early on Thursday, with some help from rising Treasury yields and a sinking Japanese yen. It’s been a dreadful week for the Japanese currency, which has already lost 2% against the euro and sterling to hit new multi-year lows, crushed under the boot of central bank divergence.

It seems like traders are frontrunning the Bank of Japan decision tomorrow, where there isn’t much scope for policy changes. While inflation and wage growth have fired up, the BoJ is not yet convinced this strength will last. That could change in July if the Bank’s updated projections show inflation staying above 2% over the entire forecast horizon, but for now, policymakers will likely keep their powder dry.

Gold has fallen victim to the aftershocks of the Fed meeting. The precious metal is exhibiting some signs of relative weakness, as it was unable to capitalise on the retreat in the dollar and yields yesterday, rising very briefly before slipping to a three-month low today as those moves reversed. There might be some sovereign selling in play, for instance with China or Turkey unloading some gold to stabilise their currencies.

China cuts rates, ECB decision next

Following another round of worrisome economic data, Chinese authorities slashed the 1-year medium lending facility rate. The move was expected after the cut in the repo rate earlier this week, and hence not a surprise.

As for today, the spotlight will turn to the European Central Bank decision. A quarter-point rate increase has been widely telegraphed and is already fully priced in, which means the reaction in the euro will depend mostly on any messages about future moves.

With the Eurozone already in a technical recession and signs that inflation is moderating rapidly, it seems prudent for the ECB to dial down the hawkish rhetoric and not pre-commit to anything further. If the central bank shifts to a data-dependent approach and indirectly opens the door for a pause next month, that could disappoint the euro, as summer rate-hike bets are pared back.

It will be a busy session on the data front too, with the latest edition of US retail sales topping the economic calendar.