- Greece Ignores Self-imposed Deadline

- Sterling Plummets to Post Election Lows

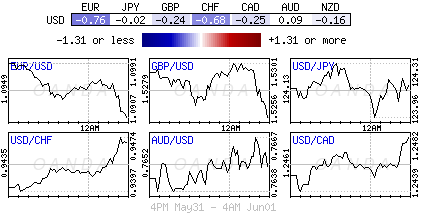

- EUR under pressure from all angles

- UK manufacturing to be a drag on growth

In Capital markets, this week will not be for the faint hearted. Market movement within the various asset classes will be dictated by a plethora of economic releases and a number of Central Bank rate announcements. Nonetheless, investors should be expecting both Greece, ahead of it’s +€300m IMF payment, along with the ‘granddaddy’ of U.S economic releases, non-farm payrolls, to be the highlights of this week’s trading both due this Friday.

With investors trying to get a better handle on the timing of the Fed’s first-rate hike. Ms. Yellen and her fellow cohorts have been rather vocal on how the timing of rate normalization is data dependent. Fixed income dealers will focus on September with much more interest if expectations for this week’s NFP report are realized. The market is looking for a moderate + 220k-headline print for a Q3 rate liftoff to remain intact.

Four central banks including the Reserve Banks of both India (RBI) and Australia (RBA), the European Central Bank (ECB) and the Bank of England (BoE) announce their respective monetary policy decisions. Traders’ calendars are also active with both manufacturing and composite PMI’s announcements for a number of countries including China, Japan, the Eurozone (and member states) and the U.K and U.S. Economists will also be assessing factory orders for Europe’s principal partner, Germany, and the world’s largest economy, the U.S, for signs of growth.

Euro’s Single Currency under pressure from all sorts

Capital markets will be held hostage to any dealing with Greece this week. The self-imposed Greek end of May deadline has passed without a deal with its creditors’ (IMF, ECB or EU). This will only heighten market tension as the first deadline schedule for June dawns near. Will the market witness any progress from Greece before Fridays first IMF payment is due? Only Greek politicians know the answer, as second-guessing their intended reactions is taxing enough.

Europe’s single currency (€1.0910) is heading stateside this morning under renewed pressure from the lack of progress in Greece’s bailout negotiations and some paring of Friday’s upside longs pressure. However, EUR dip buyers have been seen to limit a deeper decline (€1.0887-92). Good-sized market bids have been touted ahead of some of last week’s key support levels (€1.0850-60), at least for the first time around.

Already this morning, euro economic releases bring forth some mixed results. Manufacturing PMI data reinforces the regions fragile recovery, while German prices continue their improving trend.

Manufacturing activity in the eurozone grew more rapidly, but the results were mixed – Spain and Italy saw a strong pickup, while France was revised up a fraction, but Germany – the Eurozone’s backbone – was weaker and it’s slowest recorded pace in three-months. The Eurozone composite was revised down a fraction to 52.2 vs. market expectations of 52.3. The surveys indicated that the weaker EUR is certainly helping manufactures to win new export orders, while also raising costs for manufacturing by lifting import prices. The problem however is that euro businesses are not raising their own domestic prices which will only makes the ECB’s job even harder, especially as they are trying to lift the areas inflation targets back to their desired +2% level. Hence the importance of the ECB QE program.

The ECB is hoping that with QE, a weaker euro will eventually boost inflation by raising prices of imported goods enough that they will have to be passed on to the consumer – only time will tell how effective their QE program will be.

Sterling Plummets to Post-Election Lows

The pound has managed to move slightly lower again this morning to test a fresh three-week low below £1.5220 following a miss in this morning’s U.K PMI manufacturing (52 vs. 52.7). Previously, the pound touched a yearly high above £1.5800, a week after PM Cameron’s surprised Conservative majority win in the U.K general election last month. However since then, sterling has come under some intense pressure mostly on the back of some rather erratic economic data and the uncertainty over the U.K’s future relationship with the EU.

The market had been expecting the U.K to rebound strongly from a disappointing Q1, but this morning’s miss has dampened those hopes. Despite the headline print remaining in expansion territory (growth above 50), investors are disappointed by the modest expansion of output and new-orders during the month. A stronger pound and weaker business investment are not helping the situation. The market should be expecting a weaker U.K manufacturing to be a drag on quarterly growth. With GBP’s £1.5200 under threat, dealers will be eyeing the 100-day moving average as the technical first line of support (£1.5167).