With the UK markets back online after the holiday long weekend, playing catch-up is the order of the day. Euro credit markets are trading firmer this morning despite the non-rapturous applause in Asia that saw the Nikkei, Shanghai composite and Hang Seng close in the red after some quick profit taking on the back of a strong rally over the past few weeks.

When it comes to forex trading everyone should know the rules by now- currently its follow their own Central Banks lead. Last week's Jackson Hole economic symposium will eventually be regarded as a watershed moment for the Eurozone's survival. Despite Yellen's "neutral or less dovish" tone, it was "super" Mario Draghi's assertion that the ECB stands ready to act again that has quickened the pulse of Capital Markets. It was his comments that plans for ABS (Asset Backed Securities) buying are moving quickly - potentially shifting the mix of the ECB's austerity driven plan to quantitative easing. Draghi's sense of conviction has incited many to call for the introduction of QE at the ECB's next meet in September and the main reason for the ongoing current credit tightening this morning after the indices were more or less closed in line with the UK's timeout.

CBank banter guides currencies

Some smooth talking from Central Bankers seems to have now reversed the hefty US August correction in the markets, especially equities. Stock records continue to fall (S&P mythical 2,000 print, the Dow knocking on record highs), while 10-Year's rally to +2.37%. In Europe, the moves have been more pronounced. Draghi's QE rally cry will naturally favor equities and bonds and hopefully in the longer term manage to keep the EUR (€1.3199) on its knees in aiding regional growth prospects. It's natural that a "dovish" shift in tone by any CBanker probably justifies some market optimism; nevertheless, it's also important not to get too far ahead, especially in reference to the ECB's QE idea. Structurally, they are nowhere ready for it to be introduced and such plans are usually heavily data dependent. Before Europe can achieve its 'utopia' various positional squeezes will occur.

Positional play influenced by month-end

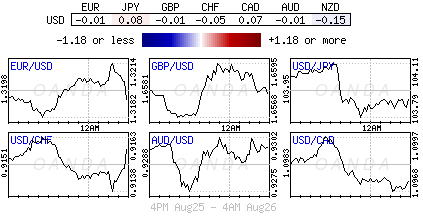

Draghi's dovish comments on inflation, weaker German Ifo data earlier this week and Euro-zone yields trading at record lows (10-year Bunds at +0.94%) will favor the EUR and maintain its allure as a 'funding' currency. Nevertheless, the markets 'weaker' EUR short positions will be squeezed and eventually forced to exit from time-to-time, as the 'single' units demise is not exactly linear. It's been reported that influential reserve names continue to want to fade any EUR/USD upticks (€1.3225-35). The recent month end dynamics (spot day this Friday) has seen US corporations being better USD buyers to close out the month. The 'mighty' buck seems to be consolidating some of its post JH Symposium gains ahead of this morning's US Durable Goods Orders. Even the techie's note that the dollar may have drifted into 'overbought' territory - a possible reason for lack of movement. Mind you, the appearance of a plethora of option barriers usually handcuff's a market until they come off.

The significant rate divergence rhetoric, couple with US/German 2-year spreads climbing (+2bp to a new +54.5bp high) has encouraged the growth of EUR short positions on the IMM. Intraday sellers continue to be camped on the topside with €1.3245 providing strong resistance while € 1.3150 barriers remain the focus for the next support. Some real-money buyers remain attracted to this area. However, EUR bears remain very much in control of the broader tone.

Follow the yield interest

It's not a surprise to see UK Gilts open sharply higher - they need to play catch up after yesterday's summer Bank holiday. The whiff of implementing QE by the ECB will favor UK debt products and the pound (both a yield grab). Despite data and events remaining thin on the ground, the market will be looking for any evidence to favor owning UK over Euro. Sterling's bounce from Monday's five-month low (£1.6542) is threatening to force a break above the psychological £1.66 handle. A momentum break through this level certainly opens the way for further gains to £1.6635-50. Nevertheless, without sustainable harder evidence, Monday's low will remain vulnerable.

Light buying from international and domestic interest continues to power the bid in the Euro peripheral debt markets. Supporting the QE story is the significant outperformance of Bono's (Spain) over BTP's (Italy) demand for debt products. The Bund-Italian spread has tightened -4bp to Bunds, which suggests that intraday dealers are bidding the market up as they grab the most liquid of instruments. Spanish bonds are doing even better: the 10-year benchmark to Bunds are -5bp tighter, probably reflecting investors’ greater comfort level for Spanish debt, and the fact that Italy does have midweek supply to contend with. Investors are doing the ECB QE pricing - now all it needs is the EUR to comply.