Equity markets posted new highs for the week and then reversed their gains earlier this morning as traders prepare for the debt-swap agreement in Greece and the added level of uncertainty led to some profit taking in stocks and high yielding currencies. Safe haven flows into the US Dollar were also seen as investors await the Gross Domestic Product data (GDP) out of the US but this number is expected to show some additional economic strength in the country for the fourth quarter and this price activity will likely reverse if the consensus expectations are correct.

The Euro and British Pound continue to make gains, trading above 1.31 and 1.56, respectively and the Japanese Yen (JPY) reversed some of this week’s losses and posted gains of 0.6 percent. Macro data out of Japan yesterday was positive, showing that Retail Sales beat the consensus expectations for the month of December. In the UK, FTSE 100 futures are pointed toward a higher open but we will only have the Nationwide Housing Price Index and an earnings report from John Swan and Sons for regional data.

Yesterday’s earnings from Nintendo (NTDOY.PK) were dismal causing the company’s stock to post massive declines. Losses were seen in both the quarterly and annual figures and this rounded out a day that was negative for most of the corporate earnings in Japan as similar results were also seen with NEC (NIPNF.PK), Elpida Memory (ELPDF.PK), Honda Motor (HMC) and Sony Corp (SNE). Part of the explanation for these weak earnings results is coming from last year’s strength in the Japanese Yen, which has weighed heavily on export orders and caused the country’s finance ministry to continually voice the possibility of central bank intervention in the currency markets.

Looking ahead today, the most important macro releases will be the US GDP, Core Personal Consumption Expenditures reading and the Michigan Consumer Sentiment survey. This will be rounded out by corporate earnings from Chevron (CVX), Procter & Gamble (PG), Ford Motors (F), and Honeywell Inc (HON).

Yesterday’s main movers in the S&P 500 were Starbucks (SBUX) (trading 2.1 percent lower, despite higher earnings numbers) after quarterly profit forecasts were revised lower. Juniper (JNPR) stock was 8.1 percent lower on weaker quarterly profits and similar results were also seen in Devry (DV) and Riverbed Technology (RVBD).

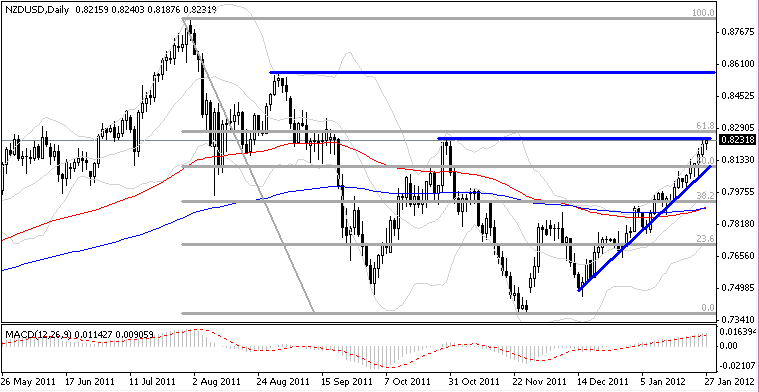

Today’s earnings will likely signal a short term top is in place for the S&P 500 if similar results are seen today. NZD/USD" title="NZD/USD" width="759" height="392">

NZD/USD" title="NZD/USD" width="759" height="392">

The NZD/USD is approaching some major, long term historical an Fibonacci resistance levels, with prices now pressuring 0.8250 with very little in the way of a meaningful pullback. Despite this lack of downside, we still have to view this as a sell entry region given the strength of the recent rise and the oversold nature of the rally. We look to start building short positions at current levels but enter lightly as prices could still see some extension to the topside.

The FTSE 100 is consolidating in the upper end of its recent range, with prices finding support at the 23.6% retracement of the latest rally. At this stage, the bias is still to the topside, as we continue to see higher highs and lows but momentum is starting to slow and we are expecting a medium term top to form in the next week or two. 5650 is the first support level to watch, and a break here will remove the bullish bias.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Earnings and Greek Event Risks Send Stocks Lower

Published 01/27/2012, 06:48 AM

Updated 07/09/2023, 06:31 AM

Earnings and Greek Event Risks Send Stocks Lower

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.