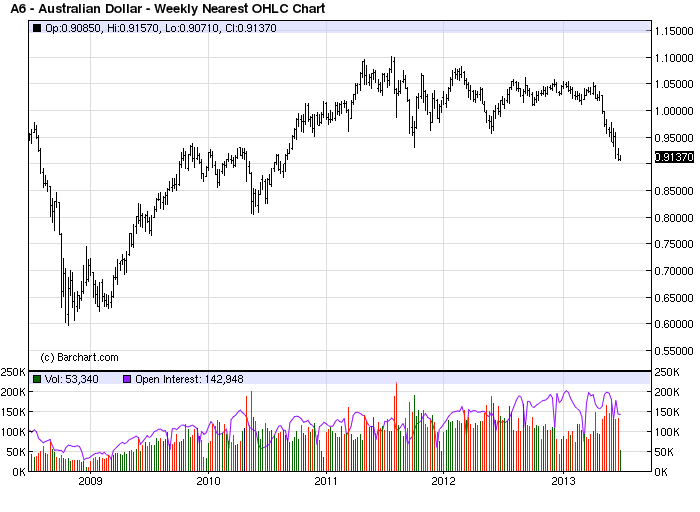

Last night/this morning we got (poor) PMI data out of China and (decent) Manufacturing data out of Europe. We also got new all time highs for European Unemployment (both headline and youth). The headline unemployment rate in the Eurozone = 12.1% and youth unemployment = 23.8%. Both new all time highs. The lowest unemployment rates are in Austria (4.7%) and Germany (5.3%) and the highest are Greece (26.8%) and Spain (26.9%). Tomorrow the Royal Bank of Australia is meeting and is expected to keep rates unchanged @ 2.75%, but it's possible they cut again. The Aussie has been cratering, making new three-year lows on Friday.

On Weds in the US we'll get the monthly (private) ADP jobs data as well as the weekly initial unemployment numbers (typically released on Thursday but pushed up because of holiday). Thursday the Bank of England will meet (now headed by Mark Carney -- who used to run the Bank of Canada). The Brits have high hopes for the Harvard hockey playing Goldman Alum. The ECB also meets on Thursday so there could be some Currency fireworks before the sun goes down on July 4.

On Friday (7/5) we'll get a look at June nonfarm payrolls. Expectations call for a top line number of +165k and 7.5% unemployment. The new (and improved?) results of the Bank stress tests are also due.

In the trading world -- The Yen is once again approaching Par with the Dollar. It's also back below the 50 day moving average again. Last time 6J (JYU13) broke par in early May all hell broke loose on currency crosses. Watching carefully.

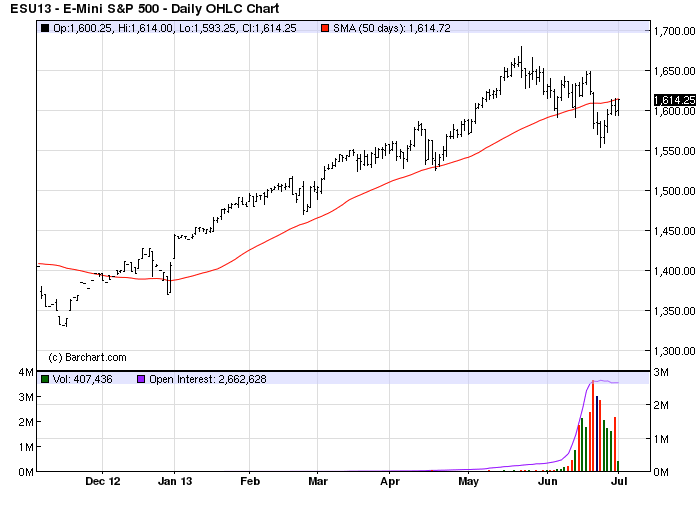

The S&Ps just broke back ABOVE the 50-day moving average.

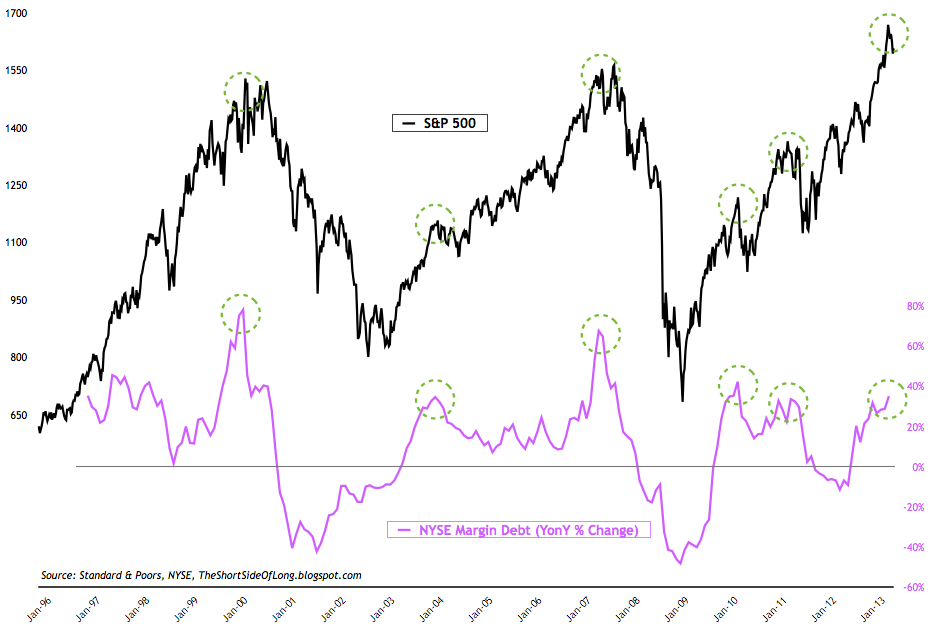

Margin debt (NYSE) was actually REDUCED last month (May) as volatility returned to the Equity market. On a year-over-year basis, margin use continues to climb.

Maybe I focus too much attention on collective short term memories, but I can't help but notice a few 2006/2007 echoes lately.

- I receive AT LEAST 4 credit card solicitations weekly.

- Channeling Stocks is running the same ad they did about 6-7 years ago showing some non descript 30 year old who is cleaning out his desk because he's retiring thanks to the services offered. He's been able to "buy low and sell high. The same stock, over and over". It's LAUGHABLE, but it must work. Maybe I'm the fool.

- Finally, and this is the one that really got me - I heard 3 radio ads selling information on successfully flipping houses over the weekend.

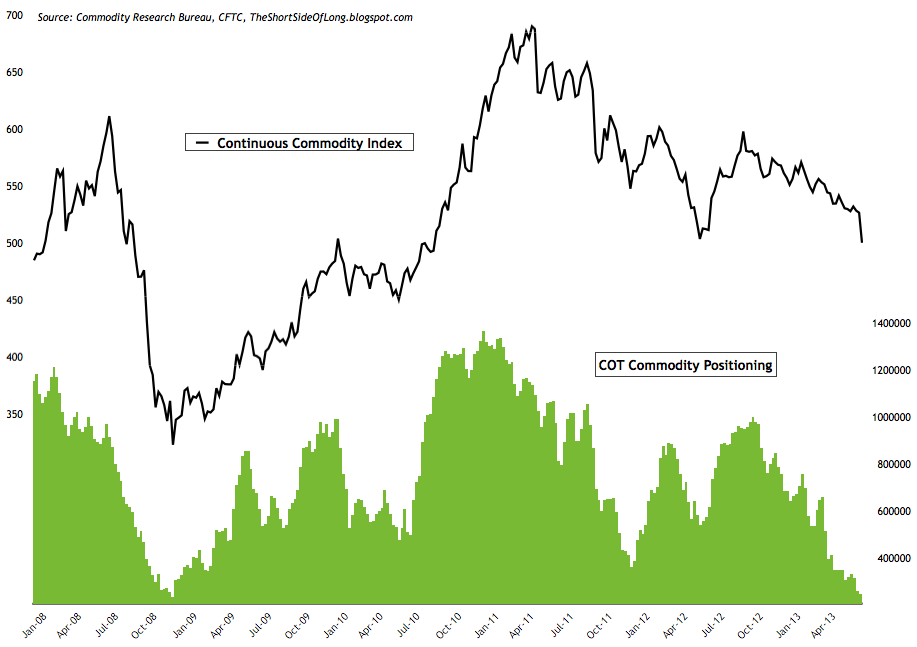

Moving on -- Hedge funds remain underexposed to Commodities in general.

This chart shows their exposure at levels similar to late 2008. Curious -- the deflation trade in full regalia.

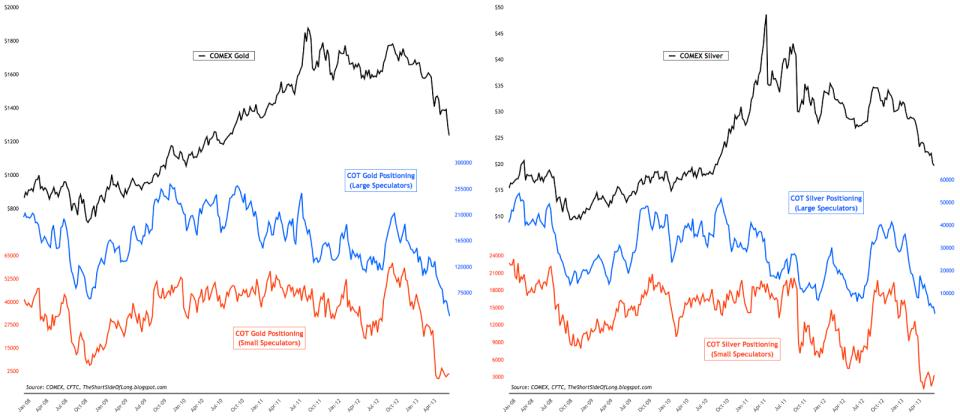

Speaking of deflation -- the Gold and Silver COT reports continue to plumb levels last seen.

Silver and Gold both made rather impressive reversals on Friday. It's too early to make a mountain out of a molehill, but the miners bounced, and now the metals are bouncing. Large and Short Specs have a bigger short position than they did at the bottom in 2008. That could be a tinder box if short covering begins in earnest.

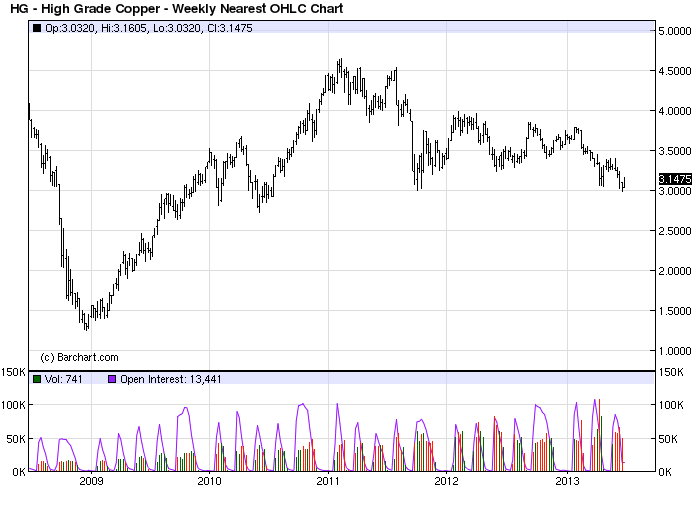

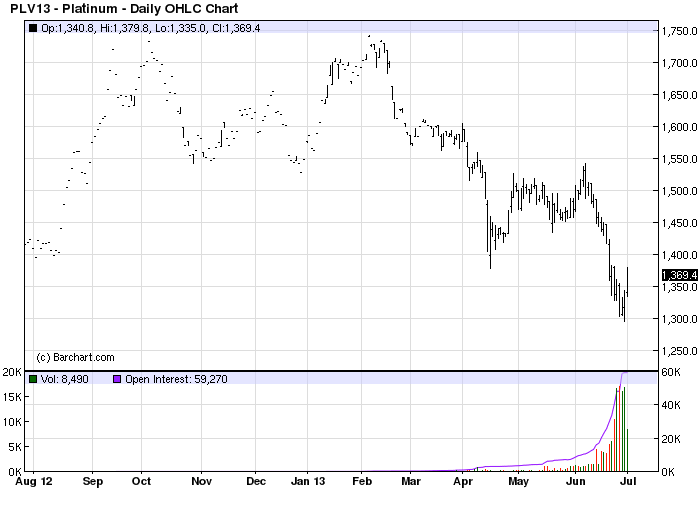

On the "Industrial" side -- Copper is nearly 20 cents off last week's lows. Up nearly 7% from lows. I mentioned Platinum trading/holding 1300 in late trade last week and this morning it printed nearly $1380. Up 6.5% from lows.

Here's a five-year look at Copper (in USD). $3.00 matters.

Here's Platinum (short term).

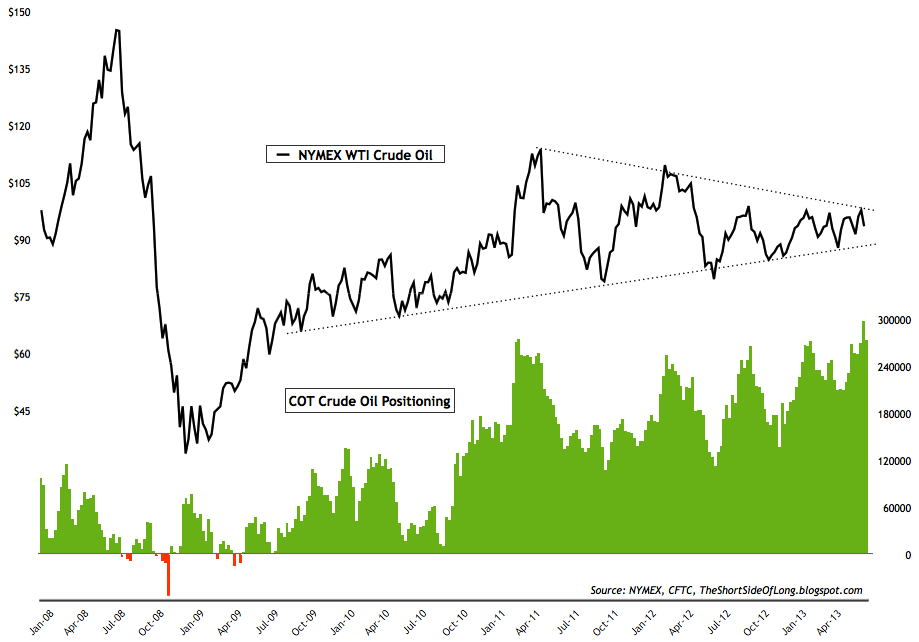

Finally, I found this COT chart on Crude oil to be interesting (and somewhat reminiscent of the Aussie Dollar prior to it's breakdown). The market has been fairly range bound for years and it's coiling into a tighter and tighter range. Implied vols are historically very low. (Frame of reference - 30 day vols in 2010 ~40%. 30 day vols in 2013 ~20%). In late March/early April of this year, implied vols in Crude were the lowest I've seen them in the past 7 years around 17%. That's simply too cheap. At the same point in time 30 day Gold vol was around 10% and Silver vol was around 21%. Those quickly moved to 40% and 55% respectively.

The Energy market is the one STUBBORLY inflationary commodity market. It's also the one that would benefit consumers the most from deflating. Watching carefully (and would recommend not being short much/any premium).

This is likely to be a slow week as trade desks are short staffed going into the fourtrh of July. That can exacerbate moves, so be aware. I will be OUT OF THE OFFICE on Friday.

Risk Disclaimer: This information is not to be construed as an offer to sell or a solicitation or an offer to buy the commodities and/ or financial products herein named. The factual information of this report has been obtained from sources believed to be reliable, but is not necessarily all-inclusive and is not guaranteed to be accurate. You should fully understand the risks associated with trading futures, options and retail off-exchange foreign currency transactions (“Forex”) before making any trades. Trading futures, options, and Forex involves substantial risk of loss and is not suitable for all investors. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources. You may lose all or more than your initial investment. Opinions, market data, and recommendations are subject to change without notice. Past performance is not necessarily indicative of future results. This report contains research as defined in applicable CFTC regulations. Both RCM Asset Management and the research analyst may have positions in the financial products discussed.