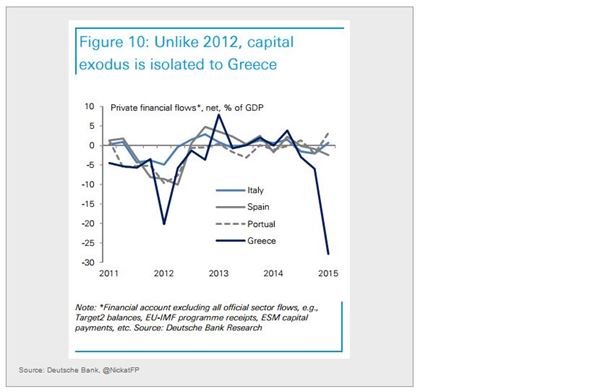

More evidence is emerging that Greece stands on its own when it comes to euro area exit risks. Unlike in the 2011/12 period, capital outflows are not an issue elsewhere in the Eurozone periphery. Whether now or in six months, the troika leadership is increasingly more comfortable to let Greece go should other options are exhausted.

Once again, it's important to point out that the most adamant supporter of forcing Greece to stick with austerity is not Germany. It is states such as Slovenia who are poor and had to tighten spending significantly. They do not want to see their taxpayers' money used for Greek debt forgiveness.

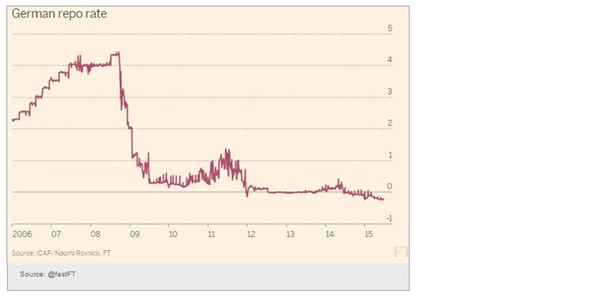

In other Eurozone developments, the area's money market funds are struggling with negative rates. Repo rates are not only negative but the liquidity in the market has declined. How do you attract depositors into a non-bank account with this?

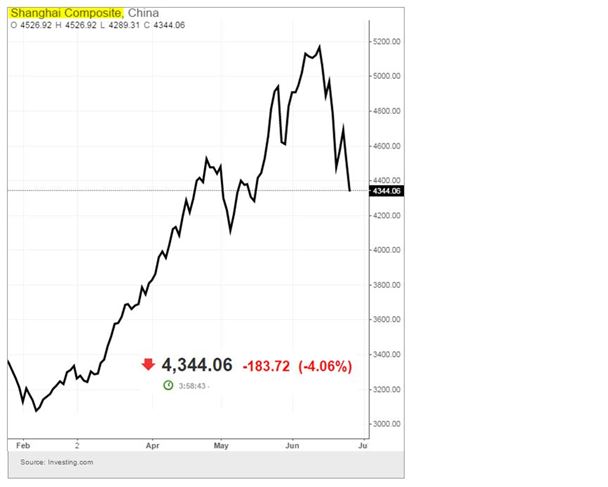

Switching to Asia, the Shanghai composite is now down 16% from the high as the volatility spikes.

Tokyo CPI comes out a month ahead of the national CPI and tends to be a good predictor of price increases across the country. The Bank of Japan's 2% inflation target remains elusive.

Japan's labour markets have tightened substantially, driven by increased hiring needs as well as labour shortages due to the aging population.

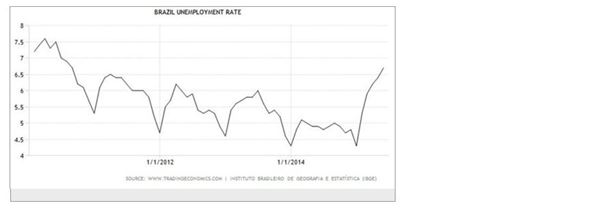

Brazil's unemployment reached a five-year high – this is no longer a seasonal increase. Political instability related to the Petrobras investigation sent shares and the currency lower and the CDS spreads wider on Thursday.

In the United States we continue to see a mixed economic picture:

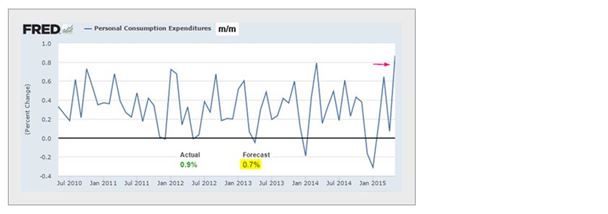

1. Consumer spending jumped more than expected.

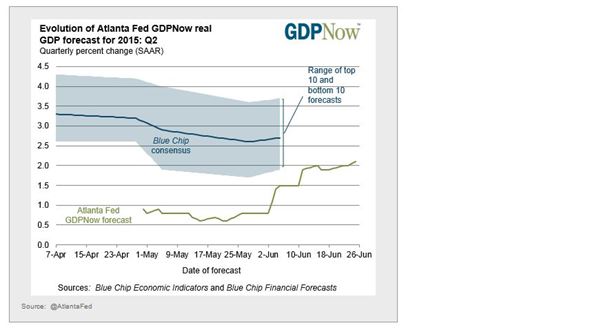

2. The Atlanta Fed US GDP tracker for Q2 reached 2.1%.

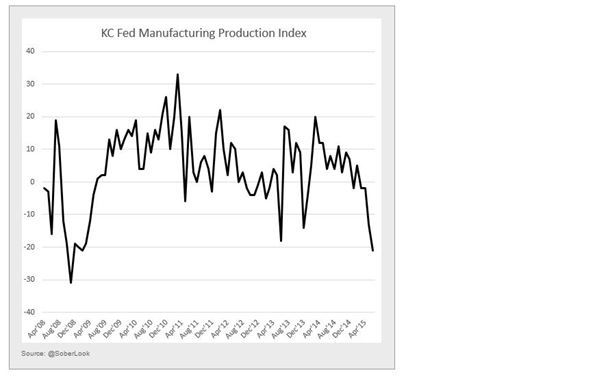

3. On the other hand, here is the Kansas City Fed Manufacturing Production Index.

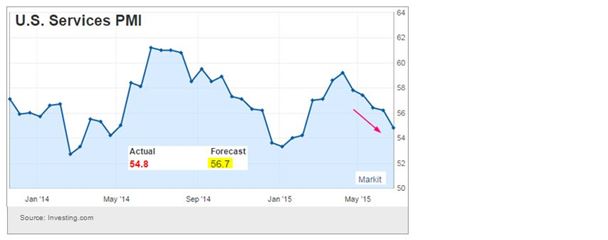

4. Markit PMI showed that US services sector growth has slowed. The report was weaker than consensus.

Disclosure: Originally published at Saxo Bank TradingFloor.com