Shares of Bed Bath & Beyond Inc. (NASDAQ:BBBY) , a leading operator of specialty retail stores, lost nearly 13% over the past six months and estimates are witnessing downward revisions. Let’s delve deeper and try to find out what is taking this Zacks Rank #4 (Sell) company down the hill.

After witnessing a positive earnings surprise of 6.1% in the final quarter of fiscal 2015, Bed Bath & Beyond began fiscal 2016 on a dismal note, with both its top and bottom lines lagging estimates in the first quarter. The company’s quarterly earnings of 80 cents per share plunged nearly 14% year over year and missed the Zacks Consensus Estimate of 86 cents.

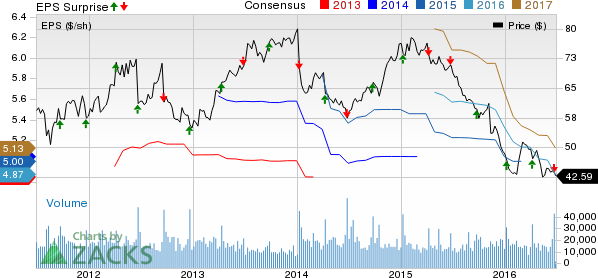

Consequently, the Zacks Consensus Estimate of $4.87 and $5.13 for fiscal 2016 and fiscal 2017 has dropped 13 cents and 11 cents, respectively, over the past 7 days. Moreover, the Zacks Consensus Estimate for the second quarter has decreased 4 cents to $1.18 over the same time frame.

BED BATH&BEYOND Price, Consensus and EPS Surprise

BED BATH&BEYOND Price, Consensus and EPS Surprise | BED BATH&BEYOND Quote

Per sources, the company faced fierce competition from online giants like Amazon.com (NASDAQ:AMZN), alongside bearing the brunt of sluggish mall traffic. Also, intense sales promotions and a shift from the brick-and-mortar store concept to online, weighed on Bed Bath & Beyond’s margins. Together, these factors affected its quarterly results.

Owing to its exposure to international markets, Bed Bath & Beyond faces various risks associated with international operations, including legal and regulatory hurdles, changing global fashion trends and unfavorable currency fluctuations. Hence, persistence of these headwinds is likely to weigh on the company’s results, thus posing concerns.

Going forward, the company’s margins will remain pressurized mainly due to soft merchandise margins and a rise in net direct-to-customer shipping costs. Management expects all these factors to linger in the future and therefore, anticipates gross margin and SG&A expense deleverage in fiscal 2016. We expect the pressurized margins and higher expenses to dent the company’s bottom line.

Nonetheless, management remains hopeful about driving future growth on the back of its strategic investments and omnichannel progress. Following the soft quarter and considering the current trends with the expected impact from the company’s recent acquisition of One Kings Lane, management still anticipates fiscal 2016 earnings per share in the range of $4.50 to a little over $5.00.

Investors like to buy stocks with a track record of better-than-expected results, constant rise in share price and a favorable recommendation. They must exercise caution when it comes to selecting stocks in order to maximize their returns. Considering all the aforementioned factors, we think that it would not be prudent to keep the Bed Bath & Beyond stock in your portfolio, at least for the time being.

Stocks that Warrant a Look

Investors interested in the retail space may consider some better-ranked stocks such as Delta Apparel Inc. (NYSE:DLA) , sporting a Zacks Rank #1 (Strong Buy), Cabelas Inc. (NYSE:CAB) and ULTA Salon, Cosmetics & Fragrance Inc. (NASDAQ:ULTA) , both carrying a Zacks Rank #2 (Buy).

CABELAS INC (CAB): Free Stock Analysis Report

ULTA SALON COSM (ULTA): Free Stock Analysis Report

BED BATH&BEYOND (BBBY): Free Stock Analysis Report

DELTA APPAREL (DLA): Free Stock Analysis Report

Original post

Zacks Investment Research