Financial news junkies love the Eurozone. Just when things seem to quiet down, something always flares up in the region. This time Portugal has been grabbing the headlines.

The Economist: NO ONE is likely to emerge a winner from the political disarray triggered in Portugal by the resignations of the finance and foreign ministers. For two years the country has won plaudits as the best behaved of peripheral Europe’s bailed-out countries. But voters have tired of the relentless austerity that Portugal has had to endure under the terms of its €78 billion bail-out programme, and the repercussions appear to have split the two-party coalition government. Portugal’s international creditors, the “troika” of the EU, the IMF and the European Central Bank, are seeing their star pupil brought low by the political and social costs of implementing their rescue plan.

CDS spread hit the high for the year - though nothing close to historical highs.

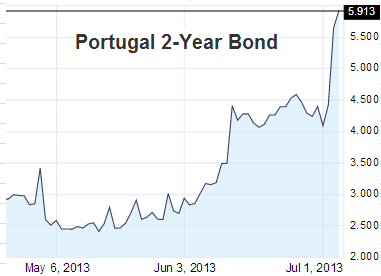

While the media has been focused on the 10-year bond yields spiking, the real action was in the short end of the curve. The 2-year paper for example, moved by some 150 bp in a matter of days.

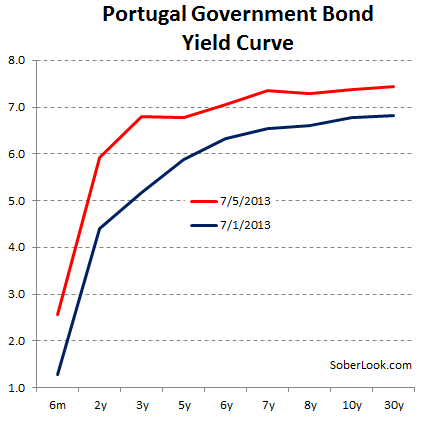

In fact, the yield curve flattened in a manner reminiscent of the dark days of the Eurozone crisis.

One of the concerns with respect to Portugal is that officially the nation may not qualify for the OMT support - the ECB's bond buying guarantee. That's because when the OMT program was announced less than a year ago, it was aimed at nations that have not yet received the full bailout package from the EU/IMF, which Portugal has. The idea was to limit it to nations that still have "market access". Without the OMT backstop - which is expected to target the short end of the curve - Portugal's short-term paper is vulnerable, resulting in higher short-term yields. That will hurt Portugal's economy because now even shorter dated loans will become expensive (in spite of ECB's overnight rates at 0.5%).

The IMF has been pressuring Mario Draghi to include Portugal in the OMT program for some time. The IMF is clearly concerned about having to provide additional support for Portugal, and would rather see the ECB come to the rescue.

Bloomberg: - “Eligibility to the ECB’s Outright Monetary Transaction [OMT] program would also go some way in helping improve the monetary transmission mechanism in Portugal and secure durable market access,” the [IMF] said in a staff report about the seventh review of the aid program for Portugal."

Now the pressure is on the ECB to make an exception for Portugal. From the beginning, analysts have said that Portugal should be the first candidate for the program. However, if the central bank does so, Greece may request the same support from the ECB, making the whole process politically tricky. The ECB certainly does not want to be buying Greek bonds at this juncture. Mario Draghi, who made the official statement that Portugal will be excluded from the OMT, is once again asked to solve structural and political problems that should not be the purview of an independent central bank.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

As Portugal's Yield Curve Flattens, Draghi Put On The Spot Once Again

Published 07/05/2013, 05:19 AM

Updated 07/09/2023, 06:31 AM

As Portugal's Yield Curve Flattens, Draghi Put On The Spot Once Again

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.