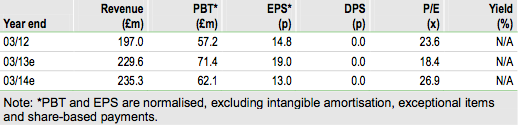

BTG is entering a critical 12-month period marked by multiple catalysts involving its lead internal programmes (Varisolve, Beads) and partnered drugs (Lemtrada). Key near-term catalysts include FY13 results (20 May) and EU (Q213) and US (H213) regulatory decisions on Lemtrada. Continued growth in core direct sales (Specialty Pharma, Interventional Medicine) and Zytiga royalties suggests FY14 revenues of £235m; it also supports our DCF-derived valuation of £1.3bn, or 398p per share, implying 11% upside.

Updated Model Reflects Strong Core Business

BTG’s recent pre-close update guided to FY13 revenues of c £230m (prev. £215m) driven by growth in core business activities and one-off effects. We believe c 30% of the £15m guidance uplift came from increased Zytiga royalties, strong sales of Specialty Pharma drugs (c 20%), a CytoFab final payment (c 25%) and favourable FX movements (c 25%). We now forecast FY13 revenues of £229.6m, underlying diluted EPS of 19.7p and period-end cash of £151m. Looking forward, continued growth in Specialty Pharma (+7% y-o-y), Interventional Medicine (+12%) and Zytiga royalties (+38%) suggests FY14 revenues of £235m and underlying EPS of 16.2p.

Zytiga: Multiple Growth Drivers In mCRPC

We expect BTG to receive Zytiga royalties of c £42m in FY13 on sales of $1.1bn by partner J&J. The Q113 uptick in US sales and script growth allays, in our view, concerns about new competition from Medivation/Astellas’ Xtandi. We expect the expanded label and ongoing ex-US roll-out to drive continued sales growth in 2013.

Lemtrada: Upcoming Regulatory Catalysts A Positive EU regulatory opinion for Lemtrada in relapsing multiple sclerosis (RMS) in Q213 could lead to EU approval and launch by partner Sanofi in Q313. An FDA decision is expected H213. Phase III extension data reinforce our positive view on Lemtrada’s efficacy. However, we continue to believe that a positive benefit-risk decision by the EU regulator hinges on the risk (safety) side of the equation.

Valuation: Fair Value Of 398p Per Share

We value BTG at £1.31bn, or 398p per share, based on a DCF analysis of revenues/royalties on marketed products (£737m), probability adjusted estimates for Varisolve (£270m) and Lemtrada (£147m), plus end-FY13 cash of £153m. We continue to view BTG as an attractive investment proposition, with the current share price offering c 11% upside to a valuation underpinned by its core cash-generative business segments and a low-risk profile by biotech standards.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

An Inside Look At BTG

Published 05/02/2013, 11:57 AM

Updated 07/09/2023, 06:31 AM

An Inside Look At BTG

Catalysts And Core Growth

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.