Synta’s investment case now effectively rests on the success of ganetespib in its two target registration indications of non-small cell lung cancer (NSCLC) and metastatic breast cancer (mBC). Following a $60m fund-raising last year, Synta is poised to embark on the c 500 patient GALAXY-2 Phase III study of ganetespib in second-line NSCLC. This will run in parallel with its CHIARA Phase II study in ALK+ NSCLC, while a separate Phase II study is underway in mBC. We have revised our rNPV to reflect Synta’s effectively exclusive focus on ganetespib and now indicate a valuation of $791m or $11.48/share (basic) or $11.00/share (fully diluted).

Aim To Exploit Survival Advantage In Better Prognosis

The GALAXY-2 study in second-line NSCLC will start recruitment in early 2013. The study will enrol c 500 patients who were diagnosed at least six months prior to the time of entry, thereby excluding patients of poor prognosis based on progression (about 30% of total). This design is based on interim data from GALAXY-1, which showed that the survival advantage was greatest in these better prognosis patients.

CHIARA Study In ALK+ NSCLC

The CHIARA Phase II study of ganetespib as monotherapy in ALK-positive, crizotinib- naïve patients gives the drug a second potential indication in NSCLC, assuming the trial can enrol patients and demonstrates a robust response rate, duration of response and good safety profile.

Multiple Data Points From GALAXY-1 And 2

Synta expects to release more overall survival (OS) and PFS data of the ITT group and sub-populations of GALAXY-1 during 2013 that could shape its registration strategy. The speed of GALAXY-2 enrolment will determine the timing of the interim and final analysis of this trial, tentatively scheduled for the first and second half of 2014.

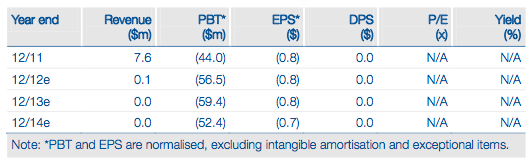

Valuation: $791m Or $11.48 Per Share

Our updated valuation reflects Synta’s principal focus on ganetespib in the two main indications of NSCLC (second-line and ALK+) and mBC. We calculate an rNPV of ganetespib in these two indications of $743m, using a conservative 50% (for a Phase II/III asset) probability in NSCLC. Adding year-end 2013 net cash ($23m) and a nominal value of $25m for other assets, we derive a total firm value of $791m, which is equivalent to $11.48/share ($11.00 per share, fully diluted). We would expect to apply a more normal 65% Phase III probability, which would give rise to a higher valuation, if final Phase II OS data from GALAXY-1 are positive.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

A Look At Synta Pharmaceuticals

Published 02/25/2013, 11:19 AM

Updated 07/09/2023, 06:31 AM

A Look At Synta Pharmaceuticals

GALAXY-2 Poised To Start

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.