Thursday’s a busy day for updates on business sentiment, including purchasing managers indexes (PMIs) for France (08:00 GMT) and Germany (08:30 GMT), followed by the Philadelphia Fed Manufacturing Index for the US (15:00 GMT). The main events are the flash estimates of Eurozone PMIs for services and manufacturing, which will be closely analysed for insight on disinflation/deflation risk in November. Later, we'll see a new report for the UK CBI Industrial Trends Survey and the US Manufacturing PMI. Keep in mind that European Central Bank President Mario Draghi is scheduled to speak today (10:05 GMT).

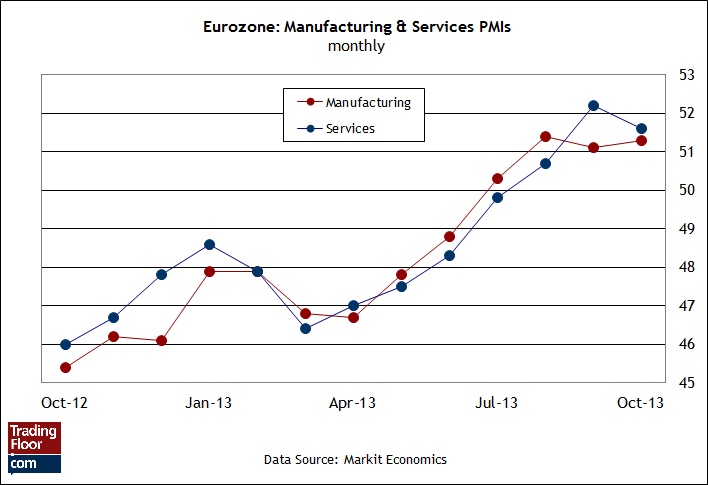

Eurozone Manufacturing & Services PMIs (09:00 GMT) The sharp drop in consumer inflation in Europe in the flash estimate for October was widely seen as a warning that the macro trend is deteriorating. Yet there’s no sign of trouble in the survey data for the services and manufacturing sectors, at least not yet. The mood in the business community remains moderately upbeat, as current data for Markit’s PMIs show. But this relatively bright outlook contrasts with the latest change in the inflation trend, which inspired the European Central Bank to announce a surprise cut in its policy interest rate earlier this month. So, which is it? Is Europe sinking into a deeper funk? Or is the economy still making progress? Today’s flash report on Eurozone PMI data for November may provide an answer.

If today’s release shows a sharp drop for both the manufacturing and services sector, the crowd isn’t likely to overlook the news. All the more so if we see numbers that fall below the neutral 50 mark again. But that’s not likely, or so analysts advise. The consensus forecasts for both PMI numbers anticipate a slight rise for manufacturing and an even bigger advance for services.

After several months of 50-plus readings for manufacturing and services, the moderately bullish trend in the PMI data looks convincing. But that implies that the inflation slump last month is a temporary affair. Which data set is right? We’ll have a better sense of where the truth lies after today’s PMI report.

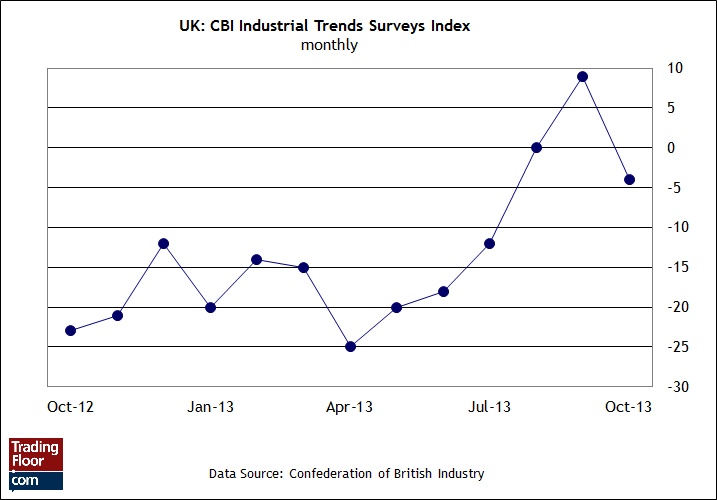

UK CBI Industrial Trends Survey (11:00 GMT) Expectations that the Bank of England might raise interest rates sooner than previously assumed were dashed in yesterday’s release of minutes for the November meeting of the monetary policy committee. The minutes also suggested that the bank’s forward guidance was in flux: “With the proviso that medium-term inflation expectations remained sufficiently well anchored, the projections for growth and inflation under constant Bank Rate underlined that there could be a case for not raising Bank Rate immediately when the 7 percent unemployment threshold was reached.”

One of the reasons why the market was considering an early rate hike is the recent strength in manufacturing. The rebound in recent months for this cyclically sensitive sector can be seen in the sharp rise in the CBI Industrial Trends Survey Index. This benchmark posted a strong five-month rally through September before slumping in last month’s update thanks to weak orders for exports.

Economists think we’ll see a modest rebound in today’s November report. The consensus forecast anticipates that this index of sentiment among manufacturing executives will rise to 1 after slipping to -4 last month (a positive reading equates with expectations for improving business conditions). With the threat of higher interest rates reduced to a near-zero probably for the immediate future, and perhaps even longer, the prospect of continued growth in manufacturing and elsewhere will inspire the bulls anew. Indeed, low interest rates as far as the eye can see with a steady economic recovery is a powerful combination.

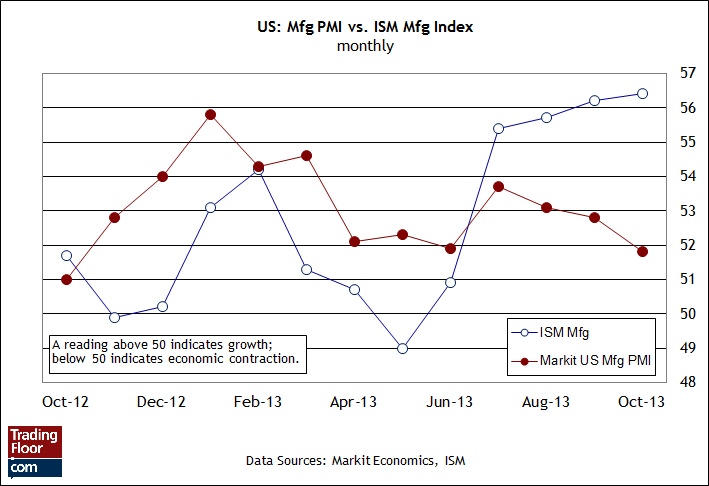

US Manufacturing PMI (14:00 GMT) Is the outlook for manufacturing improving? The answer depends on your preference of survey data. The ISM Manufacturing Index has been increasing since June, with the October number inching up to its highest level in more than two years. But Markit’s purchasing managers index (PMI) tells a different story. This competing benchmark has been sliding since July, dipping last month to its lowest level in a year. Although both metrics still tell us that the US manufacturing sector is growing, the PMI numbers suggest that trouble is brewing.

Which indicator is misleading us? One or the other has to give way… soon. Perhaps today’s the day. Indeed, economists project that the flash PMI for November will post a sizeable increase to 53.0 versus October’s 51.8, according to the consensus forecast.

But what about the divergence in the recent past? One explanation for the soft number in the Markit indicator for October is last month’s government shutdown. "It is impossible to disentangle the impact of the shutdown from other factors that might have been at play during the month," Markit’s chief economist said with last month's release. Maybe, but why isn’t the fallout from Washington’s budget battles infecting the ISM data? For the moment, no one seems to know. Perhaps we’ll have the answer when Markit publishes fresh data for November.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

3 Numbers To Watch: EU PMIs, UK CBI Ind. Trend Survey, US PMI

Published 11/21/2013, 06:44 AM

Updated 03/19/2019, 04:00 AM

3 Numbers To Watch: EU PMIs, UK CBI Ind. Trend Survey, US PMI

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.