Sign up to create alerts for Instruments,

Economic Events and content by followed authors

Free Sign Up Already have an account? Sign In

Please try another search

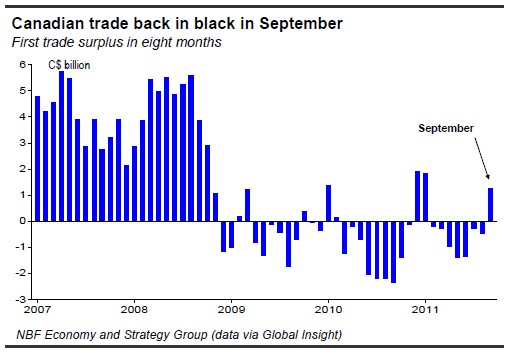

– In September, Canada’s merchandise trade balance was back in the black for the first time since January, pegging in at C$1.25 billion. Consensus expectations were for more red ink. Moreover, a revision of the previous month’s numbers saw the August deficit contract slightly. Contributing to this surprising return to surplus was a surge in exports (+4.2%) and a simultaneous retreat in imports (-0.3%). Energy was the big driver behind the advance in exports with an 11.3% increase. However, decent gains were posted by other sectors as well, including autos, forestry, agricultural products and industrial goods and materials. These more than offset a pullback in machinery and equipment. In real terms, exports climbed 1.2% while imports fell 1.9%.

Unlike in Q2, trade is set to contribute positively to GDP in Q3 thanks to an 18% annualized increase in export volumes on the quarter. The 11.5% decline in real imports of machinery and equipment heralds a decrease in business investment in Q3. This development is not surprising given the preceding quarter’s unsustainably hot pace. Looking ahead to Q4, some sectors of the economy have a good deal of catch-up potential. Production and real imports of autos bounced back strongly in Q3, but these were put in inventories as exports stagnated in the quarter. As a result, inventories are tracking at about 30% annualized growth in Q3. With solid demand for autos in the final quarter of the year (if U.S. October sales are any guide), expect these Canadian inventories to recede and auto exports to rise further. We saw a similar response in Q1 of this year following inventory accumulation the quarter before. Energy, too, has potential in the final quarter of the year, particularly given the partial rebound in Q3 (+11.4% after -22% in Q2). Hence, trade could provide some upside to Q4 GDP growth.

In October, Canadian housing starts were down slightly to 207.6K from an upwardly revised 208.8K in September. This nonetheless beat consensus, which did not expect the month’s total to top 195K. The decline was driven by singles, which fell 6K to 60.9K. Multiples provided partial offset by increasing 2K to 123.6K. On a regional basis, in urban areas, Quebec and the Atlantic region posted the biggest drops. Also, recent labour market trends suggest that disposable income, which flat-lined in the first half of the year, should not improve much going forward. This will somewhat counteract the positive impact of low interest rates on the housing market.

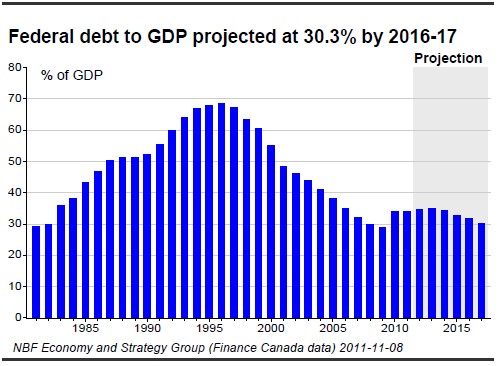

In the Update of Economic and Fiscal Projections presented this past week by Finance Minister Jim Flaherty, growth expectations for Canada were revised

down for the near term, compared with the assumptions underlying the June budget. In general, economists now see the domestic economy expanding 2.1% in 2012, down from 2.8% earlier this year. Not only did the Finance Minister take note of this, but in light of the heightened risks to the economic outlook related to external factors, the government has made additional provisions for a cumulative $6.0 billion to account for risks to revenues over the next three years. Consequently, the deficit pattern is now somewhat higher than was projected in June. Still, considering the savings targeted by the Strategic and Operating Review, a small budget surplus of $0.6 billion is projected for 2015-2016. For the following year, a surplus of $4.6 billion is expected. By then, the

debt-to-GDP ratio should reach 30.3%, which is 4.7 percentage points below the mark projected for fiscal 2012-13.

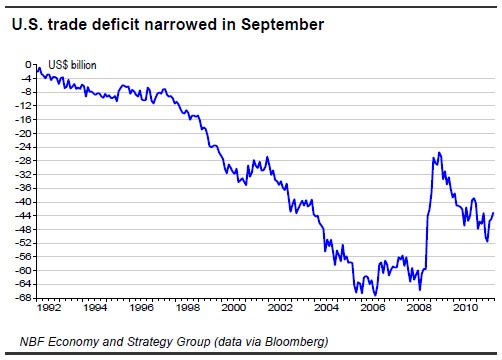

United States – In September, the trade deficit narrowed to $43.1 billion from a revised $44.9 billion in August. Exports grew $2.5 billion to $180.4 billion on the month (+1.4%), while imports swelled $0.7 billion to $223.5 billion (+0.3%). The better-than-expected trade data reflected stronger exports in consumer goods and industrial supplies. The real merchandise trade deficit shrank by slightly less than a $1 billion. All in all, the September data suggest trade will add about 0.5% to GDP in Q3.

In October, the U.S. National Federation of Independent Business (NFIB) index of activity and sentiment rose to 90.2 after showing weakness during the summer months (88.1 in August). Though the index remains at a historically depressed level, the turnaround was nonetheless encouraging.

Bank lending conditions remain favourable for U.S. businesses. Indeed, according to the Senior Loan Officer Opinion Survey on Bank Lending Practices, a majority of commercial banks maintained or eased lending conditions on commercial and industrial (C&I) loans in October. At this juncture, the fact that banks are both willing to lend and actually increasing their C&I loan book is a most positive outcome for the U.S. economy. This is a necessary condition (albeit not a sufficient one) to avoid an economic relapse.