The financial world turned back to risk-off mode on renewed fears that the coronavirus will hit global economic growth much more than previously anticipated. Following the rate cuts by the RBA, the Fed, and the BoC, more Banks are expected to take action, with the Fed anticipated to proceed with another bold action at its upcoming meeting, later this month. In Vienna, OPEC members decided to deepen production cuts by 1.5mn bpd, but Russia and Kazakhstan said that they have not agreed yet. As for today, we get the US and Canadian employment reports for February.

RISK APPETITE DETERIORATES AS VIRUS FEARS RETURN

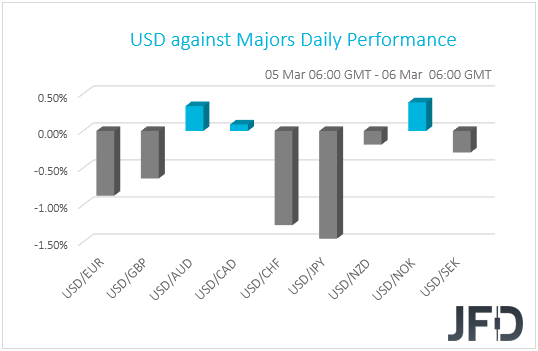

The dollar traded lower against most of the other G10 currencies on Thursday and during the Asian morning Friday. It gained only against NOK, AUD and CAD in that order, while it underperformed the most versus JPY, CHF and EUR.

And we are back on risk-off mode, something clearly evident by the massive strengthening of the safe-havens yen and franc, as well as by the relative weakening of the risk-linked currencies. The strengthening of the euro also supports that view. Remember that we recently have been repeating that the euro may have been also used as a vehicle for curry trades, due to Eurozone’s negative interest rates, and at times when investors unwind such trades, it gets benefited. The exception here is the US dollar, which has taken off its safe-haven suit, perhaps on elevated expectations that the Fed’s double cut delivered this week will be accompanied by more. According to the Fed funds futures, another 50bps decrease is nearly fully priced in for the next gathering, while US Treasury yields continued tumbling, with the 10-year rate hitting a new record low and the two-year one falling to its lowest in more than three years.

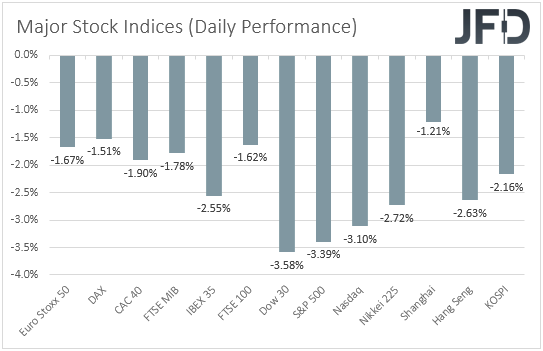

Shifting our gaze to the equity market, we see a sea of red. Major EU indices fell by more than 1.5%, with Spain’s IBEX 35 taking the lead in this tumbling race, losing 2.55%. The risk aversion accelerated during the US session, with all three of Wall Street’s main indices falling more than 3%. As for today, in Asia, Japan’s Nikkei and China’s Shanghai Composite closed 2.72% and 1.21% down respectively.

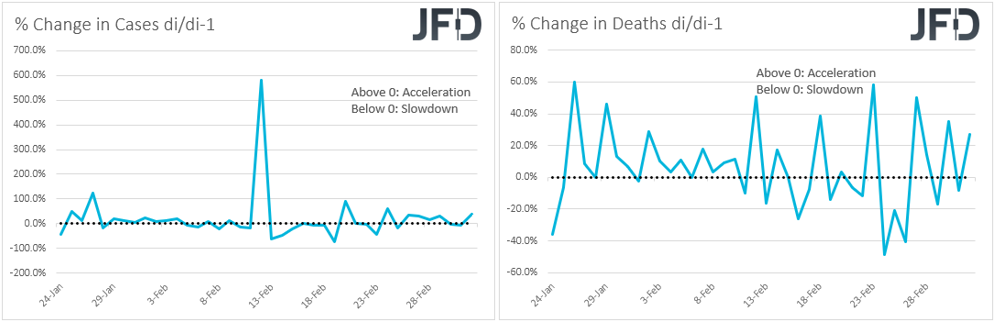

For the umpteenth time, the driver was concerns over the coronavirus’s damaging impact on the global economy. Although new infections have slowed in China, the situation elsewhere appears to be out of control, with the virus in Europe, Britain and North American, spreading at a crazy pace. Overall, both infected cases and deaths entered acceleration mode yesterday, with cases surging to 98407 and the death toll climbing to 3385.

All this adds more credence to our view that with no vaccine in the horizon, and with the virus still spreading fast, the damage may not be that temporary as many initially believed. We stick to our guns that interest-rate cuts by themselves may not be enough to revive growth, and that the economic wounds could well drag into Q2. Even if central banks are willing to ease further, with the uncertainty over whether the virus can be contained or not, we see it hard for consumers and businesses opting for cheap loans and start spending. Therefore, we believe that there is still room for equities and risk-linked assets to slide further as investors divert flows to safe havens. As we noted several times in the past, currency pairs that can act as a gauge of investor morale are those consisting of a commodity-linked currency, like the Aussie and Kiwi, and a safe-haven, like the yen and the franc. This time around, the euro could be also included. In other words, we see the case for pairs like AUD/JPY, NZD/JPY, AUD/CHF and NZD/CHF to continue tumbling, while EUR/AUD and EUR/NZD may continue climbing north.

OPEC AGREES TO 1.5MN BPD CUTS, AWAITS NON-OPEC MEMBERS’ DECISION

The Canadian dollar could also stay under selling interest, but we would like to stay away from it for now, until OPEC and its allies arrive to a final and official decision over whether they will cut production further, and if so, by how much. Yesterday, OPEC members agreed for output to be cut by an extra 1.5mn bpd, until the end of 2020, with non-OPEC producers contributing the one third. Nevertheless, Russia and Kazakhstan said that they have not agreed yet to the proposal, something that raised worries with regards to a final accord. Both Brent and WTI slid 1.92% and 1.18% respectively on those concerns.

The non-OPEC members will join OPEC today, and it would be interesting to hear what the final communique will include. If no consensus is found, oil prices are likely to accelerate their downtrend, dragging the Loonie down with them. On the other hand, if non-OPEC producers eventually decide to compromise, both crude prices and the Canadian dollar are likely to rebound. That said, with the fears surrounding the effects of the coronavirus to the global economy still elevated, we are reluctant to call for a reversal. Maybe we could get a decent correction.

NFPS UNLIKELY TO CHANGE USD’S COURSE

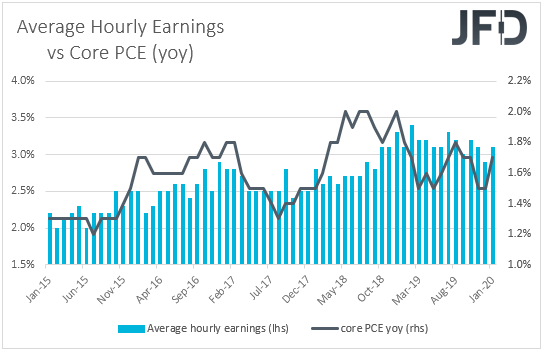

As for today, apart from headlines and developments surrounding the coronavirus and the OPEC+ meeting, investors may also pay attention to the US employment data for February. Nonfarm payrolls are expected to have increased 175k, less than January’s 225k, while the unemployment rate is now forecast to have held steady at +3.6%, just a tick above its 50-year low of 3.5%. Average hourly earnings are expected to have accelerated to +0.3% mom from +0.2%, something that, barring any deviations to the prior monthly prints, will drive the yoy rate up to 3.2% yoy from 3.1%.

Overall, the forecasts point to a decent report, consistent with further tightening in the US labor market. Under normal circumstances, accelerating wages would have raised speculation of higher inflation in the months to come and allow Fed officials to keep their hands off the cut button. However, after Tuesday’s double cut, Fed Chair Powell highlighted that the fundamentals of the US economy remain strong, adding that they decided to cut due to the risks the coronavirus poses to economic activity. Thus, this time around, the employment report may not be so determinant as before with regards to the Fed’s future course of action.

The dollar may strengthen somewhat on solid numbers, but with the virus keep spreading at a fast pace, we will treat such a rebound as a corrective move. With the Fed having much more room to cut than other central banks, the dollar is likely to resume its latest downtrend. Yes, the ECB is expected to cut as well, but only by 10bps. This is the smallest percentage expected to be cut among major central banks, and this may have been another reason why the euro is flying. The conclusion is that we see ample room for EUR/USD to continue drifting north, even if it corrects lower in the aftermath of the data.

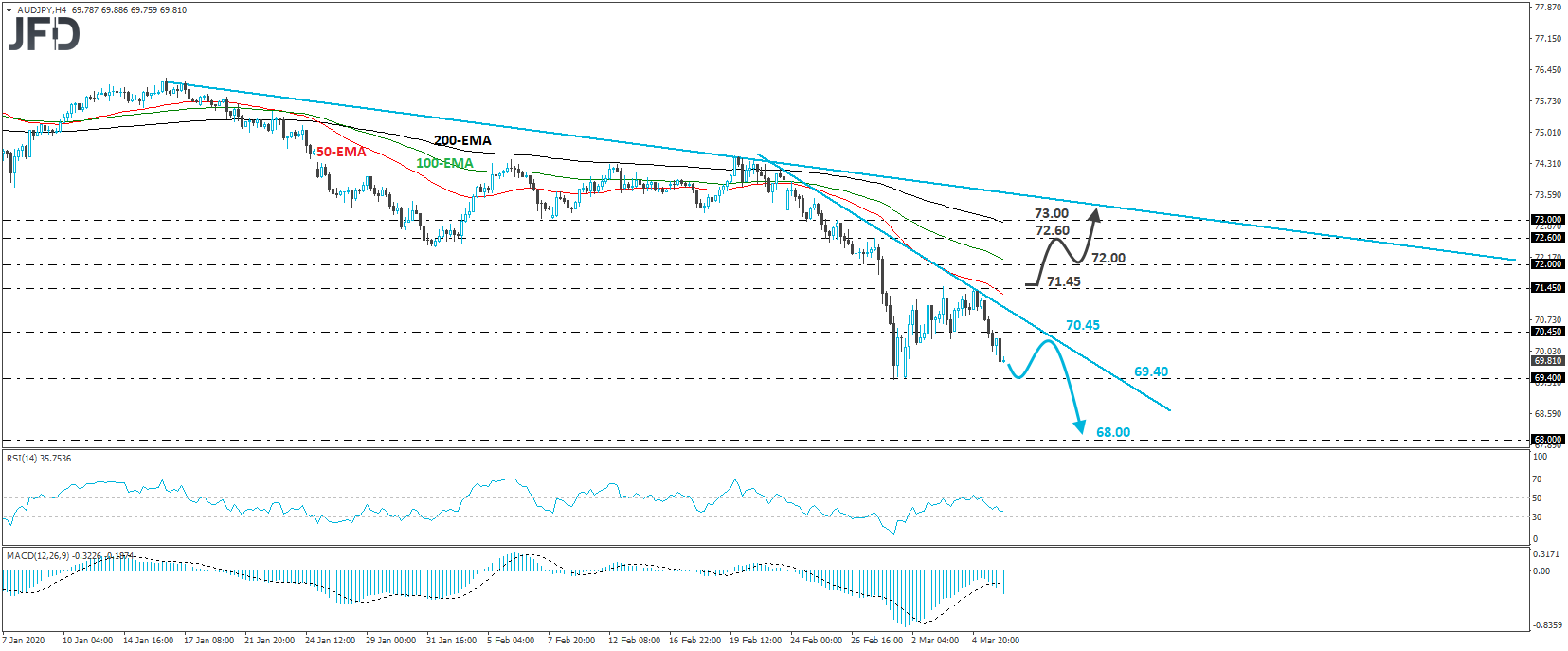

AUD/JPY – TECHNICAL OUTLOOK

AUD/JPY tumbled yesterday, falling below the 70.45 barrier, something suggesting that the corrective rebound started on Monday may be over. The rate is now trading below a tentative short-term downside resistance line drawn from the high of February 21st and thus, we would consider the near-term outlook to be negative.

The pair looks to be heading for another test near the 69.40 zone, marked by the lows of February 28th and March 1st. The bears may decide to take a small break after challenging that zone, thereby allowing another small corrective bounce. That said, if such a recovery stays limited below the aforementioned downside line, we would see decent chances for the bears to jump back into the action and push the rate back down. If they manage to overcome the 69.40 barrier this time around, we may see them pushing towards the 68.00 zone, marked by the low of the third week of April, 2009.

In order to start examining the case of a larger correction to the upside, we would like to see the rate climbing above 71.45. This would confirm the break above the tentative downside line, and also a forthcoming higher high on the 4-hour chart. The bulls may then get encouraged to push towards the 72.00 zone, the break of which could allow extensions towards the 72.60 hurdle, defined as a resistance by the high of February 27th. Another break, above 72.60, may pave the way towards the 73.00 area, or the downside line taken from the high of January 16th.

EUR/USD – TECHNICAL OUTLOOK

EUR/USD skyrocketed yesterday, breaking above the long-term downside resistance line drawn from the peak of January 10th, 2019. The move also confirmed a forthcoming higher high, with the rate challenging the 1.1240 zone, defined as a resistance by the high of December 31st. Bearing in mind that EUR/USD resumed its latest rally and managed to overcome the aforementioned long-term downside line, we will consider the outlook to be positive and we would expect some further advances.

If the bulls are strong enough to overcome the 1.1240 zone, we could see them aiming for the 1.1285 barrier, which provided strong resistance between July 11th and 18th. Another break, above that key hurdle, may set the stage for the 1.1345 barrier, marked by the inside swing lows of June 25th, 26th, 27th, and 28th. That said, bearing in mind that our short-term oscillators show signs that the momentum may start slowing, we see the case of a possible setback before the next leg north, perhaps for the rate to test the pre-mentioned downside line as a support this time.

On the downside, we would like to see a clear dip below 1.1095 before we abandon the bearish case. Such a move would not only bring the rate back below the long-term downside line, but would also confirm a forthcoming lower low on the 4-hour chart. The bears could then get encouraged to extend the dive towards the 1.1052 level, the break of which may open the way towards the psychological round figure of 1.1000. If they are not willing to stop there either, a break lower could target the low of February 28th, at around 1.0950.

AS FOR THE REST OF TODAY’S EVENTS

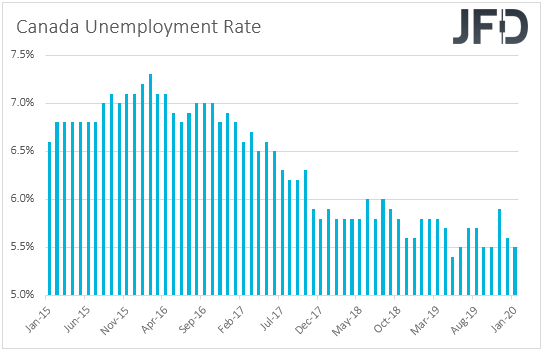

Apart from the US employment report, we get jobs data from Canada as well. The unemployment rate is expected to have ticked back up to 5.6% from 5.5%, while the net change in employment is anticipated to show that the economy gained less jobs than it did in January. Specifically, it is expected to show an increase of 10k jobs, less than the prior print of 34.5k. Following the double cut by the BoC on Wednesday, a soft employment report is likely to keep the door for more easing wide open.

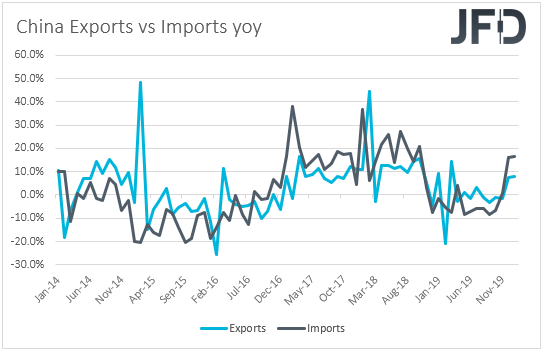

As for tonight, during the Asian morning Saturday, China’s trade balance for February is coming out. Both exports and imports are expected to have slumped 8.4% yoy and 9.0% yoy respectively, after rising 7.9% and 16.5% in January. This may result in a shrinking surplus of USD 12.75bn from USD 47.21bn. The outbreak of the coronavirus started in China, the authorities of which have adopted restrictive measures in their attempt to contain the virus, something that is expected to have hurt businesses, and thereby exports and imports. Even if we see larger slides, this will not come as a surprise to us. In any case, bigger declines may increase concerns that the virus’s economic effects are larger than previously anticipated and may result in another round of risk aversion at the start of next week.

We also have five Fed speakers on today’s agenda: Chicago President Charles Evans, Cleveland President Loretta Mester, St. Louis President James Bullard, New York President John Williams (NYSE:WMB), and Boston President Eric Rosengren. It will be interesting to hear what they have to say about the FOMC’s policy plans. Are they indeed considering to lower rates further, and if yes, by how much?

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Markets Turn “Risk Off” Ahead Of NFPs, OPEC Awaits Green Light From Russia

Published 03/06/2020, 04:31 AM

Updated 07/09/2023, 06:31 AM

Markets Turn “Risk Off” Ahead Of NFPs, OPEC Awaits Green Light From Russia

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.