Monday December 5: Five things the markets are talking about

Is there EMU turmoil on the horizon? The odds are beginning to stack up.

Italy’s pro-EU Renzi stood down as PM earlier this morning after his referendum for Italian constitutional change was resoundingly beaten by a record turnout Sunday. This has paved the way for another general election and the possibility of an anti-EU party win for the fourth largest economy in the eurozone.

There has been no early reaction from the European Commission to the news, with officials calling this a domestic Italian issue, and not a vote on the European Union. With national elections slated for the Netherlands, France, Germany and Italy next year will certainly keep the euro markets under pressure (overnight – EUR prints a 20-month low, periphery yields back up while bund prices rally).

Elsewhere, Austria chose a Pro-EU President in their elections on the weekend; the result was a rejection to the ‘populist’ Freedom Party. In New Zealand, PM John Key indicated that he will step down and will not seek reelection in 2017.

Aside from political uncertainty, this is a busy week on the monetary policy and data front. Four central banks will announce their rate decisions – Reserve Bank of Australia (RBA), Reserve Bank of India (RBI), European Central Bank (ECB) and Bank of Canada (BoC). The Aussies post their Q3 GDP data, while composite and/or service PMI’s will be reported for Japan, China, India, Eurozone, France, Germany and the U.S.

1. Mixed equity response to Italy’s outcome

Being the first line of defense due to timing, Asian shares have taken the brunt of the pressure overnight; mostly declining amid concerns the result of the Italian referendum could trigger a selloff in Europe’s banking shares that would ripple worldwide.

Japan’s Nikkei Stock Average fell -0.8%, while stocks in Shanghai fell -1.2% and stocks in Hong Kong shed -0.5%.

In Europe, stock indexes are rallying in early trade as markets respond in a remarkably muted manner to Italian voters’ rejection of constitutional reform. Naturally, Italian bank stocks and government bonds are under pressure, but the bulk of the negativity for Italian equities, bonds and the euro seems to have been mostly priced in leading to the vote.

The Stoxx Europe 600 has rallied + 0.7%, while Italy’s FTSE MIB index fell -1.3%, led lower by the banking sector. The wider Euro Stoxx Banks Index is down -1.7%. Mining stocks are leading the gains in the FTSE 100, further supported by Brent and WTI which are trading sharply higher intraday.

U.S futures are set to open +0.5% higher.

Indices: Stoxx50 +1.5% at 3,063, FTSE +0.8% at 6,786, DAX +1.7% at 10,696, CAC 40 +1.4% at 4,594, IBEX 35 +1.3% at 8,716, FTSE MIB +0.4% at 17,157, SMI +1.2% at 7,874, S&P 500 Futures +0.5%

2. Crude prices see support; industrial metals climb

Crude oil prices continue to find traction, trading at a fresh 16-month high overnight, as optimism spreads about the prospect of a “tightening” market after last week OPEC deal to cut production.

Brent crude oil futures has soared to +$55.20 a barrel, up +62c or +1.1%. WTI crude oil is trading up +54c, or +1% at +$52.22 a barrel. Since last Wednesday’s deal, Brent is up +19%, the highest in almost eight years while WTI is up +16%.

For crude bulls, the one large uncertainty in the global supply balance is U.S output. The higher energy prices go the more off line drillers become attracted to increase production.

In industrial metals, copper have rallied +1.8%, while zinc has gained +2.2% and nickel +1.7%. Ahead of the U.S open, gold has fallen -0.4% to +$1,164.75, extending its -0.5% decline last week.

3. Euro periphery yields back up, Fed to go

Sovereign debt is the notable black spot in the market after Italy’s Renzi loss. Italian bond yields continue to rally (10’s +11bps to +2.01%), while debt from other riskier countries such as Spain (+5ps to +1.595%) and even France underperformed versus German bunds (+3bps to +0.31%).

The swap in yield between 10-year Italian and German debt is +7bps wider to +1.702%.

Elsewhere, Aussie and Kiwi yields both eased, falling -7 and -5bps to +2.79% +3.19% respectively. Stateside, U.S benchmark 10-Year yields rose +2bps to +2.40% after shedding -7bps on Friday after the nonfarm payroll (NFP) print (+178k jobs).

With the U.S. unemployment rate falling to a nine-year low of +4.6% in November is making it almost certain that the Fed will raise interest rates on Dec 14.

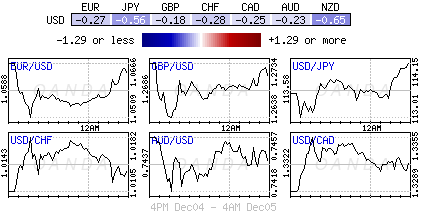

4. Euro down, but not out

For the time being, the EUR (€1.0651) has clawed back most of its early losses (20-month intraday low €1.0538) after yesterday’s Italian Referendum defeat.

The single currency’s modest decline would suggest that investors had anticipated that Renzi would lose. Nevertheless, expect political uncertainty throughout mainland Europe (Netherlands, Germany, France and Italy) to keep modest pressure on the EUR for the foreseeable future.

The ‘big’ dollar continues to out perform across the board (US Dollar Index +0.2% to 100.95) on rate expectations – Fed is expected to hike on Dec 14 and more to come next year (¥114.31).

The NZD, which earlier weakened almost -1% to +NZ$0.7070 after PM John Key unexpectedly announced his resignation overnight, has recovered a tad to trade down -0.5% at +NZ$0.7090.

5. Euro sales and business activity improve

This morning’s October Eurozone retail sales were stronger than expected, rising +1.1% on the month vs. +0.8% expected – the largest increase in two-years. The headline print is yet another sign that the eurozone’s modest recovery has gained some momentum and is also an indication that high levels of political uncertainty are having little impact on activity.

Other data showed that Eurozone business activity last month grew at the fastest pace in 2016 (53.9 vs. 53.3 m/m).

However, with the sustainability of a recent pickup in inflation still very much in doubt, the market expects the ECB to extent its QE program beyond March at this weeks ECB meet.